Porinju’s investment theory is completely different. He doesn’t prefer Quality Businesses as upside is limited. He is more of high risk high return. He openly says that.

On the other hand, diversifying from IT to hospital biz is not an easy task as it involves real estate and tremendous money power to go through initial phase. The burn rate (operational expenses) is higher untill you get substantial biz.

AR mentions two companies which have invested close to 11%. It might be worth digging about theses 2 cos.

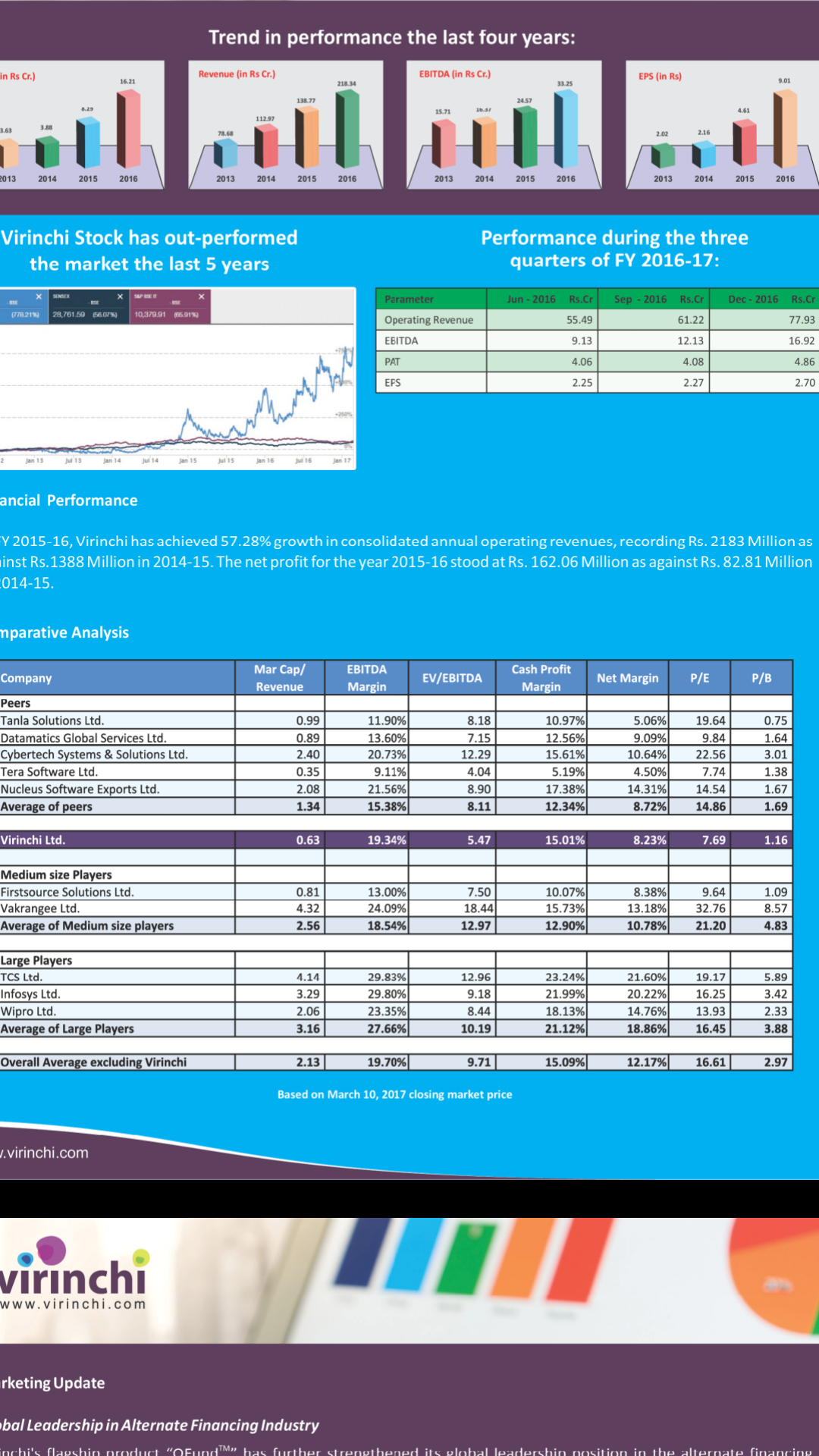

Irrespective of the valuation, I personally am vey wary of companies which do not generate free cash over a long period of time which is happening in the case of this company…Such companies dilute equity or take on debt in their pursuit of growth… look at the debt and share capital of this company since 2007 … that is my major concern

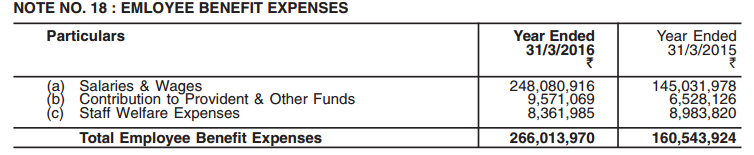

The employee cost of the company consistently stayed in the range of 35 to 40% of sales. This means employee cost almost doubled from 2015 when it was around 49 crores to 92 crores in 2016. But as per the Annual Report the number of employees in payroll in 2015 was 400 where as in 2016 it was 365 as on March 31 2016. Snapshot below.

The median employee salary in 2016 was Rs. 2.81 lakhs (from 2016 AR) . But the average (92cr /365 employees) stays at roughly 25 Lakhs per employee which is quite high for a company that has most of the employee resources in IT . Am I missing something?

If I understand correctly, the hospital launch in Hyderabad was Nov 16, so can’t be the case. The data was for the financial year ended March 16.

I have contacted investor relations about this. Lets see if I get a reply back.

Well it will be better if one can find cons too…

I mean what about Promoters?

Have anyone met or anyone have clarity on it?

Otherwise everything seems positive about VIRINCHI