There are only two raw material here, Phenol and chlorine -> they mix them to make different types of chloro phenols.

They import phenols from international markets and chlorine is for free , I tried to see the phenol price variation but i couldn’t find historical data anywehre.

Rupee depreciation might have helped as well but they have claimed they are currency neutral as they import phenol and export cl-phenols so there is a natural hedge.

I think its a very valid question from the perspective of how long these margins going to be sustainable. I don’t have the answer for that.

May be people who are holding it from long time could answer that ?

Could not resist any longer. Entered at Rs740. Seems to be a good company and have started paying dividends already. Hope there is still value at Rs740!

Why is reliance buying this company? That too 2% for aroundRs5crs which is peanuts for them. Doesn’t make sense.

I always remind myself with life lesson from Buffett …

This feeling of could not resist is the worst of all kind of feeling in stock market, I came across this blog on expected returns, Now after the run up your expectation should be around 15% CAGR.

After all its just a Chemical company , right now enjoying pricing power its a matter of time somebody would start making Chloro-Phenols . Considering that i exited the stocks today.

Also technically this seems like a top to me …

It is quoting at an annualized PE of 25. Quadruplling of sales, high ROE, ROCE and the small cap size attracted me. On top of it, this is dividend paying and has no debt. I am not happy about the price I bought for sure, considering I have been tracking this since around Rs400 levels. but i feel it is still not crazy valuations to consider exiting. Debt and cash are a majority of my portfolio now. My exposure here is very limited protecting downside risk. This is more like a small indulgence in an otherwise disciplined risk management. True, I cannot afford multiple such indulgences.

The CAPEX plan is 5 years down the road , If that would have been happening next year then its cheap.

If you put the numbers in the Excel sheet as per calculations shown in that blog… i think even at today’s price you can make 15% CAGR for 5 years considering pricing power remain intact and market sentiments remain firm etc.

I think personally 15% is fine considering the alternate investment options available at this time with heavily over valued stock market. I am as such struggling to find value in this market. Please advise if you have any picks with a good margin of safety.

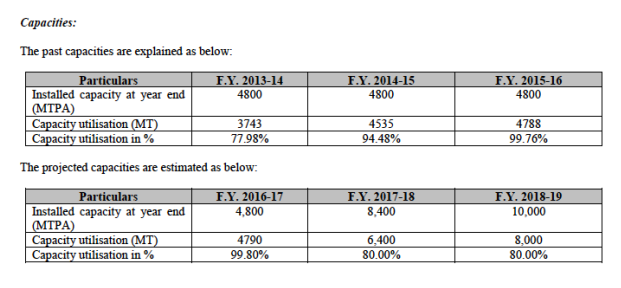

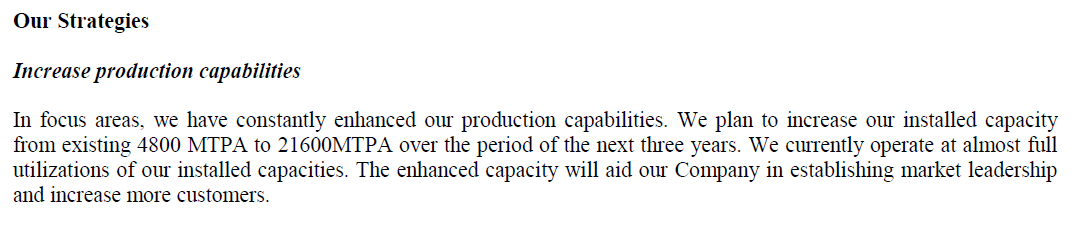

Well, from what I know the capacity expansion isn’t something that takes very long. It can be done very quickly once the clearance is there. While I don’t have exact numbers, the company can double capacity in a few months if required. However, capacity here is more a function of not flooding the market rather than the time consumed in expansion itself. I don’t think the company wants to suddenly double capacity, in which case the entire market now knows you have a lot of supply but demand is the same. In such a situation, to avoid idle capacity, a company would be required to slash prices.

Here, I think investors should think of the capex as capacity “in-the-wings” waiting to be brought online quickly when additional customers are added. Just my two cents. My source remains the DRHP statement and conversations with the company from time to time:

Thanks very well explained the economics of the business.

I tried to reach out to the management over the email investor@valiantorganics.com but i never got any response, May i know how you are in touch with management ? does the simple phone call works ?

I would be great if you can ask these questions raised the community members .

what is contribution of our top 5 customers ?

When is the government approval expected to be received for the expanded capacity ? (tentative time if any - 3 months / 6 months ??)

If the product price is set by China, then are the margins sustainable ? (mgmt informed China’s production cost is increasing in AR).

What is our competitive advantage over China ?

What the strategy from the merger of Abhilasha tex chem ?

Are there any Capex planned here as well ?

It typically takes a long time to get response from management - involves a lot of follow ups.

What is contribution of our top 5 customers?

Haven’t asked yet.

When is the government approval expected to be received for the expanded capacity ? (tentative time if any - 3 months / 6 months ??)

Trial production is on and will continue in second half of financial year. No date for final clearance.

If the product price is set by China, then are the margins sustainable ? (mgmt informed China’s production cost is increasing in AR).

Price is not set by China, as per company, it is set by themselves. Not sure how far it is true.

What is our competitive advantage over China?

Cheaper costs, better quality. Personally, I think the Aarti brand and distribution advantage is the biggest competitive advantage as you are getting relationships of an established big business.

What the strategy from the merger of Abhilasha tex chem ?

No specifics, just synergies mentioned.

Are there any Capex planned here as well?

No, ample capacities there. Plus paranitroaniline has antidumping duty for another 5 years.

Have they extended it again ?

The anti-dumping duty on PNA imports from China will now be valid up to September 8 next year, the revenue department said. It was earlier to lapse on September 8, 2016.

I guess it might have expired on Sep 8 2017.

Also, Another thing is what after all the CAPEX is done 21000 MT , Then there will not be any growth.

If you see the PAT would be around ( if pricing power remain intact) 46 Cr and MCAP would be around 550 Cr.

Which is like 40-50% up from todays MCAP and if they take 5 years to achieve that then its not trading at very attractive valuation today.

No competitors comes in - pricing power remain intact.

No problem in getting regulatory approvals for further CAPEX.

We won’t worry about the pollution like china and won’t shut down the chemical plants.

Management won’t do anything stupid.

Even after that all capex done and if its running at full capacity utilization making 50 Cr then it won’t be a growth story anymore.

So , i feel markets will not pay 25 x for the stock. Markets may pay 10-15 x.

which is like 500 Cr - 750 Cr MCAP this is like 2-3x of MCAP today.

I think you are seeing the facts right now and concluding that nothing further will happen in 5 years. If you like nicely spun stories of how a particular company will grow for the next 30 years without any slowdown or set-backs, maybe you should re-evaluate how you assess investments.