pearls of wisdom. Good to hear that and it makes me saner looking at the madness around

I forget his name. One of the regular "experts’ on CNBC. He sold all equity and booked profit before the

crash in January 2008. He was asked what made him do that. He replied to say " I realized that I am not so intelligent that I can make this kind of money. Something is definitely wrong. Better to take the money out."

I never forgot this. So simple.

15 Likes

Can’t agree more.! Specifically after seeing 10% circuit in CDSL and Au @700.Projocted appreciation of 3 years in just 3 days…! Time is approaching to take the money out and more watchful isn’t it sir…? Any views on salasar public issue please…!

1 Like

Hi vivek

Have u studied jm financial? Wud b interesting to know your thoughts.

Hi Sir

I tried posting on CDSL in another cat but I guess the post got flagged.

So posting it here - I completely agree with your thesis that this is a duopoly + capital light biz + will throw out cash & has a long runway due to the very low demat penetration in India

Looks like a buy and sleep stock - let’s see where it goes.

Current valuations @ INR 400/share do seem a bit bonkers though - but probably because of scarcity as you mentioned.

1 Like

Salasar seems a good issue but of very small size.Chances of allotment is v miniscule .

JM Financials I dont track closely but since tailwinds are there for this sector JM could give good returns.

CDSL & AU Bank gave excellent returns to those who bought on listing days.

One should always book profit when prices run way ahead of fundamentals. Now wait for price to dip to buying range with patience.Keep a watch on coming quarter results.

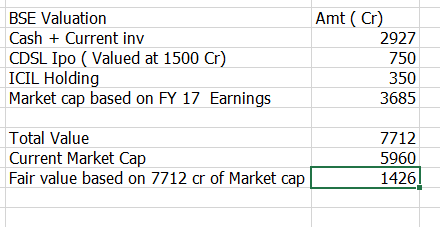

Any views on BSE ? someone tracking it?

1 Like

How retail investors trapped in IPO listing

2 Likes

@Vivek_6954 : Focus lighting does indeed look a promising story. Thank you for highlighting it here!

Optically, the PE of just 9 looks quite attractive.

In your view, how should one value a business such as focus lighting ( with no obvious listed peers).

Does a PE of 20 look reasonable to you ? Or is PE 9 the maximum one can get , accounting for the low entry barriers as mentioned by @whipsaw ?

In other words, will the PE valuation dictated more by the growth rate of this company or quickly get limited by the lack of a ‘moat’ ?

Sir, bought around 900 as it has a duopoly with NSE 2) benefit of CDSL listing of aound 400 cr and having 24% stake post listing. 3)NSE management has internal transparency issue and charges of allegations of unduly favoring some brokers -these may give chance to grab more market share. 4) more and more investors joining the party through IPO and vast opportunity ahead is the reason ,is there any other listed international stock exchange anywhere to compare the future outlook apart from MCX…? hope you have some idea to share with us about BSE LTD.Thanks…

1 Like

check this link

1 Like

https://www.prosperotree.com/investing-idea/stock-idea/bombay-stock-exchange-bse-strong-growth-ahead

An excellent report on BSE ltd from a very astute investor Dhruvesh Sanghavi who runs a superb blog with great recommendation & performance track record.

Views Invited on BSE Ltd

4 Likes

Focus Lighting seems one of the nanocap which needs to be tracked closely .

I bet mainly on promoters & Amit Sheth a 2nd gen entrepreneur with family being in lighting business since last 50 years having started from Lower Chawl lighting mkt in Mumbai.His stake is nearly 75% which is a big comfort as it shows skin in the game.

RONW & CAGR both v decent. Opp size seems big as its focused mostly on LED lighting uniquely designed .Results has been consistent & predictable since 2013 albeit on a small base. Client list is good . manufacturing has started at Bhiwandi & Ahmedabad so the trader impression would reduce.

An architect friend of mine who was earlier v sceptical on the sector mainly due to perceived bias & China threat called the Focus sales rep & was very impressed with the quality n specs of the product which Focus makes. Seems quality as good as Philips but price much less. But now he was skeptical on Focus ability to withstand deep pockets of big competitors.

Focus IPO @45 was priced v cheaply at 5 PE.may be a smart astute cheap way of getting listed in SME & then get listed to main board in 2 year time.

I got in when it opened @ 80 rs & bought higher as well.risk remain its small sizes n competition from big players,key man risk ,China threat,etc,

Have a look at Amits Linkedin profile & activities.

https://www.linkedin.com/in/amit-sheth-96828226/detail/recent-activity/shares/

2 Likes

Whats your view on the upcoming Captain Technocast Ltd SME IPO To Open On 20th July. It has been stated that the Company is bringing the issue at p/e multiple of 15.47 on post issue FY17 eps at a price of Rs 40/- per Share while peers like Bhagwati Autocast ,Carnation Industries, Investment & precision Castings & Nitin Castings are trading at p/e multiple of more than 20.

1 Like

Disc: Invested . Please do your own diligence and research before investing.

1 Like

MRSS reaching 439 vs FPO of 114 in dec 16 when i first wrote about it on this thread.

It may be come the first pure play listed market research company once it lists on main board & shifts from BSE SME.

Discl- Invested in it since FPO@114

Vivek did you attend the Sheela Foam AGM today?

If yes, can you share the management commentary and your impression?

Best regards,

Aniket.

@Vivek_6954

Hi, Demerged entity Sintex Plastic is going to be listed on Monday. RBI has increased limit for foreign investment limit. Could you please share your views on it.

1 Like

Are you sure about Sintex plastic listing on Monday.Co seems a good bet with good EPS & ROCE. who else tracks it?