good point ! For that we really need to asses management.

Management with growth mindset will re-allocate extra capital earned from existing businesses intelligently, (I hope that happens. )

for that one has to see the track record of management.

The Company was incorporated as Valiant Organics Private Limited on February 16, 2005, Till 2016 they did nothing much if you see. On 2016 they planned CAPEX because of Chinese competitor were forced to close down. Definitely they are opportunistic but they are not opportunity creators in my view.

Promoters are old now, If Aarti guys take over this company i feel then we can expect growth from new avenues.

I think merger with Abhilasha is a sign they are looking outward ( may be Aarti involved here too ). I hope they continue doing that.

It was nice playing devil advocate with you, important to think all the aspects.

If you look carefully into the board of Valiant, you will find one or two people that are young. You will also see, going into last 2 years history, about some persons exiting the company. Look into their background. You will get insights on whether someone is being groomed to take the business forward. You mention that promoters are old, but you have not done any research into who is on the board and what their connections to the family are.

You say that the company did nothing till 2016, but do you have an understanding of what their capacity utilization was up till then? When did they business really start getting traction? I can incorporate a company today and keep it mostly dormant for 5 years. After 5 years, for year 5-10 I can start actively growing the business for demand-supply reasons or any other number of reasons including the promoters being more involved in their listed company i.e. Aarti. Does that mean that you will not invest in my company because it started growing only in the last 5 years?

Do you look into the operational history of all your investments? Now if you go back and do this analysis for your other companies and find that in its first 5 years nothing much happened but in the next 5 it grew 10 times - will you take that as a negative sign and just exit? What kind of rationale is that? Almost every company listed today had a period of no traction for many years after incorporation. How do you deal with that in your investment thesis? Is it even worth considering?

Yes , I get your point. My point was they are not like Ajay Piramal for example. They started a business without knowing how far it could take them. What if the chinese thing have not happened ? Then it was a bad choice to start with.

So the question is would they take intelligent decision in future ? or things will again depend on luck.

I want to ride with a management who creates opportunity, I am not sure these guys are really like that.

This is all i am discussing to make sell decision ? Stock is still fairly priced but if Mr markets gives you 500 Cr Mcap today would it makes sense to sell ?

I think yes, Because although i think business is good ( they earn very high return on capital) but i am not sure about what’s next bcoz there is a chance that good thing might happen and bad thing might happen as well.

but if the Jockey is good ( that i am not sure about) i would not sell even at 500 Cr mcap because that jockey will perform in many other races ( businesses) .

The jockeys are experts in complex chemicals and Valiant has their entire distribution network to sell the products. The jockeys have grown their stock 44 times in the last 10 years. The jockeys business also did not grow for a few years from time to time.

Regarding Piramal - the whole hoopla on the company has been created in the last 2-3 years, and for good reason too. You wouldn’t have found the kind of talk you hear of Ajay Piramal some years ago, even though a few knew it. You have a lot of hindsight bias, try to get over it to see where wealth creation will happen. Not saying Valiant is the one, but you’re coming to the table with preconceived notions not based on fact or logic.

@AmitContrarian - if you see stock charts of many great companies which have grown from small to mega, you will find hockey stick patterns, dormant for many years and then increased exponentially. Reasons for such exponential increases - company performs x stock rerates. I have lost many opportunities by selling too early in last 2.5 years - Thirumalai (10x), Piramal (3x), TCI (4x) & many more. So gaining from previous experience, I have realized

Invest atleast for 3 years - even if the stock doesn’t perform (we have performer here atleast for next 4-5 years, conservatively we foresee profit of at least 2.5x in next 5 years, atleast double in 5 years - 15% CAGR )

Dont sell compounding machines unless extremely over rating - 60+ PE

Good companies will always be trading at higher PE multiples.

It is not possible to catch top or bottom of stock everytime & re-entering is even more difficult after selling especially at higher price. So best way is to buy and hold

Story can be rechecked periodically, but run through the entire growth cycle of the company and don’t sell early. Stocks can be sold when growth stagnates but ride through the growth cycle. We are just at the start of the growth cycle at this counter.

The post is not meant to change your mind (as I know it is extremely difficult to change somebody’s opinions) but to learn from mistakes of others.

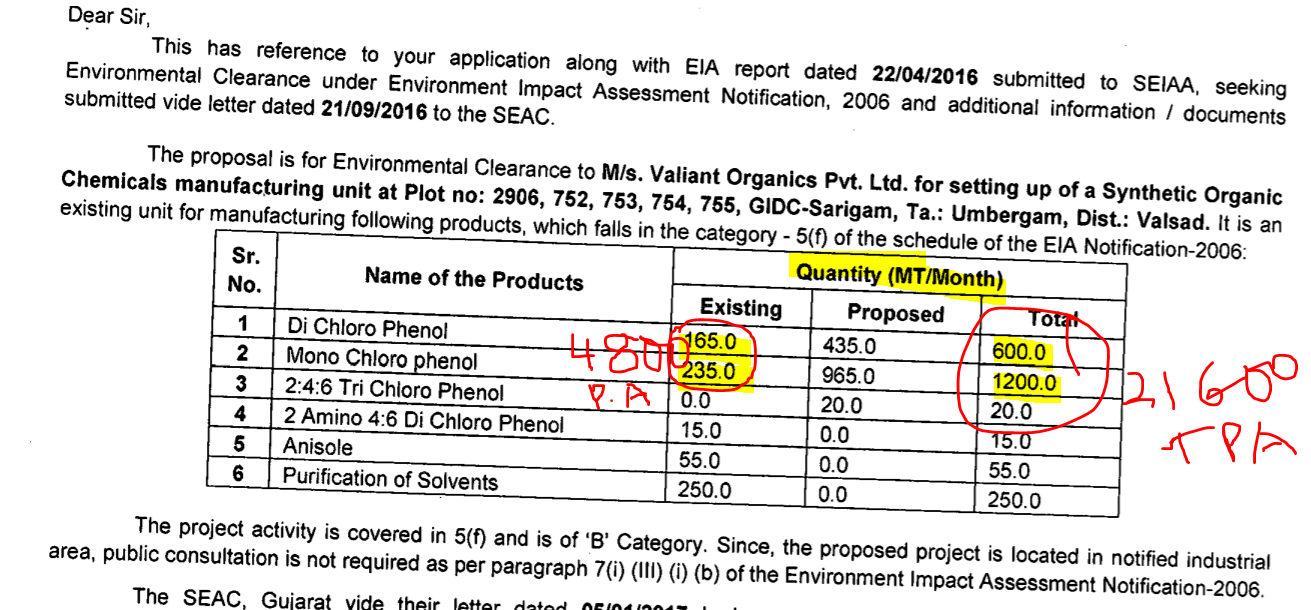

I was going through earlier discussions, seems like capacity now should be doubled of FY17. Lets see how p&l numbers looks like by FY18.

Earlier we had this discussion about are margins sustainable

They had applied for the entire proposed expansion to take the capacity to 21600 tonnes as stated in the prospectus. Would be adding 4800 tonnes per annum capacity per year. They have adequate land adjoining to existing plant to take care of the expansion.

I came across this forum through a Twitter reference and have much to thank the contributors here!

This is my first post here and looking to contribute my own two cents on the companies researched here.

Coming to the original post on this company:

I was wondering if we have more data to support this assertion. I tried finding info on the internet about the demand for Chlorophenols but very limited research available.

Considering the wide usage in agro-chemicals, pharma and drugs industries, demand should be steady and non-cyclical but would be more comforting to have data to support this.

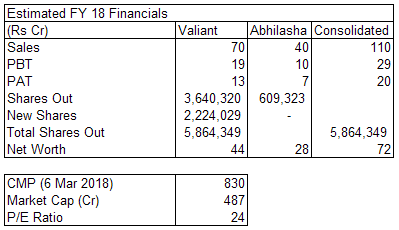

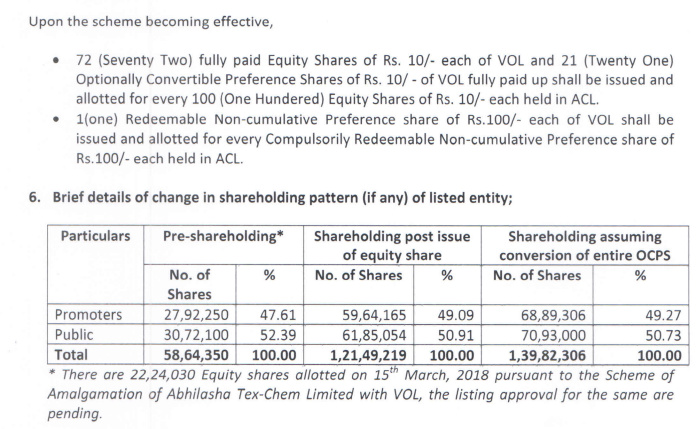

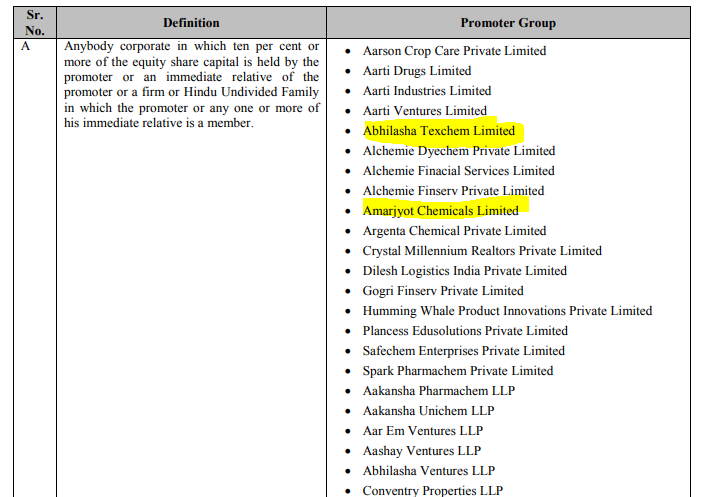

Valiant will issue 365 shares for every 100 shares of Abhilasha. financials of Abhilasha are available here.

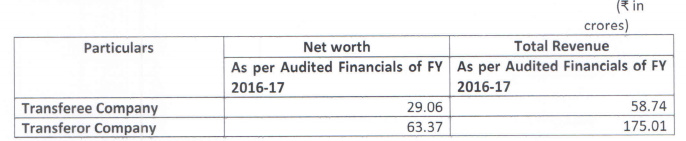

Overall, Abhilasha appears to be similar to Valiant in terms of business and profitability. Merger has closed and results of March 2018 will reflect financials merged entity.

Abhilasha numbers are available upto Sept 16 and Valiant Numbers are available upto Sept 17. I have used my own estimates of growth for both the entities and came out with estimates for FY 18.

As with any estimates, there will errors and actual numbers may be significantly different from estimates. However, a rough estimate will help in valuing the company especially since there is a significant dilution happening due to merger of Abhilasha.

Source: BSE, Author’s calculations.

Note: Market Cap is based on total shares outstanding after merger.

Valiant is diluting 60% stake to merge Abhilasha. In terms of sales, profit and net worth, Abhilasha is also about 60% of Valiant so pricing appears to be in line with fundamentals. Since Valiant shares have rallied sharply over the last 18 months based on the optimism about proposed expansion, it has also revalued Abhilasha. However, there is no planned expansion for Abhilasha. In % terms growth of merged entity will be less than growth of Valiant alone.

Merged entity will have an impressive 32% ROE and will be debt free. Given the growth potential and excellent fundamentals, valuations appears to be fair.

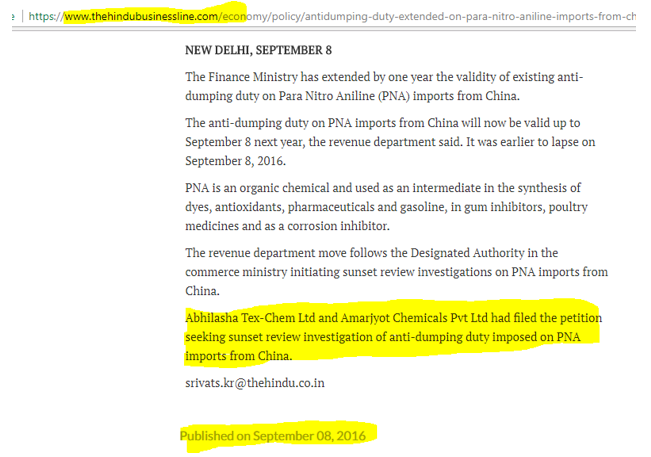

Product lines of Abhilasha and Amarjyot are similar as they together had filed for ADD for one of their products & the ADD is levied for 5 years more starting from mid 2017

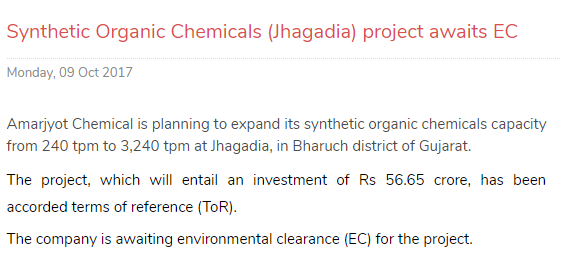

Google search shows a debt of ~117 cr on Amarjyot Chemical -