There seems to be lot of hype. 2 of the guys I follow on MC have put in 25% of their portfolio in VEL. Its making all the right noises. If the Q2 result is anything short of spectacular, the bubble could break.

Vikas EcoTech Ltd has informed BSE that the Company has constituted an

Advisory Board consisting of eminent personalities with the purpose of

providing guidance and act as a sounding board to the senior leadership

team in the company including the Board of Directors.

The nature of the board is non-statutory status and members will be invited to join

the Advisory board based on past credentials.

Shri G.N. Bajpai, ex-Chairman SEBI & LIC is appointed with his consent as the first

Chairman of the Advisory Board. The Board will consist of other members

by invitation who will be people of eminence from the field of finance,

engineering, general management, marketing & branding, legal, etc.

The Advisory Board will guide and advice the Board of Directors on various

strategic business decisions in a more rounded manner. They will also

share best practices from the outside world for organization learning

purposes.

source: http://www.moneycontrol.com/stocks/stock_market/corp_notices.php?autono=5230301

Extremely surprised to see equity dilution on this counter. Why would a company that is growing at such a rapid rate opt for this? Aren’t they harming their own stakes?

Last when we spoke to them, they needed money more for Working capital rather than actual Capex. It would be good to know as to where this 80 odd crores is going to be deployed?

Any info about meeting

Vikas EcoTech Limited has informed the Exchange regarding outcome of meeting of the Board of Directors of the Company held on October 27, 2016.

Hi Abhishek, i appreciate your efforts and would love to read your note. Can you please mail me on padisudhir@gmail.com? thanks, in advance.

Vikas Eco Result out… Good numbers. Net profit more than doubled.

http://corporates.bseindia.com/xml-data/corpfiling/AttachLive/EC67DF03_FCA6_465E_8D02_3DDB6138BD75_174903.pdf

Disc : Invested

1 Like

Please note my email id - anup.agarwal47@gmail.com. Abhishek your efforts are highly appreciated. I am planning to put some money in this stock.

Hi Abhishek, I would like to read your note to take decision. Can you please mail me at n.arvind2k@gmail.com ?

Thanks in advance.

Disc: Not invested. But planning to add based on the note.

Curious, strange reason - Vikas EcoTech Ltd has informed BSE that in pursuance to the special resolution passed by the shareholders of the Company on November 23, 2016, the Board of Directors had issued letter of offer to the specific investors to subscribe the shares on preferential basis.

Further, the Company has informed that all the four investors, to whom the offer was made in accordance with the aforesaid special resolution, have conveyed their inability to subscribe the shares. Hence, the Board of Directors would not be issuing any shares on preferential basis in pursuance to the aforesaid special resolution.

2 Likes

Hi Guyz,

I met the management and visited the factory couple of days back. I have attached my report on the company. RR - Vikas Ecotech.pdf (1.3 MB)

Disc - Please do your own due diligence. The assumptions are purely mine and may turn out to be different. Take your own decision.

15 Likes

Thank you … I appreciate your efforts …

1 Like

Superb,Keep up the good work.

1 Like

Abhishek - did you have any discussion with respect to the company’s plan for eliminating debt (if at all)?

Hi tushar,

The company is still in its growth phase…in FY18 they said…they will generate positive OCF…once that happens…repaying debt should be soon…since business is only working capital intensive and not capex intensive…it hardly needs 10 CR for capex every year…as per my assumptions business can make OCF of 40-50cr in fy18…so deducting 10cr we still have 30-40cr left out with which we can repay part of the debt…

Again these are assumptions…nothing has been told by mgmt on this…

Hi Guyz,

Met the President of All India Plastic Association - Mr. Atul Kanuga. He has a factory in Ahmedabad. He manufactures plastic granules used in manufacturing Pipes. The following info was gathered from him -

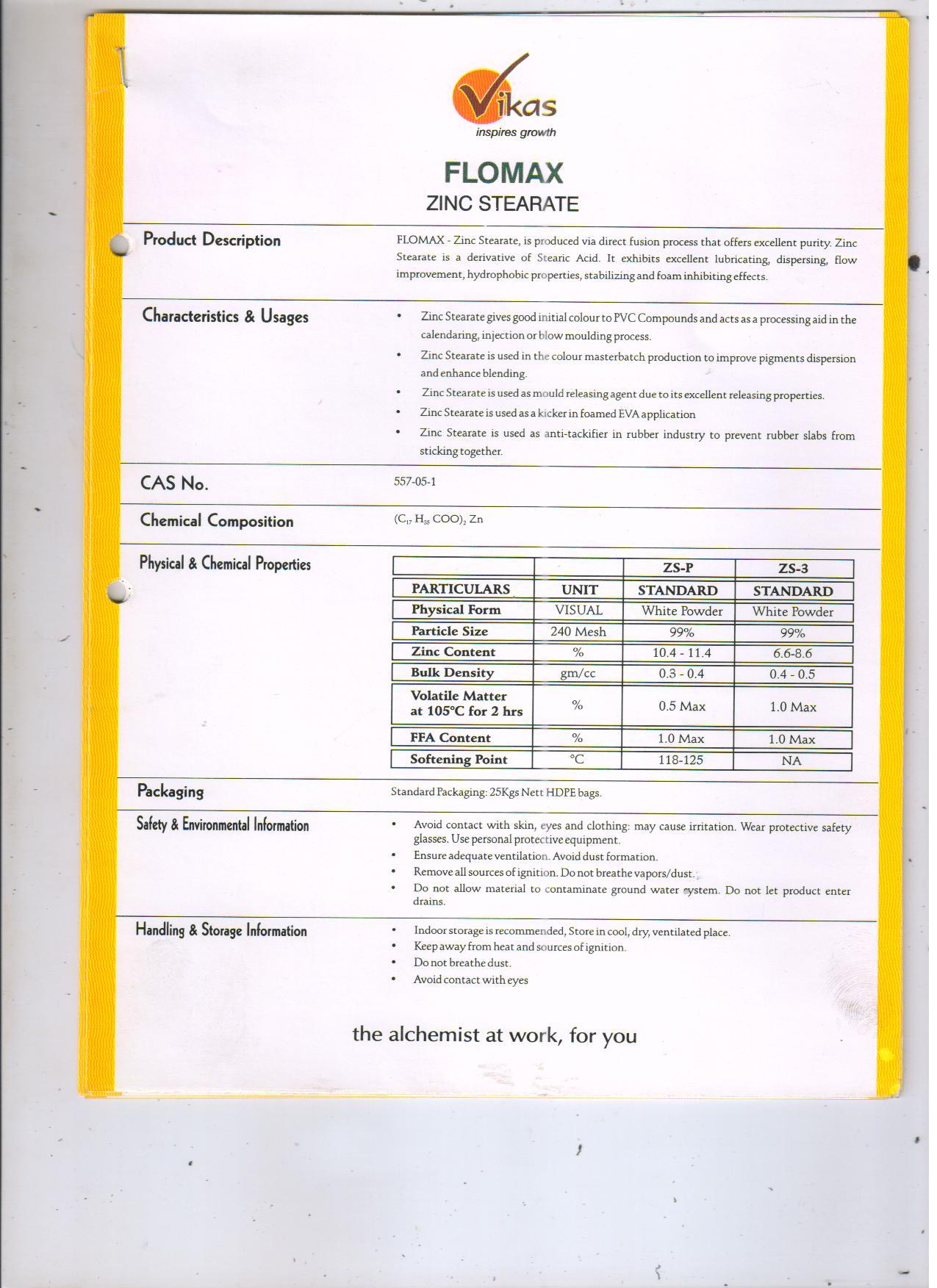

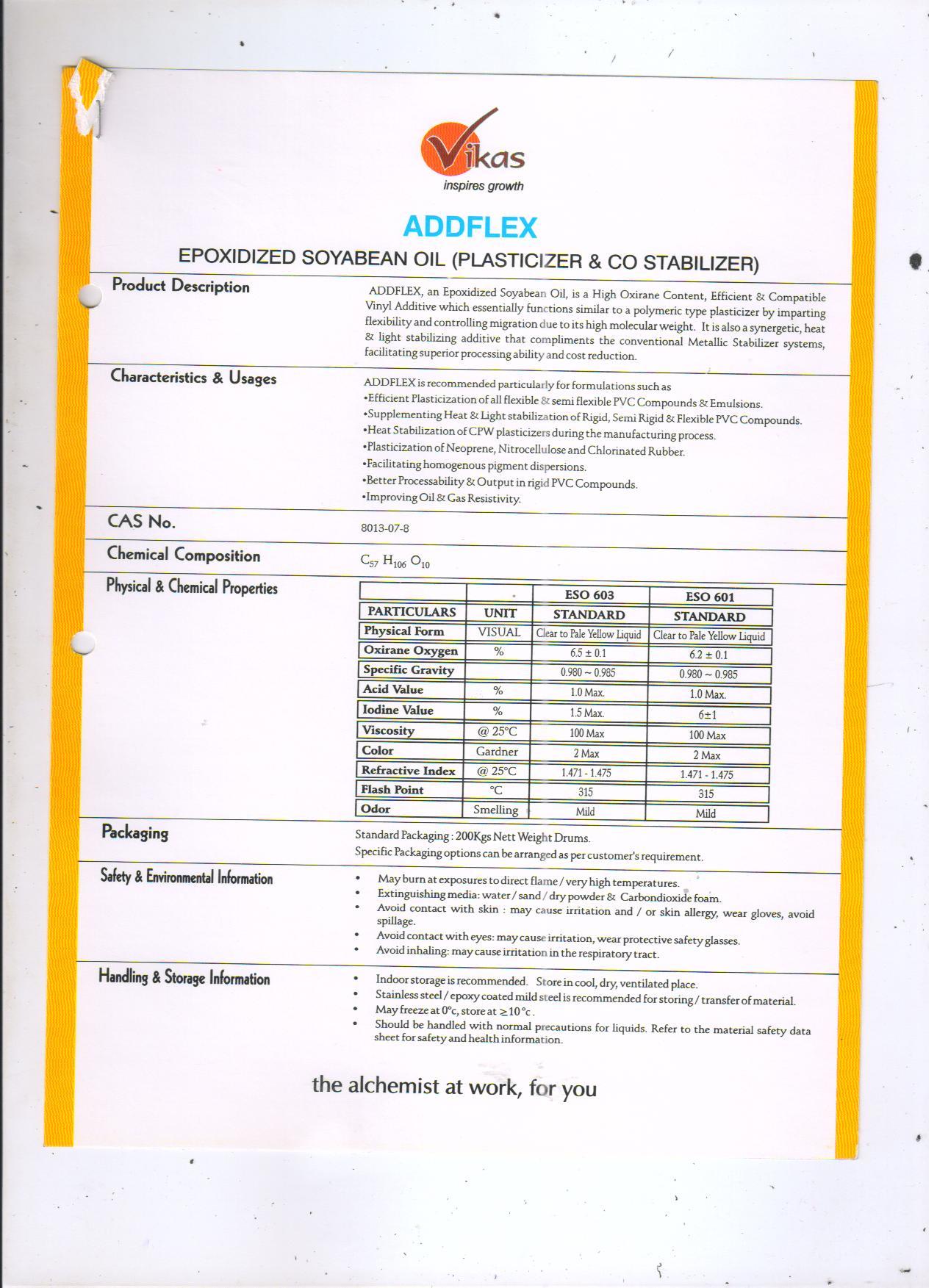

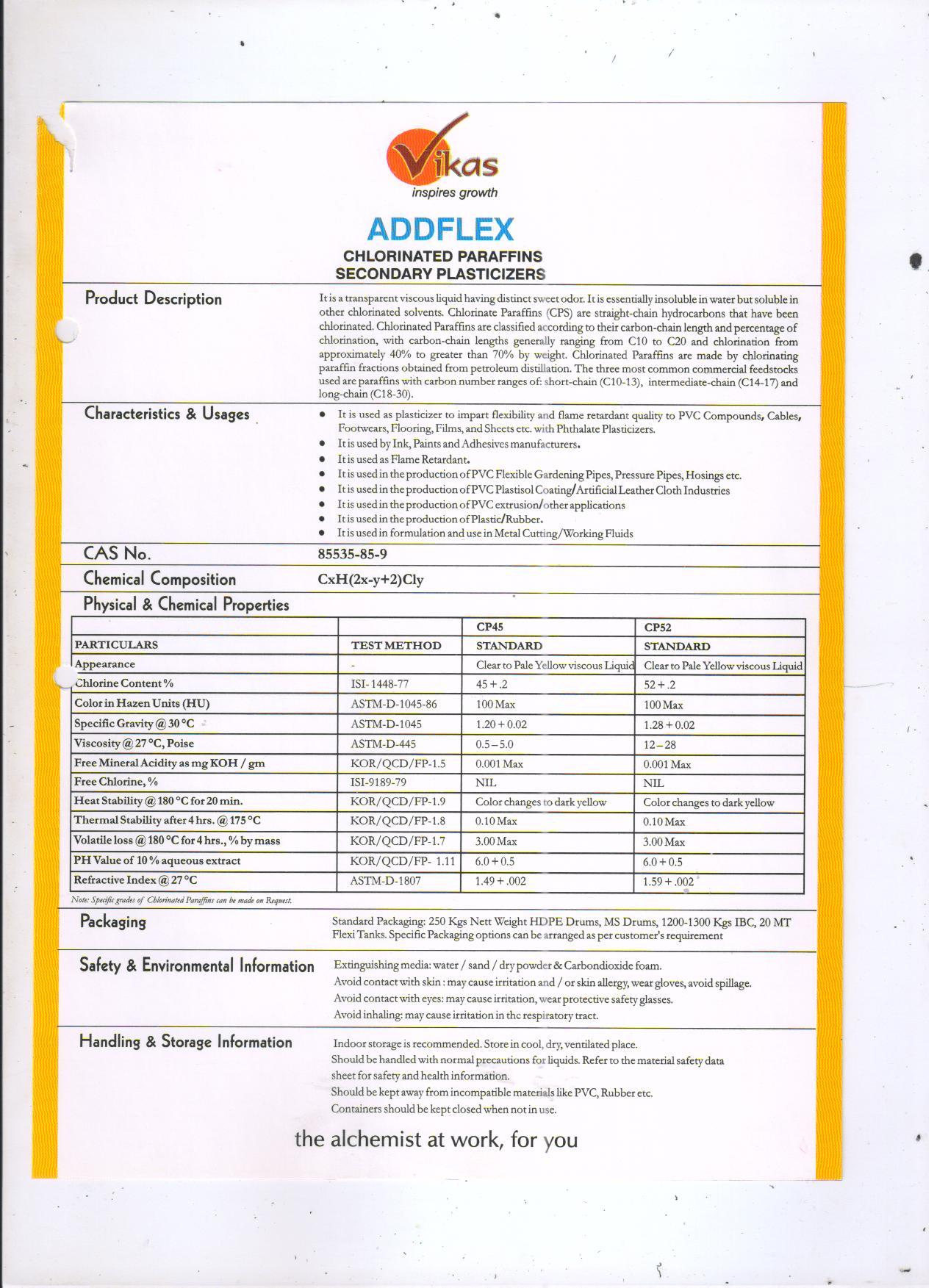

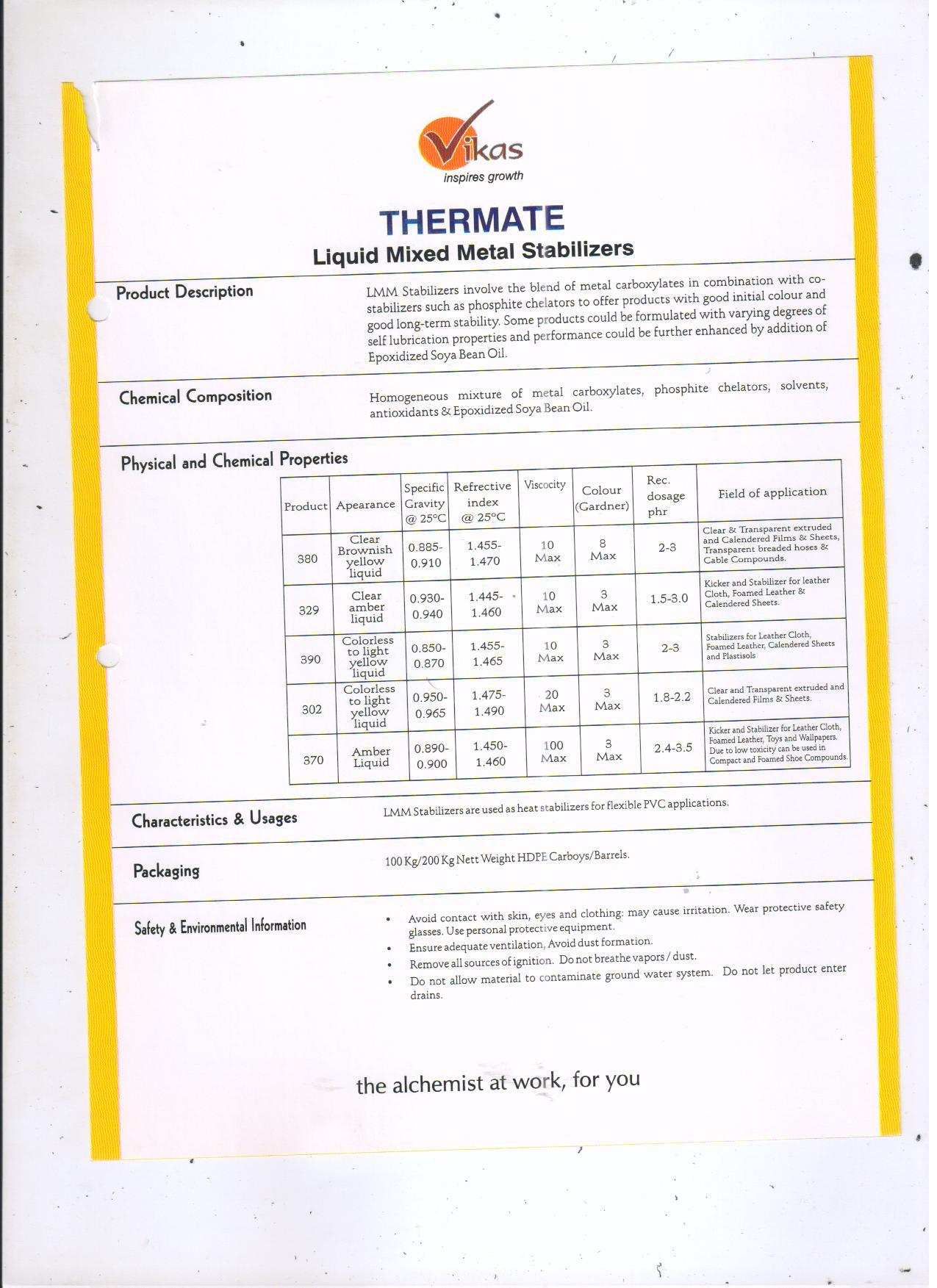

1). He uses MTM from Vikas Ecotech. He said Vikas Ecotech is now some what famous player in the pipe industry. There was a plastic exhibition on 24th Dec in Rajkot, where Vikas Ecotech had made aggressive marketing and advertising.

2). But, now he uses MTM manufactured by company called " Gold Stab". The distributor of this company is his friend and the company wants to penetrate in the market and since Mr. Atul is the president of the industry, they sold him the MTM at cost to cost. Mr. Atul said, he took MTM from this new company purely because his friend was the distributor and the price is cheap (because sold on cost to cost basis). Else, Vikas Ecotech is cheaper than this new company.

3). So, now who is this new company. This company (as Mr. Atul confirmed with his distributor friend over phone in front me) is an Indonesian company exporting MTM to India and the Indian company Gold stab does the selling part here. So, the production is done out of India and hence customs duty is levied. Now, this is a threat. Why? This can be replicated by all other players (those in China) to explore the Indian market.

4). But, then, there are only 7 players worldwide to manufacture MTM. So, even if at one point of time 7 players come in competition in India, it is going to benefit by expanding the market rather than price wars. The size of the opportunity is too big.

5). Most of the (60%+) players still use Lead based stabilizers. The price of Lead based stab is 190 and MTM is 450+ - more than double. This is the main reason for low awareness.

6). Shital is nowhere in this industry. He said Shital has neither approached them nor done any marketing in MTM. The distributor friend, told that he knows only one player - VIkas Ecotech in MTM in India, and said shital is not a serious player with complete technology.

7). CPVC application is growing very fast. Industry is changing from UPVC to CPVC. In CPVC, it is compulsory to use MTM. You cant use Lead based stabilizer. Also, confirmed, that in CPVC application, the dosage of MTM is 3 times. Astral is aggressively marketing on CPVC. This can be huge positive.

I have attached, the marketing brochures published by Vikas Ecotech distributed by them at the Plastic exhibition on 24th december. I got them through Mr. Atul.

20 Likes

Excellent work! Much appreciated

1 Like

that is an excellent work abhishek

1 Like

Hi Abhishek,

I read your posts on ValuePickr on Vikas Ecotech. You have done deep work on the company and met the management as well.

Just wanted to know if you got any convincing reply on the debtors issue from the company… 5 months of debtors in a business in which there are not many suppliers is very puzzling, even though the relationships may be new for MTM product.

Thanks,

Vinay

With reference to your message, I would like to post my view point…

It is not that the product is new or the competition is nil…in fact competition is huge…from Chinese players…Chinese products are 5-7% cheaper even after customs duty…imagine if you have to penetrate this market you have two options…either compromise on margins or compromise on working capital…this business model is still evolving one and one can’t compare this with a mature business…theychose to compromise on working capital…even their product is very new…their customers want to see how the product works…this can be seen only after 5 months of using their product…it takes hell to convince big players like prince and finolex to use ones product…Infact the quality of their debtors is better today because of big clients…it’s basically a working capital intensive business…what if the business is capital intensive…needs more and more fixed asset investment every year…like cement co?? We donot doubt the genuiness just because we see the OCF positive…we forget a huge negative figure in cash flow from investing…do we even think if all the money that the company says they have deployed have actually deployed in the business?? Have they actually bought plant and machines??just because it is a working capital intensive and a business with new product, generating negative OCF, we start doubting the numbers?? Even today on an average almost all the chemical co are having debtors to sales close to 25-35%…what is important is free cash flows…very few business generate free cash flows…it is that this level that the business really generates cash…else all other time it is simply re investing, either in working capital or in capex…lets imagine if the business doesn’t grow next year, what will happen to the OCF?? So if business made PBT of say 100cr last year, with no growth it will make 100cr this year also…since there is no growth, no additional investment will be required in working capital…and hence this entire 100cr will fall down to create 100cr of positive OCF!! So at no growth business is generating 100cr in cash from operations…and since company doesn’t have much capex requirement, company will start paying off it’s debt…and company becomes fancy of investors…I am not trying to favour vikas ecotech…Forget vikas ecotech…take any company…what if company A declares that they are going to deploy 1000cr over next 3 years (when today they balance sheet size is 500cr)?? How will investors react?? It’s a wonderful investment opportunity!! Now there is another company B, which is working capital intensive but less capex intensive, and it declares that we want to reach to a top line of 1500cr in next 3 years, when there top line today is just 500 CR…and they will do this by launching certain new products…so how will investor see this?? Now imagine additionally that both the businesses are faced with immense competition…would you bet on company A or B??

I would bet on company B which is working capital intensive…what if the business can’t withstand competition?? I am better of with working capital investment which I will anyhow get back eventually rather than investing in plant and machinery and selling them all at scrap value eventually!!

P.s.- these are my views, and do correct me if I am wrong in my understanding…

6 Likes

Excellent Work Abhi. Havent invested in Vikas at the moment, but it seems to be a consistent fav of the stock forums all around.

1 Like