HI Dhiraj Bhai,

Sorry was travelling, hence could not reply. Thanks for writing. Your points are very much valid. I had similar concerns as you have raised regarding tax payments, ESOPs, etc. I did inquire about them with the management when I met them. Here is my understanding about each issue.

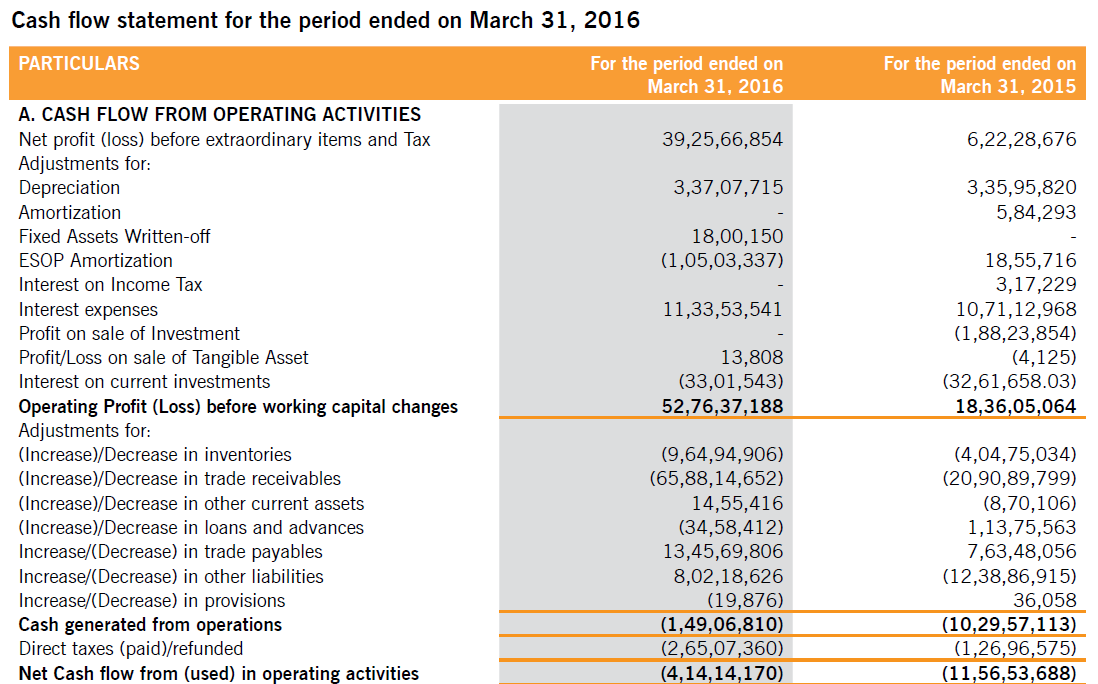

1). Tax payment - Yes, they had liquidity issues last year. They couldnt pay full taxes to the IT authorities. Their 50% sales were held up in debtors and the rest of the funds were either reinvested in growing business or paying out expenses like salaries. To this justification given by Mr. Vikas Garg; I pointed him out the necessity to pay dividends in such scenario. He said, it involved an outgo of 1-2cr only and the decision was taken from the shareholders perspective. I was not convinced with that answer. Rather they should have pad 2 cr of taxes and reduce the liability. This was a case for capital mis- allocation. Vikas Garg took salary of 3.6 lacs only. Dividend was the way out for him to sustain his lifestyle - “backdoor salary”. However, company has paid all its tax liability of 15-16 and have been now paying all the taxes in advance. Any company having a new business would face such a problem in the initial years. I have personally visited the facilities in Shajanpur, cross verified with the President of All India Plastic Association and with the China guy whose company is into MTM and enjoys leadership position in China. So the business is real and genuine. Every startup takes time to generate positive OCF. This is a case of transformation from trading to manufacturing.

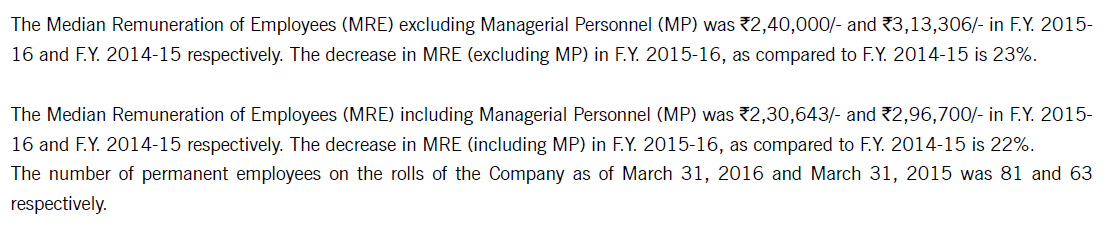

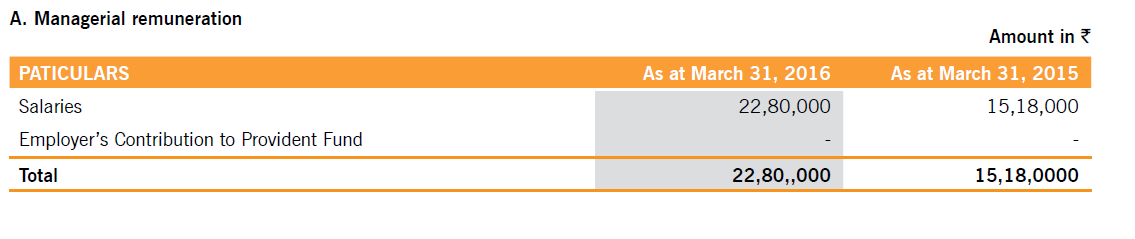

2). Median Salary - Number of employees have increased from 60 to 80 in one year, whereas the median salary has decreased. This is a limitation of median method. If the additional employees are hired at lower levels in the organisation, the median salary point will move down and not up. I confirmed with the IR. He said almost 18 of the newly hired are hired at lower levels in the organisation. Coming to the point of median salary with managerial remuneration, Mr. Vivek Garg earns NIL salary and Mr. Vikas Garg earns 3.6 lac. Again, if we use the median method to calculate the median salary, the amount is going to shift down rather than go up. All the middle level managers are earning far more than the MD. Vikas Garg shared his views of creating his wealth through growing his business and increasing his Market cap rather than taking salary. On the other hand, he must pay all his managers good. So, Mr. Ashutosh Kumar Verma is paid 16lacs (approx) and all other managers are being paid average 8-10 lacs. It is just because the total number of managers with salary of 8-10 lacs are far less than the employees that are paid below 15000 pm in the total count, the median salary slips down to such levels. Ashutosh Kumar Verma is the R&D head and he is getting paid respectable salary. I have seen their R&D dept. You must always discount 20% of what mgmt talks in the AR. The rest 80% is very genuine. You may check the linkedin profile of Mr. Ashutosh Kumar Verma and his ex bosses and colleagues commenting on his work. Plus, MTM is a purchased technology. So R&D has been done in the TPR and TPE part.

3). Restructuring - Vikas Globalone is not another group company. It is the old name of this company. Restructuring has been done in past, which is better for us. Company had invested in a partnership firm and one another company. Due to this there were many related party transactions. They actually decided to consolidate the operations. Today the financial statements look more transparent. Zero investments in companies and far lesser related party transactions.

4).Disputed Statutory dues - I think this is a pure business issue that occurs in every other business. The amount is small and is under dispute.

5).EPF for top level managers - As per EPFO guidelines - contributing to EPF is mandatory for the employees who have a basic salary plus dearness allowance up to Rs.15,000 (earlier it was Rs.6,500). And those who are earning above Rs.15,000 may contribute voluntarily. Does this case fall under these guidelines?? I have not checked this with IR or mgmt. Will come back on this. But, do you still consider it a red flag?

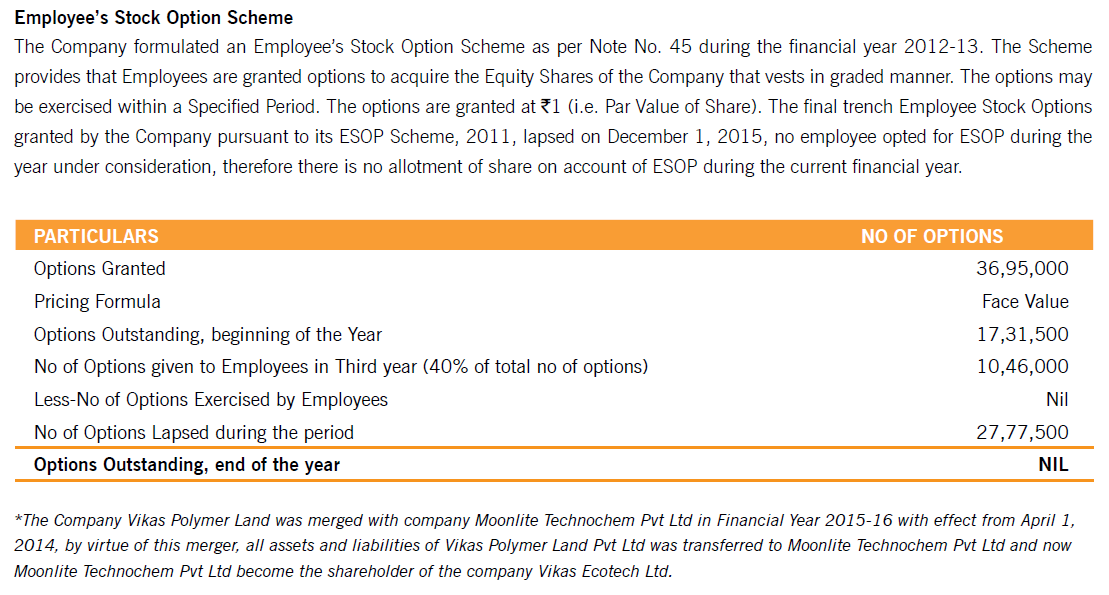

6). ESOPs - Good point. I agree to your concern. It should have been transferred to general reserve. The profits got inflated by 1cr. Would send this concern to the mgmt along with the ICAI guidelines on the same so that the same can be forwarded to their statutory auditors.

7).Export Incentive - Can you please clarify further on this. Did not get your point.

8).Acturial Gain - Acturial Gain booked is not 1.2 cr but 12 lacs. (correct me if I am wrong). There are two set of assumptions - financial and others. Financial assumptions include discount rate, salary hike %, etc. Others include attrition rate. Attrition is very high at the lower levels due to which the PBO keeps on changing. If an employee does not stay for 5 years, he would not be eligible for gratuity. Since a lot of employees left job within 5 year period, company had to reverse the PBO (liability) booked and hence acturial gain. I confirmed this case with the mgmt. Would like to have your views on this. Do you still see a red flag?

9). Real Estate Purchase - I need to check this with mgmt.

10). Break up of trading and manufacturing sales is not provided in AR. However, they have provided the same in the Investor Presentations. You may refer that.

11). ESOP lapse - In AR 2013-14, the top management/executives have applied for ESOP (656000 shares). Ashutosh Verma and all the top executives have got ESOPs. All the rest ESOPs were available to middle level managers. This is a concern and I agree to your views. I need to get justification from the mgmt on this.

Overall, I find this story good and the mgmt running the show genuine. I have done cross checks at the ground level. The product is genuine, their main customer is having 8% stake in their company, the competitor in China is well aware about Vikas Ecotech. It is transforming, and the road is not going to be straight.

Disc - Invested and a major position in my portfolio. These are purely my views. Please do your own due diligence.