I was replying to the person who thought that there is no effect on

reserves. I do not know the answer to why the reserves reduced despite

that.

1 Like

Does anyone know the issue price of the warrants? I read thru Regulation 76 which says that it shouldn’t be less than face value. Does it mean that the promoters + preferential investors can elbow minority investors and get allotment at face value or significant discounted price?

As we have to be balanced in the views.

Looking at the other side - For such a small company, too much diversification - Software, Infra & Health care.

Discl: Invested

1 Like

Convertible equity warrants allotted to promoters and strategic investors for issue price of INR 100…this should now technically form a support in medium term.

Good part is the issue price is higher than the prevailing price of ~90-95 during the announcement date. Plus this will have lock-in of 3 years for promoters (including existing shares if I remember correctly) and after issue of new shares from warrants will have further 3 years lock-in.

http://www.bseindia.com/xml-data/corpfiling/AttachLive/aa648a40-451a-4659-ae29-3ee873eb94f1.PDF

Discl: Invested

4 Likes

Just to understand as to why would promoters allot warrants to themselves instead of buying in the open market, apart from the obvious that they are reducing their risk, they get to buy a higher stake with lesser liquidity which they can convert at a later date when they do have the required funds. Any other pros/cons?

And regarding the effect of warrants on share capital/reserves, if they have to pay only a certain percent of the total value of the shares during the allocation, does the share capital/reserves only increase by the amount given the promoters or the entire value of the shares? And does the promoter shareholding increase right away or after the warrants are converted to equity?

Investor Presentation for quarter ended 31st December,2017

http://www.bseindia.com/xml-data/corpfiling/AttachLive/f300203f-8145-4b9b-ac5f-2b5c954cc4ce.pdf

2 Likes

Promoters have acquired more shares…

http://www.bseindia.com/corporates/anndet_new.aspx?newsid=900d983c-9f94-4b54-ac99-c297f67c09ce

Not substantial but still suggest business going in the right direction…

Disc: Invested

1 Like

Was anyone here able to attend the Analyst / Investor meet in Mumbai on Jan 15th?

The investor presentation doesn’t talk about FY18 quarters. Anyone noticed that?

Apologies if this is a naive query.

I had a short chat with Mr. Shrinivas (IR contact). The notes were made after the conversation from memory and so certain figures may be slightly off.

planning on opening hospitals in MP (indore, raipur), Orissa, Chattisgarh… mainly under penetrated areas

should cost 25 lakhs/bed for a 100-200 bed hospital and 40 lakhs/bed for a 400-500 bed hospital since a larger hospital will have the best technology available

their arpob is already 29000/day in 1.5 year old hospital

5000 beds is the target for the next 5 years

This will require a capital of 1500 cr which they intend to raise through PE funding over time

Within 12 months, they will attempt to raise 100-200 cr and set up hospitals according to that and as they grow in size, they will continue to raise funds

Transferring funds from the US can only be done after paying taxes over there

they see an opportunity in India for tying up with a private Indian bank to provide credit cards through their app

they will ask for aadhar, pan card, bank details, social network accounts to assess credit

banks generally give Rs. 4000-5000 to agents to sign up new customers

in this case, the bank will give 1500 to Virinchi for bringing the client and nothing further for transactions as it will use the free UPI system

currently, credit cards charge 1.5-2.5% to merchants which is shared among the network and the banks

banks will benefit by being able to cross-sell their products…

there are 75 cr bank accounts, out of which 25 cr accounts maintain minimum balance. About 3 cr credit cards held by 1.25 cardholders

This app-based system will target the 23-24 cr ppl who do not have any unsecured mode of payment. (This figure of 23-24 cr is definitely a very rough estimate in my opinion as people have multiple bank accounts)

tyohar foods was a company incorporated by Mr. Kompella because he was interested in starting mobile restaurants for providing affordable food and replace street food. the plan has been shelved.

1 Like

~1500cr fund raising (even over a few years) sounds a lot given their MCap is 300cr+. Large portion of EQ will be diluted in this case. EPS will take a hit. Also in last 2 qtrs, there has not been a material change in hospital biz numbers on a consolidated basis.

In last five years, their revenue grew at a CAGR of ~34% (78.68 cr. in 2013 to 334.4 TTM), PAT at ~48%. For the same period, their debt increased at a pace of ~49% CAGR and equity at ~8%. Their reserves have grown at ~20%. They have diluted equity only once last year (in 5 years) when they decided to merge Bristlecone Hospitals. Much of the growth has been funded by debt and yet they have been able to maintain a reasonable gearing of 0.77. From a period, when operating margin hovered around 15-20 percent, they are now closing in on ~30% operating margin. Given their numbers in past five years, I don’t seen any red flags so far. It gives me confidence about their growth plans going forward. Besides most of all, the management team is highly qualified and would have thought deeply before setting audacious goals.

Still, if you wish to judge them by the flat growth in hospital business for a quarter or two, then you are free to do that. But in my opinion, it would be myopic, and slightly unfair considering their efforts in past few years. If only we allow them time and be a little patient, Virinchi might turn out to be a very long term story and not just a 1-2 quarter kind of blip.

7 Likes

I have posted earlier about my stock buying and reasons for buying. Now, I have sold almost 80% of my holdings in the stock. Still, balance 20% forms a significant part of the portfolio. Reasons as listed below:

-

The stock was a huge allocation for me and after the run-up became a huge part of my portfolio.

-

The Equity dilution did take out a significant portion of growth from retail investors.

-

As stock price went up, the margin of safety reduced and the stock was in the region of being near fair priced. I had missed such opportunities in the stock earlier waiting it to be perfectly priced. The opportunity cost of being invested can be significant given the marginal returns possible from hereon.

-

It seems that rapid growth phase will come down a bit as hospital business will have to slowly grind its way up, Significantly altering the valuations.

-

I think in case of correction stock can be picked up at cheaper prices.

-

As issue raised by vibs6615 , ramping upto 5000 beds is not a easy target to achieve in terms of financing and breaking even, In all fairness, I think unless they acquire running hosipitals or merge with them this target is not reasonable to achieve.

The positives still left in the stock:

-

Hospital business still has a long way to go.

-

Management is talented.

-

Hospital is still undervalued based on acquirers multiple.

-

Huge runway for growth in healthcare.

-

Experience in financial and healthcare data analytics.

My probable future Entry points:

-

Stock goes below 95.

-

Other hospital acquisition to increase beds, or new hospital construction with conservative capital raising.

-

Adoption of downloadable credit card by retail customers.

I don’t deny Virinchi has a tendency of providing deep discounts intermittently. But from a high of 150+, it trades at sub-120 levels, which is a 20%+ kind of discount already. I won’t comment on any further downside potential, but the numbers already reflect deep value in the stock. Its trading at - PE of 11, PEG of 0.33, PB of 1.4, PBXPE of 15.8,Earnings yield of 12%, EVEBITDA of 5.4, Graham Number of 140, MCap to Sales of 0.96. The return ratios are healthy - ROCE 13.8%, ROE 14.3% and CROCI of 16.3%. I do understand completely your reasons to sell and I understand the risks of holding a micro cap as well, but I would genuinely like you to help me understand why you feel it is available at fair valuation with reduced margin of safety, when the numbers tell a different story. The future, although uncertain, looks quite bright given their goals, considering its still just a micro cap. Good managements habitually set audacious goals to the point of being unreasonable (yet achievable) to motivate their human resource to stretch and go the extra mile (Remember the Stretch initiative by Jack Welch while he was transforming GE?). This way, if the workforce achieves even 80% of the targeted goals, its an achievement, and any top up on it is a handsome bonus. Also, do you not think its a bit early to take a call on their hospital business which is fairly new and would take sometime to pace up. Their software division has always been robust and the company is looking to explore future growth opportunities in India. The margins are on the high side and do run the risk of peaking out, but as long as they keep improving the capacity util. of the hospital business, they have enough headroom to grow even without further capex.

In last five years, Company’s highest PE has reached a max of 17.8 and highest PB has been a max of 2.3. These valuations considering the growth of the Company seem pretty reasonable and it gives me a sense that Promoter’s have not indulged in pumping up the stock in last five years. Secondly, if they are hiring a professional agency to look after the investor relations, its a step in the positive direction. If you would have noticed, the average volumes being traded in the market in last 1-1.5 years is much greater than its past average. It shows growing interest among investors. Responding to investor queries efficiently or having a fully dedicated IR team in-house may not be a practical solution for a Company of a magnitude of Virinchi. Lastly, they haven’t even given dividends since 2013, let alone increasing it. With growth plans in place, I wonder if they would be distributing profits in coming years but a small portion in dividend can at best be a welcome step.

Hi Nolan, I agree with your point of view, as stated, I myself am still holding 8% in my portfolio. So you see it was a huge position for me. I sold at 135/- from which point i thought the upside was roughly 30% more, compared to almost 90% return LTCG from my buy price.

I have valued Hospial Buisness at 60/- and software at 90-100. Unless some new initiatives contribute to topline or bottomline the management commentary should be taken with a pinch of salt. I believe when stock goes beyond 150-180 the stock becomes priced as growth stock which cannot be held with a huge allocation.

These are some of my conservative thinking and may be wrong too. But given the market scenario it better to be conservatively wrong.

1 Like

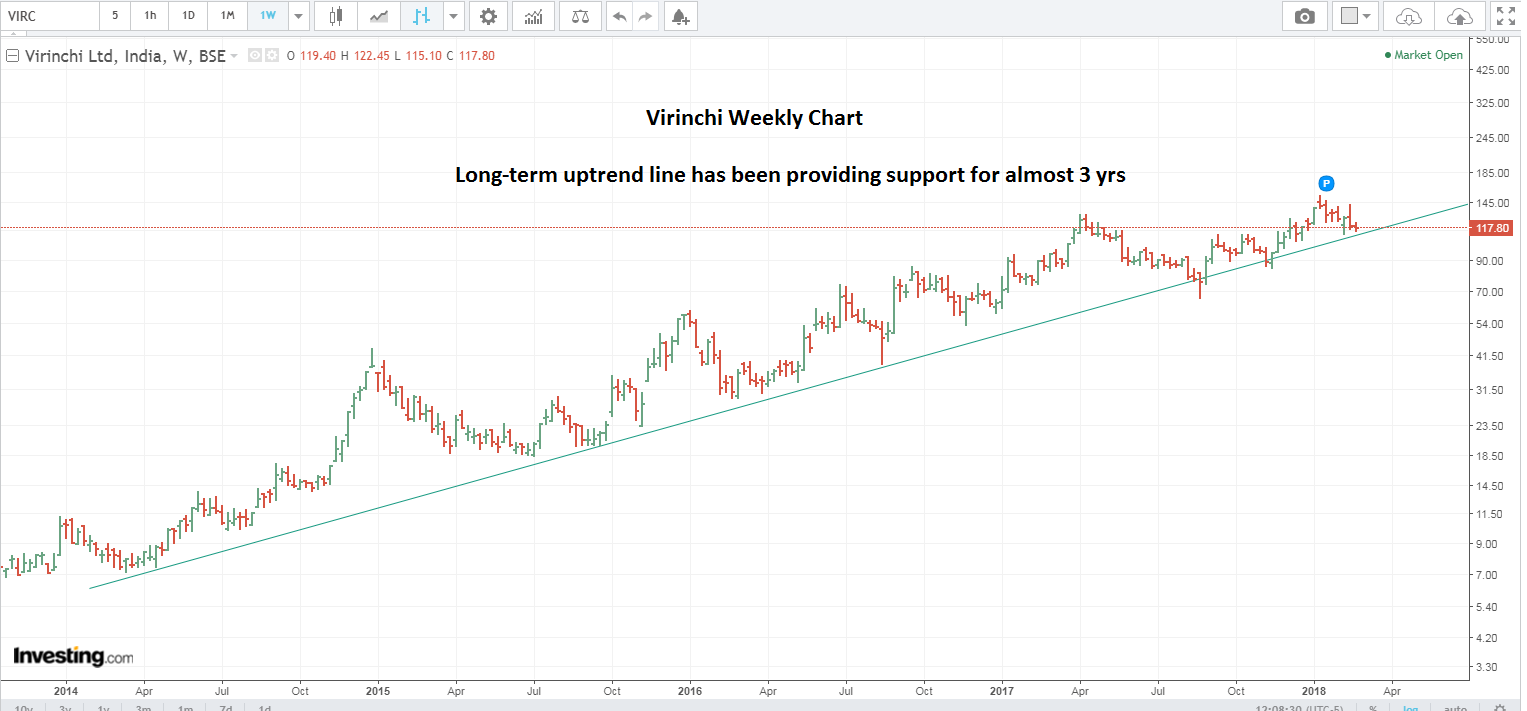

Monthly chart forming cup pattern. Also beautiful thing is that the volume is also forming a cup pattern.

Can anyone able to attend the Investor Call today please share the highlights afterwards? Thank you.

Please share the concall highlights if attended.

Comments by Vishal Ranjan (CEO, KSoft. Head – New Business)

Who is Virinchi?

- Technology company. Business solutions which are technology backed

- Growth verticals – Fintech & Healthcare (both powered by IT knowhow)

QFund Product

- Global leader in software for micro lending industry.

- Serving 20 of 25 top players in US. Capturing 90% of their IT spend.

- We work with NBFCs and run the ERP/loan management system beginning to end.

- Caters to subprime citizens, people who have exhausted all options like credit cards, family & friends etc. These customers have FICO score of 400-500. Conventional banking options not available.

- We look at the bank accounts, see 12 months of cash flows, look at into his address, check blacklisted zip codes, utility payments, what kind of car he is driving? Checks 30-35 different data sources are integrated – decision is made in real time.

- Loan decision made in 2-3 minutes.

- Typical loans - 15-30 days loan. $500-$1000 loan size. 30-35% loan default rates. 300%-350% APR

- 25 mn citizens have gone through our product. Created huge database of customer data, goes into machine learning tool. Gives us 90% confidence on loan decision. Nobody other than us has this data to serve this segment

- Industry has a lot of regulatory oversight due to very high APRs. We get a customization income every time there is regulatory change. Each loan has to be reported to 18-20 agencies on daily / monthly basis for which we get another fee.

Customer Stickiness in QFund

- Huge amount of stickiness to our customers because of our knowledge expertise. We handle the whole journey, integrations. We are the SAP for these customers.

- Did first contract with Advance America 11 years ago. Not lost any customer in last 5 years

- Clients have tried to do in house but have not been able to meet challenges of this industries.

Market share & Competition

- 20-25% of all such subprime loans go through QFUND.

- Monthly 500,000 loans. Will grow higher with Advance America.

- Next competition is 40% of our size. Very tough for them to compete on cost with us.

- Infosys etc. – this is too niche, and domain is too deep to match our service. They can go to a Wells Fargo / BAML and make the entire revenue of QFund through one engagement.

- Consolidated, cash cow position.

- Geographical diversification of QFund to other markets – nothing concrete currently

Advance America contract

- We were negotiating with them for 7-8 months. Got a 5-year contract

- Revenue from this contract will be 250 cr - 280 cr fixed over 5 years. Lot of it is front loaded at this stage.

- Virinchi Product revenue segment – FY 2017 – 92 cr. FY 2018, annualized 126 cr.

- Incremental revenue from this contract for next year FY 2019 will be this year’s run rate (126 cr, minimum) + ~20 cr year. Hugely EBITDA accretive with 75%+ margin. Cost associated with this contract will be only 3-4 cr for initial investment. Should add 13-15 cr ebitda / year for this business (pretax)

- Additionally, will also earn a significant amount of implementation and service income

Healthcare Business

- Huge synergy in technology experience. Democratizing technology in other hospitals.

- At this point see the businesses together. Could demerge in future

- Overall utilization ~30%

- First 3 quarters 14-15cr EBITDA. Improving day by day. Cash flows are breakeven here. (8 cr interest + 4 cr principal per year)

- Apollo’s add capacities. Virinchi wants to touch a billion patients

- See the best model as Business solutions and not a directory service (e.g. Practo). Feel that healthcare a touch and feel business.

- Currently touching 6 cr patients in UP.

- Don’t see IT business subsidizing Healthcare anymore

- Next 12 months – hospital stand on its feet, paying cash flows. Want to run this business better.

- Balance 50 beds completed in this quarter. Waiting for occupancy for expansion for next 100 beds.

Analysis:

Overall, he sounded very bullish about the business. My reading of their comments on healthcare vertical is that they are still figuring out the best model for expansion and the growth has been slower than expected. He mentioned more than once that healthcare business has reached breakeven and will not be subsidized by the core business. Many of the callers were focused on the healthcare vertical because it is new and sexy, but my key takeaway was that the core IT business is significantly undervalued at current price.

Based on back of the envelope calculations:

FY 2018 estimated PAT – 30 cr

Earnings growth rate for current business for next 2 years – 15%

FY 2020 estimated PAT for current business - 40 cr

Post tax incremental margin from Advance America contract is ~10 cr per year

FY 2020 estimated PAT – 40 + 10 = 50 cr

FY 2020 PE multiple – 12x

Valuation – 600 crore

Current market cap – 365 cr

Upside not captured –

- Higher PE multiple than 12x

- Growth of 15% is conservative – last 3 years PAT CAGR is 83% (from lower base)

- Better than expected performance of healthcare business

- Future demerger of healthcare business

Please let me know if I missed anything.

Discl. Invested, adding to my position.

15 Likes