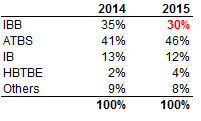

Also, the company is de-risking its product portfolio from IBB and also shifting to higher margin products (like ATBS) without diluting its leadership position.

Below is the % breakdown for revenue:

Also, the company is de-risking its product portfolio from IBB and also shifting to higher margin products (like ATBS) without diluting its leadership position.

Below is the % breakdown for revenue:

Excellent report to understand Indian Specialty chemical sector (though bit old)…covers many important aspects around competition, future growth prospects, industry dynamics etc.

Also covers details on Vinati and other specialty chemical companies like Aarti Industries and Atul Ltd…

http://emkayglobal.com/Uploads/EmkayResearch/Indian%20Specialty%20Chemicals%20Sector%20Report.pdf

How will VOL be impacted with yuan devaluation ?

Vinati sells ~70% of its products on the contract basis (which comprises most of its exports). They keep realizations per litre constant and pass on the exchange rate risk and raw material price risk on consumers.

The remaining ~30% is on spot basis which is primarily to domestic market, hence there is very little impact due to forex fluctuation.

Only thing that will hit the P&L is market to market forex loss/gain on their loan, which you will be able to see in their finance cost.

To put things in perspective, in June-2015 1Q results, the revenue fell but the EBIDTA increased by 22% (due to fix realizations and passing on fall in crude price, also you can see forex losses in finance cost in 1Q result in notes.)

On competitiveness front, China’s export competitiveness will increase which is bit of negative for chemical industry but since VOL has economies of scale and has very low cost base, it is difficult for any Chinese player to compete with Vinati IMHO.

You can verify the details regarding passing on of forex losses and raw material prices in the Pg. 7 of the below report:

http://www.hdfcsec.com/Research/ResearchDetails.aspx?report_id=3008142

Disclosure: Invested and my views may be biased, please do your own due diligence before any investment decision

This article speaks tonnes about the innovation and hard work that went into for production of ATBS:

That was really excellent insight. Thanks indeed.

anyone invested/tracking vinati organics? Does anyone has any update on capacity expansion or new products?

accumulating in SIP mode due to confidence on the management… no idea about expansion…

Hi,

I am actively tracking Vinati Organics. They have recently announced capex plan of 200 Cr in May-2015. You can find the details below:

http://www.nseindia.com/corporate/Letter_to_NSE_270515_05272015124001_1.zip

They are making new plant for IBP which is intermediary for IBB and Ibuprofen. Also, they are expanding capacity of IB for which they have monopoly in India.

I got in touch with Mr. Vinod Saraf (management) to inquire about the progress. They informed that the work is progressing as desired and they are still having some statutory approvals pending for the same. The revenue from this is expected to flow by end of FY16.

Happy to discuss any other queries. Thanks.

Disclosure: Invested

Superb company but too rich at 18x PE.

I would be very happy to pay something around 12-13x PE for such a business. Dont get me wrong, its a superb operation but too rich for me.

Cheers

N.

Hello Vivek,

Its a good business and good management. As you have done such a detailed work on Vinati Organics can you please throw some light on:

Disc: Not Invested

I think valuation is very subjective matter. But to add some points for you to take better decision:

Currently Vinati is trading at 16x 17E fwd PE multiple. If you read the reports which forms this consensus, you will find that they do not account for 200 Cr capex revenue which will start flowing from a year now.

The company has excellent return ratios around 30% RoE and 23% RoCE, just look around in the market and see how are businesses with similar return ratios trading >>> look at La Opala, Mayur Uniquoters, Kajaria, Wim Plast etc.

You find all the points which Graham or Fisher mentiones in their books >>> Dull B2B businessess >> Niche in their business >> Economies of scale >> Well-known among customers >> Expanding market share >> Oligopoly market >> Market leader with competitive advantage >> Good management etc.

You can even compare the return ratios and multiples of its peers who are fairly discovered and having decent coverage like Atul limited and Aarti industries >> they trade at same multiples despite slightly moderate return ratios

The only negative currenly I see is the stock is less discovered, less tracked by brokers and there is lack of communication from management in terms of disclosure, concalls etc

Happy to have your views on above points.

Disclosure: Invested and my views may be biased

Hi Brijesh,

Please see below my thoughts on your queries:

1>> The key products of Vinati are IB, IBB and ATBS. You are correct there could be disruption in terms of discontinuity of use of some products in some applications or fear of substitute. The application of these chemicals are very broad ranging from water treatment, adhesives, personal care, gelatin substitutes, epoxy resin, coatings, construction chemicals, mining chemicals etc. Hence, I believe the threat of disruption is also diversified and suddenly there will be no big impact on usage.

Read: Pg. 16 and 17 of annual report for applications >> http://www.nseindia.com/annual_reports/AR_6524_VINATIORGA_2014_2015_16072015160500.zip

2>> The application of ATBS in oil industry is to act as sealant to prevent leakage during high pressure oil while drilling and doing maintenance. As per my understanding this forms only part of ATBS application and guess if there would have been impact of falling oil prices this would have been evident till now but on contarary the market share has increased to 45%+ during last year. Also, Vinati Saraf has spoke about ATBS application and impact in one of the videos you can find it below:

OR

Vinati Organics forms more than 10% of my portfolio. In my opinion, this stock may not be a multi-bagger within a year but once the capex which the company initiated in last 1-2 years starts kicking, it should improve its earnings on a consistent basis for next 3-4 years.

Is Vinati Saraf Mutreja wife of Mohit Mutreja?

The both are board of directors. Mohit is founder and MD of another company Alphagrep securities (trading).

Yes, Vinati Saraf is daughter of Vinod Saraf (CEO); She is married to Mohit Mutreja sometime back.

Thanks Vivek for providing the updates.

I missed earlier on picking up this great company earlier. I believe here lies an opportunity to pick this for long term now that there is some selling pressure. The 200Cr expansion could be a good risk reward once and if it materializes. Considering the previous experience of the management in reducing the debt they should be able to work this out well.

Disc - Not invested and tracking closely.

Thanks. Absolutely, by current pace of repayment, they should be debt free by FY2016 or latest by 1H 2017.

Also, given the track record of succefully completing capex, I believe they should be able to do this one in timebound and efficient manner.

Vinati organics reported its quarterly result today…

Overall, flat quarter on Q-o-Q basis and muted growth I believe.

Disclosure: Invested

Good improvement in Balance sheet.

Debt reduced, current investments have improved a lot.

Good jump in Capital WIP also.