I am not sure micro caps are allowed in this forum, I am just bringing this company to light.

If against rules this post can be deleted.

About:

Virat Industries is a Gujarat based Textile Company specialized in Sock Manufacturing.

Products: Manufacture cotton dress/casual socks, for Men, Ladies and Children on the latest computerized electronic knitting machines of Lonati and Matec from Italy and KTM from Korea. Socks are manufactured in Cotton, Cotton/Viscose, Wool, Acrylic, Wool/Cashmere, Wool/Silk, Cotton/Silk. Special yarn requests can also be developed.

Markets:

VIL manufactures excellent quality socks for export mainly to the European markets. The Company started its operations in 1995 and has successfully completed more than a decade in Socks business. The socks are manufactured on the latest computerized electronic knitting machines by Lonati and Matec, Italy and KTM, Korea supported with balancing equipment from Spain and other European markets.

Virat plays the role of a Contract Manufacturer who supplies socks against specific orders. Also provide design facilities as per customer requests.

Customers: include John Lewis and Ted Baker in the UK, Migros in Switzerld, Shoe Mart in the Middle East, Puma in the UK.

Production Facilties: capacity is normally based on size, design and style of socks. As per the prevalent pattern of production, the production capacity of VIL is estimated at 6 million pairs per annum.

The factory was designed and engineered by Gherzi Textil Organisation, Switzerland and their Associates Gherzi Eastern Ltd, Mumbai, India. VIL commenced production in November 1995. The project cost was around Rs. 85 million.

Awards: Virat has been awarded ISO 9001: 2008 Certificate by SGS

Winner of the BID Century International Quality ERA Award in Geneva 2013.

Positives:

Low valuations

High Dividend Yield

35% dividend payout and increasing YOY

No debt being Textile Company

Good growth shown recently

Experienced Management

46% promoter share and increasing.

Negatives:

Microcap â Not much information to judge correctly.

Textile Company â valuations may remain low

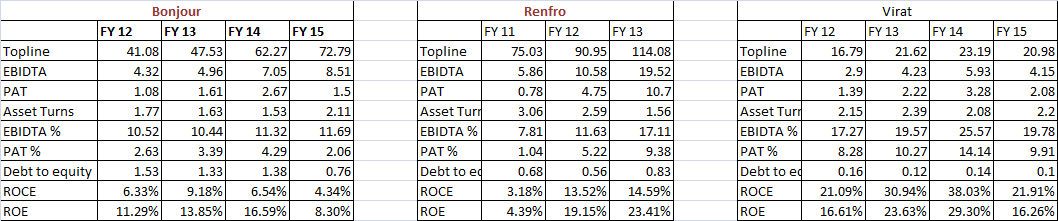

Financials:

|

2013 |

2012 |

2011 |

2010 |

2009 |

|

|

Sales |

20.7 |

16.44 |

14.18 |

13.53 |

13.8 |

|

Op Profit |

3.72 |

2.41 |

0.82 |

3.13 |

3.08 |

|

NP |

2.22 |

1.39 |

0.87 |

1.46 |

1.83 |

|

Sep '13 |

Jun '13 |

Mar '13 |

Dec '12 |

Sep '12 |

|

|

Sales |

6.92 |

5.25 |

5.39 |

5.09 |

5.5 |

|

PBIT |

2.07 |

1.41 |

0.81 |

0.96 |

0.99 |

|

NP |

1.37 |

0.93 |

0.52 |

0.64 |

0.66 |

Last Full year EPS is achieved in first half of FY14.

|

Compounded Sales Growth |

|

|

10 YEARS: |

24% |

|

5 YEARS: |

17% |

|

3 YEARS: |

15% |

|

Return on Equity |

|

|

10 YEARS: |

20% |

|

5 YEARS: |

20% |

|

3 YEARS: |

18% |

|

LAST YEAR: |

24% |

Investing Theme:

Company is specialized in Sock mfg and it is evergreen market like âinnerwearâ

Company is in Growth phase

Opportunity ahead with EU markets showing revival

Good Exchange rate driving profits.

Ref: Company Website: http://www.viratindustries.com

Disclaimer: Not invested yet