I think one can play around the numbers to justify current valuations. This is common in bull markets. If one has to use some kind of a accounting mumbo-jumbo to justify current valuations, then that is a warning sign to me.

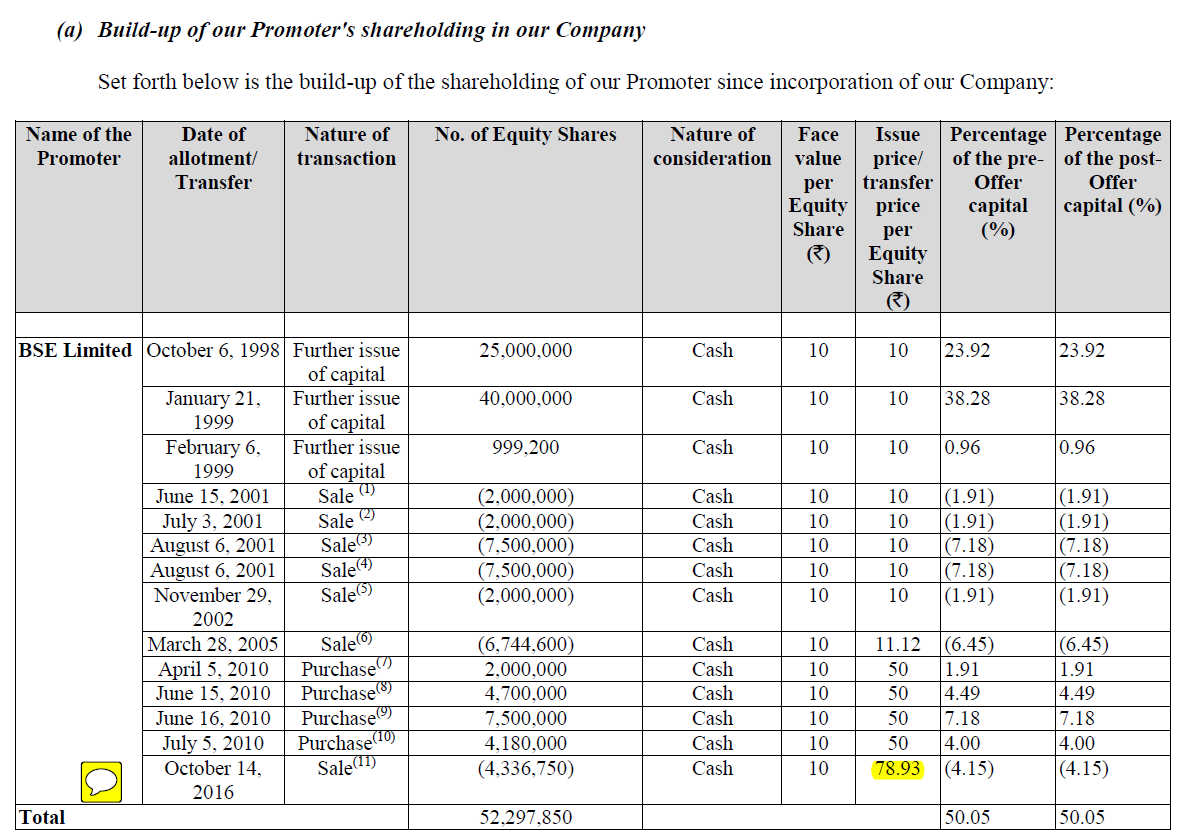

Fact is BSE sold 4,336,750 shares to LIC for 79 Rs/share in Oct 2016. Nothing has changed in last 8 months that will cause CDSL to be worth 3 times. Some liquidity premium is justified but not 200%.

As predicted once the selling from weak hands in retail & HNI category absorbed CDSL moving to new orbit.Today cdsl touches 298.

I feel scarcity premium to remain high as NSDL IPO might not come soon. NSE stake is already at max 24% . This ipo came as BSE was forced by regulators to reduce the stake from 50% to 24%.

Gone through your portfolio thread. Really you are making a killing in the markets. Since it is mentioned in parts, do you mind sharing at one place your core holdings as on date.

Good set of results from Focus Lighting with EPS for fy 17 mentioned in result at 16 anounced on 5 July 17.

I liked the co & had bought on listing & subsequently as well due to

Young promoter in right age of 40s with 75% stake.

Good ratios like ROCE OF 53%,ROIC 45%,PE 9

Good sales growth of 47% & profit growth 196% (Screener) ,Sales & Net Profit has increased from 18 Cr & 0.44 Cr in FY 13 to 71 Cr & 4 Cr in Fy 17.

Promoter is 2nd gen whose family is in lighting business since last 50 years having good reputation in lower chawl are which is the lighting market of Mumbai

Had left lot on table for retail investors as IPO was at PE of 5 only.DE post issue of 0.2 as per RHP. .

Now foraying into manufacturing with 2 units from earlier import from China though having its USP of good design of its own thanks to its agreement with leading designers of Germany & Europe.

Own Brands like Pluslight & TRIX having good demand in the lighting mkt over mass products inspite of being priced 40-50% higher over nass chinese imported products based on some limited scuttlebutt…

Gives good quality product with extended warranty as high as 5 years giving an edge

Good & increasing opp size for Focus with mktcap at lowly 49 Cr only vs sales of 71 Cr in FY 17.OPM of 10% which may go up as per MD once own manfg starts

10)Increasing exports mainly to Middle east which now are 15-17% of turnover showing its capability of countering Chinese import threats even in other countries.

,

11) Good clientele like Shopper Stop, Raymond,Croma, RIL amongst 250 others.

MD Amit Sheth says can easily grow at 25-30% CAGR due to huge opp.His linkedin profile is impressive showing him to be very focussed n well abreast of all development in LED lighting business world over.

May shift to main board in 2 years like other SME cos have done & maybe a smart move on part of promoter to get listed with v little expense vs IPO on main board.Promoter stake is healthy 75%

Risks include high working capital requirement, small size of co,increasing competition from established players like Phillips,Osram & on pricing fromy by Chinese importers,low liquidity in SME like NSE Emerge,big lot size of 3000 shares. Need to closely track whether this nanocap can execute well & become a midcap over next few years.

@Vivek_6954: Sir, a very silly question here. When you say your X of 2012 has become 9X now. Do you consider only the subset of your portfolio which was there 5 years back or do you consider the entire portfolio value as it stands today.

In case you only mention the subset, how do you completely track these changes because you have switched stocks as well as done some changes in the portfolio allocation as well.

I am an eternal optimist & have been mostly remained invested in equity since 2012. I am also a calculated risk taker & have been invested 110 to 120% thru LAS.Though I try that the interest out go on LAS & interest earned by me on my PF of tax free bonds & dividends balance out each other or net out go remains a minimal part of my total portfolio.

Though I earn a salary but most of it goes in repaying EMIs as has been the fad of most middleclass in India taking home loans & other loans since long inspite of rental yield hovering way below the intt on housing loan.As such not much saving from salary goes into equity from mine side & my X of 2012 did not had much contribution from salary or other sources subsequently as well .

But my X in 2012 was not v substantial due to 2 factors

I had large no of scrips as high as 40-50 scrips .

Many were largecaps Like TCS,Icici bank,GAIL.ONGC,OIL,BOB, etc.My performance improved once I reduced the no of stocks to 10-12 resulting in better allocation which is more imp then stock selection IMHO .

I converted all other then TCS into quality small & midcaps like Astral Poly,Mayur uni,Page Ind,Repco Home,Shilpa Medicare,Ajanta Pharma ,OCCL etc thanks to VP.

TCS I held on till 2015 & then converted into quality small n midcaps.

So all I remember is the X of 2012 & present PF value.But then one should not confuse brains with the bull market .This has been an unprecedented bull market for sure due to huge rush of domestic & FII liquidity.

AU finance is a high quality stock which is into collaterized lending unlike MFIs run by a top grade technocrat first gen self made entrepreneur with growth mindset & execution track record and huge plus increasing opp size the criteria I most like while selecting a stock.

Main question is of Valuation.I hope AU finance cracks giving an opp to load at a reasonable valuation. I intend to hold on to my IPO allotments.

Just playing devils advocate: On Focus lighting,

I see many shops in malls & local done by local interior decorator + electricians. So what gives Focus an advantage other than manufacturing their own lights? Even that may be threatened by cheap Chinese imports,

I understand Focus does B2B for major retail chains, but how can they sustain? I have listened to Amit’s interviews. But I don’t see anything niche, which local guys can’t do. Don’t see any entry barrier. One of my friend owns a jewellery shop. Recently he renovated his shop and the woodwork guy himself took care of all lighting and its locations etc. I also did scuttlebutt on one of the retail dress shop here where it is designed aesthetically and lighted beautifully. Its design & placement was also done by local guys with little inputs from owner. Lights were all some unnamed brands bought wholesale from Parry’s corner.

Dear Vivek Gautam Sir,

I am not able to see chart history for FOCUS Lighting as well as VSCL.

Checked in moneycontrol, Rediffmoney and screener

Please correct me if i am missing something here.

Where are you tracking and analyzing these stocks.

Pl dont sell a high quality stock like Shilpa due to temporary lulls in stock price n boredom. Its founded by an intelligent fanatic Vishnukant Bhutada who has professionalized this small co years back in by recruiting a high calibre professional like Mr Sehrawat from Dabur Pharma Oncology division.