Vindhya Telelinks Limited was established in joint sector between Universal Cables Limited and Madhya Pradesh State Industrial Development Corporation Limited to implement a Project for manufacture of Jelly Filled Telephone Cables (JFTC). The Plant located at Rewa (M.P.), India started commercial production in 1986.

The company has since then become the leading supplier of Jelly Filled Telecommunication Cables and Optical Fiber Telecommunication cables to BSNL, MTNL and other leading user organizations like Railways, Defense, Coalfields, NTPC, SAIL, Atomic Energy, Bharti, Tata Tele Service, Reliance Infocom etc.

EPC Division of Vindhya Telelinks Ltd since its inception in 2007 has become one of the leading players for Telecom Network Rollout, also providing solutions for Power Distribution and Sewerage projects. EPC Division has vast experience of working in hilly and inhospitable terrains and has successfully executed several projects in India and nearby countries. The EPC Division has a strong presence in the Northern Region of India and is well equipped to execute the Network for Spectrum Project as per the specifications and requirement of the Defence Services.

Major triggers that can shoot the price of Vidhya Telelinks are:-

-

MP Birla Group company Vindhya Telelinks, which manufactures telephone cables in collaboration with Sweden’s Ericsson Cables had bagged a part of Rs 7,582 crore contract from BSNL to build an optic fibre cable network for India’s armed forces; according to the management this order is primarily divided into two parts; supply and execution of the project, followed by the AMC. The AMC is about Rs 440 crore which is to be done for seven year subsequent to the execution of the project and the project is valued about Rs 1,036 crore. This will be in the name of Vindhya Telelinks Ltd. In the another package, Vindhya Telelinks Ltd is partnering with Larsen and Toubro (L&T) wherein they will be having some revenue around Rs 125-150 crore – that will be in addition to Rs 1,036 for one package.

-

After Rs 1,036 crore plus Rs 125 crore odd, they would be doing about Rs 900 crore for this year because this project is to be done over a period of 18 months, so it will be divided into two financial years meaning this financial year one can expect a turnover of 900 cr + with only one quarter left for results, the combined turnover of the 3 quarter is ~500 Cr which implies that the coming quarter results one can expect 400 cr + turnover with ~10% margin in the profit for a company with just 600 cr market cap.

-

In addition to laying this mega network on turnkey basis in the northern region, Vindhya telelinks Ltd. would also be involved in creating OFC Network in other parts of the country and would be partnering with L&T for the same.

-

The recent bulk deals by Reliance and Sundaram mutual funds at around the current market price justifies the credibility of management and better future prospects of the company.

-

Government is working hard for Digital India Mission and is spending aggressively on Defence by the way of which lot of orders are expected to flow for Vindhya Telelinks.

Promoter holding: 43%

Mutual fund: 4/

FII: 9/

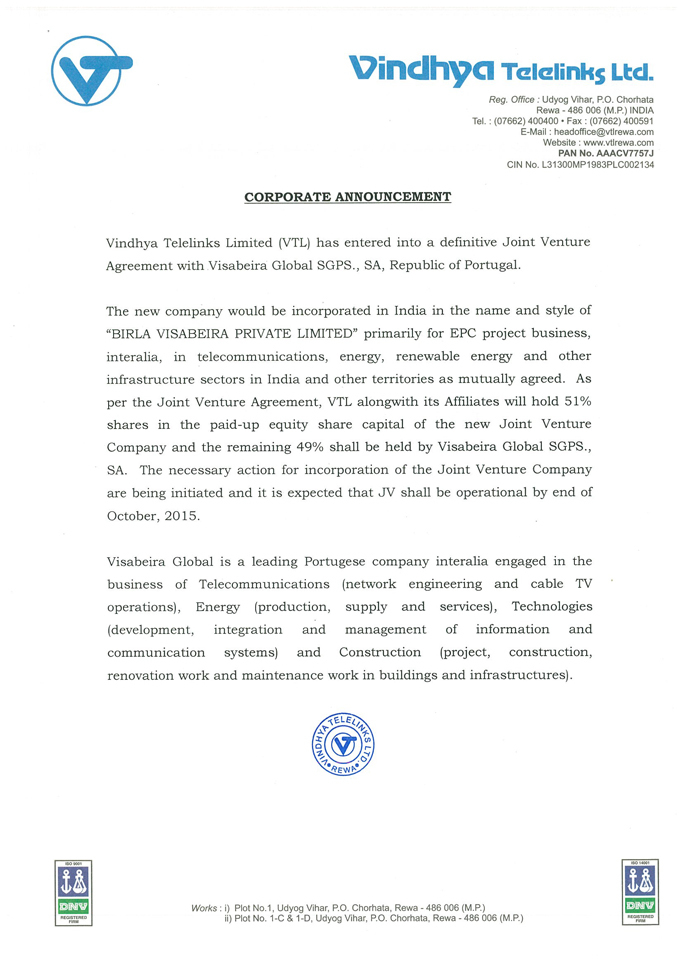

Recent Announcement

Vindhya Telelinks Ltd has informed BSE has entered into a Definitive Joint Venture Agreement with Visabeira Global SGPS., SA, Republic of Portugal, primarily for EPC business.