What is the logic for declaring share purchase in advance. Any such announcement by promoter will lead to rise in price and he would end up coughing more money to buy same qty.

Manish,

I think it is mandatory under new SEBI insider trading guidelines, 2015 to disclose if the quantity is meaningful. Will still try to confirm from my sources. Thanks.

From the latest SEBI Prohibition of Insider trading guidelines 2015

“The trading plan once approved shall be irrevocable and the insider shall mandatorily

have to implement the plan, without being entitled to either deviate from it or to execute any

trade in the securities outside the scope of the trading plan”

See Pg. 12 of the attached guidelines:

3 Likes

I can find following reasons of this action. ( Trading plan disclosure).

-

It may be mandatory to announce such plan to SEBI.

-

You want to give signal to minority shareholder that promoter believe business has value and would like to buy below 500.

-

They may be willing to give exit route to SBI fund which holds 9.9L shares. SBI may be willing to sell out, which promoter is ready to buy.

-

As promoter you know that business prospect is dependent on crude price, which is crashing, you want to give message to sellers not to go short on the stock with your war chest of buying out 9L shares.

I see it as a positive signal.

Disc:- I am invested in it from higher level and my views may be biased.

1 Like

Hi everyone. I am new to valuepickr and I have been recently analyzing Vinati. Has anybody been able to figure out the price and volume effect of their decline in revenue. Based on my understanding, price effect is not a cause for concern due to the nature of their customer contracts, however a fall in volume would be.

I noticed that some people were going to contact IR regarding this. Just wondering if anyone has had any success with their IR communications.

As per this management interview, they’re buying back because promoter holding had fallen to ~72% after FCCB conversion and they wanted to bring it back to the ~74% levels which have been seen historically. Disclosure to bse was made because it is a guideline as per SEBI. Also interview makes it clear that management sees value in the stock below 500 levels that’s why buying back at these levels.

Had a short discussion with the company secretary. Key takeways:

- Some demand on the volume side is getting affected due to fall in crude. I mentioned the point decreasing use of Enhanced Oil Recovery due to a drop in crude and whether that had an affect on demand - he said yes. He did allude to the fact that profits have still increased.

- There aren’t any client churning issues - no client has churned away and moved to competitors (clarified this as it was mentioned in one of the research reports)

- He asked me to check the bse website as they have just submitted a disclosure today. As per the release: “Vinati Organics Ltd has informed BSE that the Company has entered into long term tripartite agreement with USA & Japan based Chemical Companies for supply of a customized product.Due to this turnover is expected to increase by Rs. 45 Crores in Financial year 2016-2017.”

Hope this was helpful.

Regards

5 Likes

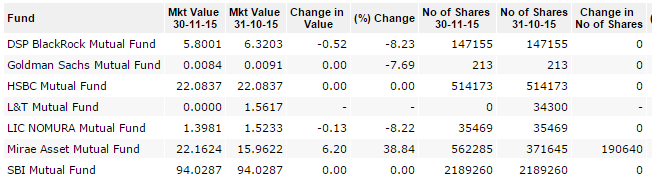

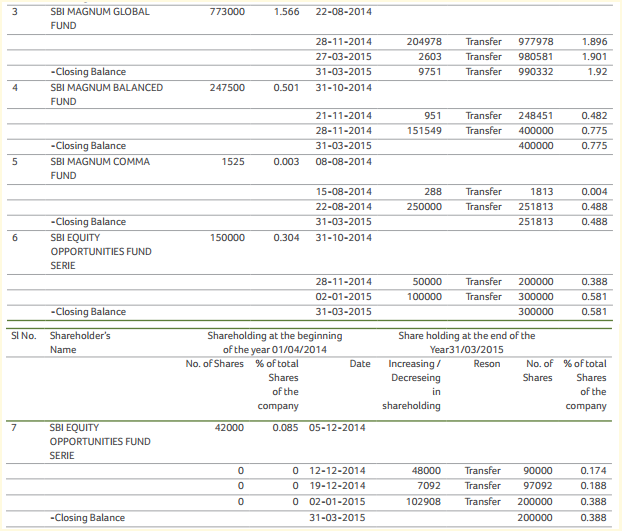

@kkarunakar - regarding SBI MF holding they hold close to 4.24% stake in Vinati…smwer around 21l shares…the holding of 9.9l shares represents only one scheme…sharing fund holding details of Vinati as of Nov’15 from CapialLine…i dont think SBI is looking for an exit…

I think there is something wrong with this data (But I remember SBI taking stake from Jwalamukhi which was actually c.4%)…please see below from BSE (above 1% holding). Clearly SBI is the only one with more than 1% and it is holding 9.9 lac shares. Will still check with other sources and confirm by tomorrow.

Hi Vivek…you are right when you see only SBI Magnum Global Fund holding in isolation which is getting reflected under Public >1%…but other SBI Funds togather holds 21.9l shares in Vinati…if you go through their FY15 annual report, there are 5 SBI funds mentioned in top 10 shareholding…as of March, reported SBI MF holding was around 21.4l shares…hope this clrafies the doubt

1 Like

Perfect Chintan. Thanks for the quick research.

But still logically isn’t it possible that SBI or any other mutual fund might be willing to sell shares from one of the fund or part of any other fund. This is just a possibility. I think signalling to market of undervaluation might be another strong motive though.

Yes Vivek, that cannot be ruled out as @kkarunakar has pointed out…but if you see the Fund holding i posted earlier…Mirea asset has added good qty last month while HSBC continues to hold similar qty as they were holding in Mar’15 AR…both funds now holds close to 1% each…but not getting reported as it has been parked in two or more funds…

i also checked FCCB conversion thing…they raised USD 5mn from IFC in 2011 which got fully converted last year…issued sm 22l shares to IFC at conversion price of Rs 100/sh in Sep’14…and in subsequent qtrs dec-mar…ifc exited fully making 4-5x of conversion price…

now only concern and question is rampup of ATBS - as pointed out by @gagandeep_nanda - crude price correction impacted ATBS sales and its impact on topline growth…margins were held up nicely in 1st half which is smwhat heartening…with crude price likely to remain subdued…rampup of ATBS gets delayed impacting topline growth in medium term…

@Chintan, As per Sep 30 shareholding pattern Only SBI Global fund has more than 1% . Most of the mentioned institution have existed the stock.

See here from BSE site.

You can check Bajaar.me also. Put Vinati name, you will find which institution has existed in which quarter. Hope this helps.

My doubt come due to number of share declared 9L and SBI holding just more than 9L share. SBI is still in profit.

As far as the topline is concerned the company has pass-through clause in the contracts so that they are able to pass on forex and raw material price risk to the consumer, hence as far as the bottom-line growth is fine we should not get worried about top-line (since this is bound to decrease due to lower crude prices).

As far as ATBS application in shale gas and Enhanced oil recovery (EoR) goes, it contributes c.20% of ATBS sales and rest of the 80% comes from various other industries such as water treatment, personal care etc. And obviously as far as they keep on drilling oil (which they are) the demand should not drop so much.

Both these points come from interview of Vinati on ET 2 years back:

1 Like

Yes @kkarunakar bajaar.me only report and compile data as per public>1% as disclosed by the companies…

for clarity i have posted top10 holders as per AR15 which shows there were 5 funds of SBI MF which r invested in Vinati including 9.9l shares of SBI Magnum Global Fund…cumulatively SBI MF holds more than 21l shares…which is getting reflected in fund holding data of Nov’15 which i extracted from Capital Line (hope it is not a violation of VP rules)…hope it helps

@vivek_mashrani thanks

1 Like

Thank for the update guys.

I think information about volume is important as it is reflective of demand for ATBS. Vinati has a strong low cost competitive advantage in the ATBS business. ~56% of the operating profit comes from the ATBS business and it has been the main growth driver in recent years.

If demand for ATBS does not get significantly impacted by the fall crude prices, and the ATBS market continues growing at 10-15%, then it would give me comfort as an investor as I know that Vinati will be able to reinvest (by adding capacity) in its moat, sustain a very high ROC, and grow earnings accordingly.

Vinati is also diversifying into other products that it expects will contribute significantly to its topline, but I don’t know if Vinati has or will be establish a moat in these products.

A company that has a wide moat business, is able to reinvest in that wide moat business due to strong demand prospects, and is trading at 16x earnings, sounds like a bargain.

However, a company that has a wide moat business that it cannot reinvest into, and must deploy capital elsewhere, is a more uncertain investment. In such a case a 16x multiple may not be a bargain price.

1 Like

@veerbhartiya93 i agree and as mentioned i feel that is the only concern…but new supply agreement announced give hope on new products are also getting accepted which might offset ATBS loss to some extent…

Discl: Not invested, but inclined to add

1 Like

Recent management interview on Stake increase decision:

2 Likes

BP Wealth has come out with initiating coverage report on 9 Dec 2015. Will share the web-link as soon as it is available in public domain.

hi guys,

new to this thread. Have couple of queries to understand this business:

-

How easy or difficult is it for customers to change a supplier (switching costs)?

-

Currently, growth of topline is in question mark big time (i believe). On one hand IBB is a mature product and shall face declining profitability. While, ATBS is facing headwinds because of crude price fall. Any idea if company has got any in-house capability to produce new hit products (with sales potential enough to make a difference to topline)?

-

They claim to be lowest cost producers, is there anything apart from backward integration contributing to this?

Thanks

Rajat