I was watching CNBC in morning. They said it can go in two digits also , they gave 50-60 targets.

But is it really possible (Unless its a big scam like Satyam). Management has clarified that nothing is their still stock having continuous lower circuits daily.

Depends on Mr. Market. If market wants to punish this management it can bring down multiple to 10. Having EPS around 7, price in double-digit is possible.

hmm…Than will wait for such an opportunity…I bought 3-4 yrs back around 40 rs , than sold around 80 without any reason…waiting for correction since than and it touched 500. If it comes in two digit , will give it a benefit of doubt.

Disc : Not invested

Since Vakrangee began transforming itself in 2013 (according to their own presentation) going asset light model using the franchise route, company has effectively transferred asset heavy part of their balance sheet to the balance sheet of franchisers in exchange for higher operating costs. This converts their capex into opex.

As a result EBITDA margins have dropped from 28% to 20% but Net margins have gone up from 9% to 13%. This is because rising operating costs was more than offset by dropping depreciation and interest costs over last 4 years (which is almost zero now). During this period, D/E ratio has dropped, interest cover has gone up sharply, operating cashflow has gone up to. Essentially they did all the steps necessary to get their stock re-rated by the market which was previously weighted down by their asset (funded by debt) heavy balance sheet.

But I doubt if the underlying business model actually transformed. that’s what I actually wanted to find out in their annual reports but all I got was grand vision of transforming India at the grass root level.

9 Likes

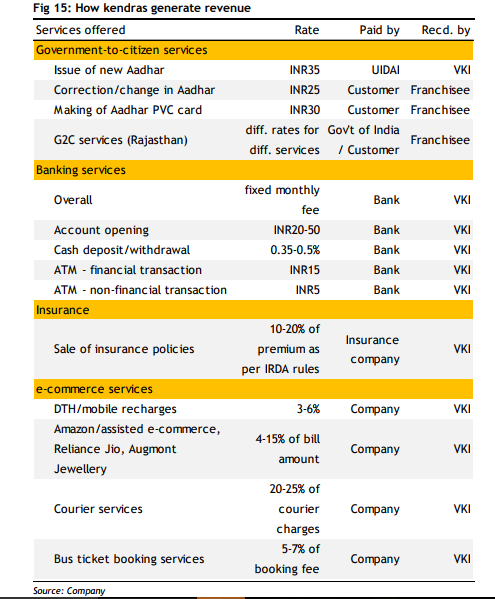

I just got a report prepared by Maybank, available in Vakrangee website. Got some info related to VKI revenue details, Hope would be helpful for some analysis

Apparently they have done over 50 million Aadhar enrolments. That’s about Rs.175 Crores. Assuming each of them has a correction, its another Rs.125 Crores. Assuming each of those 50 million enrolments also got a PVC card, its another Rs.150 Crores. So overall its about Rs.450 Crore revenue from complete Aadhar enrolment business - Am being extremely generous with the assumptions here.

Their last 5 year sales is over 18000 Crores! How is it even possible? Is Aadhar not even 2.5% of their overall revenue?

2 Likes

Vakrangee - Initiation Coverage report by Maybank.pdf (1.3 MB)

Attaching the complete Maybank report, thought it might be useful

http://www.bseindia.com/xml-data/corpfiling/AttachLive/4cbc03c2-e011-4ae7-a751-06a7f9beb4b5.pdf

Clarification letter dated feb 03

So basically it’s just falling for no reason. Business of the company remains unaffected. Growth Target’s remain the same.

A correction was due in the stock and I think its and opportunity to add to ones position.

Though I would wait for the stock to settle before I add some more.

Cheers

Aj

These two simply don’t correlate.

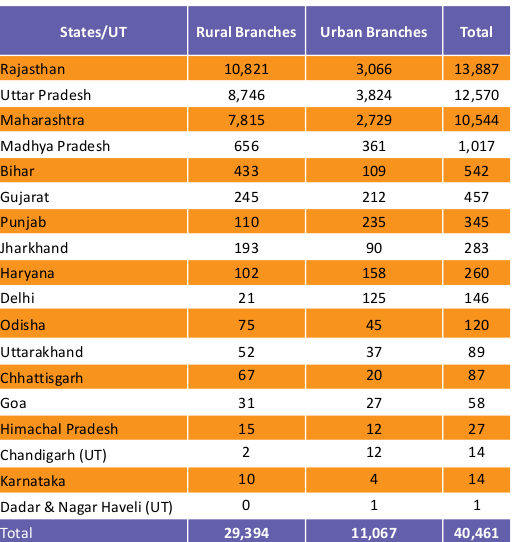

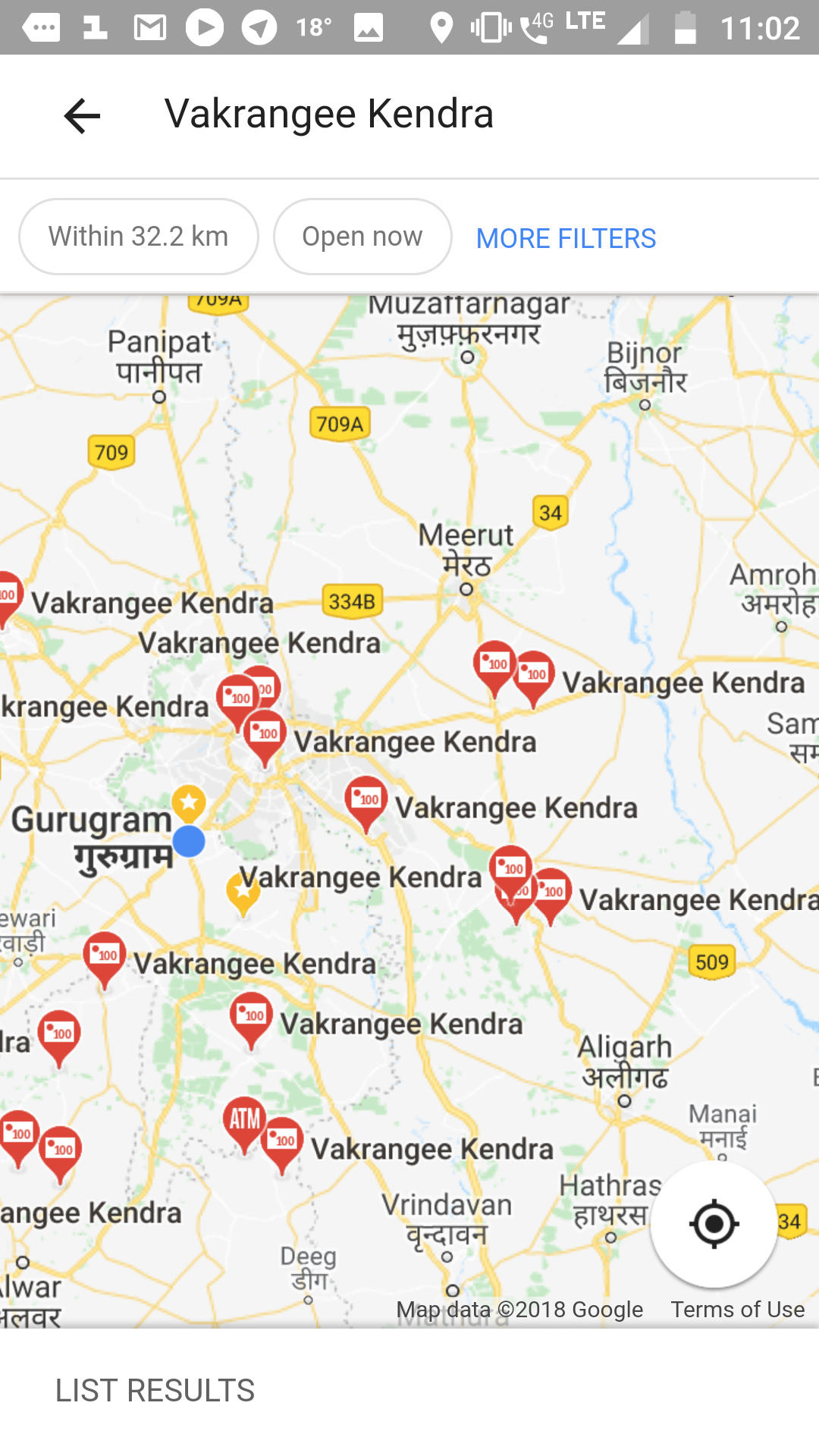

and Kendras on the map add up to only 20.

Granted this is not the most scientific way to check but only 20/40461 are locatable on the map? If you argue that rural ones may not be on the map, I would expect the urban ones to be on the map - At least 50% of the 11,067 kendras have to be on the map? 20 is nowhere near.

Urban centres of such utility businesses always get mapped. Take a look at Bangalore one centers in just my 4 km radius for example.

Yet another way to look at this is via SBI ATMs - Which according to their website is 43,000+ in the country. Vakrangee Kendras are supposed to be 40,461 so its a comparable number. Search on the map by location for SBI ATMs and you will see hundreds on the map in each city correlating to the 43000 claimed number. Not so with Vakrangee Kendras. Something seems off with the claimed number

7 Likes

Here is a list presented by the company wrt Amazon related services.

https://vkms.vakrangee.in/VakrangeeKendraLocations/Amazon.jsp

1 Like

Interesting. When I do a search here in Gurgaon, it shows me some 17 Vakrangee Kendras around here alone.

2 Likes

Budget 2018 and Govt focus is rural / farmers improvement and connecting them with main stream of development.

Many businesses like Insurance, Banking, Logistics, E-commerce, etc are now seeing the best opportunities of growth from rural and semi urban. These businesses do not want to be capex heavy by opening their own centers and do not want to increase their cost of services by having their own man powers. However, they look for Business Correspondence through them they can deliver their services with minimum cost. Vakrangee over a period of services/experience in rural and semi urban area knows ground reality. Vakrangee having technical platform and necessary govt approval like IRDA for Insurances services, RBI for Banking business correspondence, etc act as moat for new player…

Having huge networks of VKs, they can bargain good commission from business who want to roll out their services to rural and semi urban through VKs. It is win-win situation for VKs and Businesses as VKs can get good commission and Business like insurance, BFSI, Logistics can get business at reasonable cost compare to their own branches. For established VKs, adding one more services does not cost much more as they can use same IT and manpower with technical integration through Vakrangee. Hence, this will be huge operating leverage VK can get.

http://www.vakrangee.in/insurance.php

http://www.vakrangee.in/banking-services.php

The only critical point is promoters should not spoil reputation for short term gain. With latest clarification, appointment of excellent CEO (Ex HDFC guy) and having huge opportunities, if they focus on solid and honest ground they and investors will be benefited hugely

Main strength of this business: 45000 (75000 by 2020) Vakrangee Kendra integrated on same Vakrangee IT platform. For example… If HDFC Ergo want to roll out their insurance services to 75000 centres they can do with help of Vakrangee through VKs. With this HDFC ergo can get huge untapped rural market without much cost and Vakrangee can bargain good commission from HDFC ergo.

2 Likes

Here, you can find sample revenue break-up model claimed by Vakrangee for Rural and Urban VK.

@phreakv6 @Yogesh_s

One should count following in revenue -

Vakrangee charging 2.5 - 3.5 Lakh as non-refundable deposit for granting any franchise. Present growth of revenue covers (1) study income from comission due to sales of product from VKs (2) income from one time non-refundable deposit. What i believe the exponential growth in revenue is due exponential growth in new VKs. More number of new VKs generate more revenue as non-refundable deposit. (3) study income from insurance product commission - Vakrangee acts as corporate agent for insurance company. Hence, once they sell any insurance policy, Vakrangee get commission on premium paid by policy holder (annuity type income)

Key take away Exponential current revenue growth is due income from one time non-refundable deposit per new VK. More number of new VKs more revenue that Vakrangee claiming. Over a time, as VK getting mature real income will be from commission from matured VKs due to sell of services

If you compare Vakrangee and PCJ shares traded on 1 & 2nd Feb

Vakrangee - % delivery based volume - On 1st Feb 63% (~ 66 lakh shares) and on 2nd Feb -100% (35 000)

PCJ - % delivery based volume - On 1st Feb 26% (18 lakh) and on 2nd Feb - 5.6% (8 lakh)

hence, more trading activity in PCJ whereas more delivery based activity in Vakrangee

What this concludes ??? Please share your view.

Are Promoters of Vakrangee buying from open market at this corrected price ??

1 Like

Disclaimer - I do not own shares in Vakrangee, will never own. I am hence a neutral objective observer here

The one thing I have learnt from the market over the years is this - when a stock keeps falling and you cannot figure out why, most of the time the market knows something that you do not. Please assume that you are the sucker here.

One has seen this in some counters in recent times - Shilpi Cables, Treehouse. The stock price falls first, then the bad news comes out since promoters/management will keep BSing till they just cannot anymore.

This counter being valued at 50,000 Cr itself was an anomaly in my opinion.

I had heard about this investment idea from someone 3-4 years ago, I decided not to consider it since I have spent time in IT sales and have run interacted with the company’s salesman in the past, let me just say it did not meet the criteria I have when I do channel checks

Be very very careful in stories that unravel in this manner, looking at fundamentals and numbers in such a scenario isn’t usually the best approach.

16 Likes

Nice post @vij

The list shows 10,031 addresses.

Do we have any reason to doubt such a elaborate list?

I hope many of us have seen the MumbaiMirror post with which Vakrangee price had a nose dive:

https://mumbaimirror.indiatimes.com/mumbai/other/aadhaar-enrolment-firm-under-sebis-scanner/articleshow/62677483.cms

What I analyze from the news:

Good part:

- The SEBI concluded “no adverse inference is drawn" and recommended that the investigation “may not pursue this matter any further”.

- The suspected trading happened long back: January 1, 2016, to June 30, 2016, and September 1, 2016, to June 15, 2017.

- Vakrangee has not yet received any official notice from SEBI/NSE/BSE.

- The bad news is about suspected unfair trading practices, but nothing related to bad fundamentals to the company. If bad news is proven as true, then related people shall be punished. But, that may not radically change Business model of the company.

- One of the directors, Ramesh M. Joshi, if a former executive director of SEBI.

- It is still at the rumor level. How did MumbaiMirror get the documents? Have they published those documents? What all is written in those documents? It seems to be half-hearted truth.

- Allegation of published names Dinesh Nandwana (the current MD & CEO of Vakrangee), Ashok Kumar Gautam (former director) and another client Vinod Kumar Bohra, are already defended by Vakrangee in the formal letter:

http://www.bseindia.com/xml-data/corpfiling/AttachLive/4cbc03c2-e011-4ae7-a751-06a7f9beb4b5.pdf

Bad part:

- The news is about a group of 22 clients related to each other as well as to the company were continuously buying and selling the scrip, accounting for 74.87 per cent of market gross on certain days. They traded the scrip on 123 days, and 18 of the 22 had more than 90 per cent trading activity in this scrip only.

1 Like