One point though treehouse had taken in a lot of cash by diluting equity and also had a tad bit of debt.Compared to vakrangee it paid only a small amount of tax in comparision to the equity it raised…Also it’s dividends were small too.

1 Like

I think it’s of limited use to just focus on past ways of frauds and look for those indicators. fraudsters are very smart people they innovate new ways that you will not find suspicious, instead when fraud will be out you will say oh! It was a one off fraud but there was nothing wrong in my analysis. I will now take care of this new indicator further.

This doesnot work. You need to think like a Promoter, what all you will do to fool the investors .what are you best at.

I think most important thing that value investors missed was competitor comparison. Most mentioned that Vakrangee has no competition … and just kept making big profits without any USP or a patent. Actually companies like FINO were direct competitor in financial inclusion and hundreds in Aadhaar . If any analyst do even basic comparison of these company financials from MCA with vakrangee they will have absolutely no explaination for vakrangee revenues and profits.

2 Likes

Hi

I dont follow this company but have been tracking their business for a few years since I used to work in a similar space. Today’s Ken Article is again about Vakrangee. More here: Vakrangee: It is all relative - The Ken

Its a lot muddier than I thought ![]()

Rgds

Deepak

4 Likes

Had pointed out these entities from the shareholding here but had no idea these were present and past directors’ companies

8 Likes

All of them most likely exited at lower than CMP (81 / 160 before split) it seems. Before the run-up of last year started. Doesn’t add up.

Vakrangee Limited-$ -Clarifies on News item

Great piece of investigative work done there.

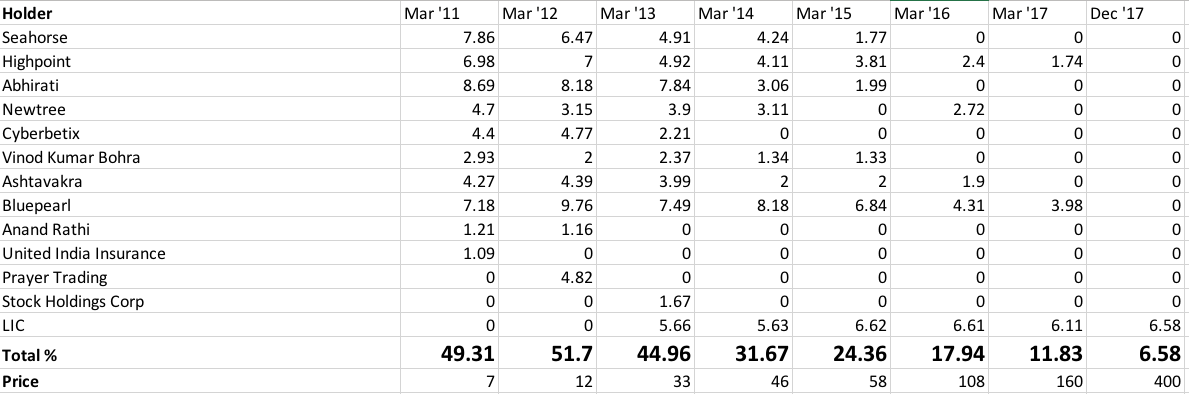

Let me try to complete the story then.First in 2012 -2013, these related parties dispose of almost 12 percent of their holding (excluding LIC),they would have made atleast 200 crore(using the average value of the share price in that time frame).Then in 2013-2014,they dispose of 13 percent more to make atleast 400 crore,they repeat the same in 2014-2015 to sell almost 7 percent shares,to make almost 400 crore,they repeat the same in 2015 -2016 to make atleast 500 crore more,then in 2016 -2017 ,one more sell off and the company makes almost 700 crore.It finally repeats the same thing in march 2017 to dec 2017 to sell amost 5.6 percent shares to make atleast 2000 crore.

Total corpus collected :4200 crores.

This does not include the sell off in promoter shareholding in the time period 2011 to 2017,which i assume must be worth quite good too.

It is now a piece of cake to pay 1000 crores as taxes and also a small amount of dividend.Nice little ponzi scheme they have got!!!

Disclosure:Dont hold this stock,only following this stock for personal curiosity.Opinions may be biased.

1 Like

@Gothamcapital So, same modulus operandi, back-end proxy promoters shareholders working in full swing  Great work @phreakv6 . Good there are more quality research being done by likes of Ken, Moneylife

Great work @phreakv6 . Good there are more quality research being done by likes of Ken, Moneylife

Need to beware of monkey business,i guess.

Funny how the annual report 2016 claims bluepearl as a shareholder other than promoter,even though one of the directors is a director in vagrangee infra.

All this happened in plain sight.

Why do you think sebi gave clean chit to this company??

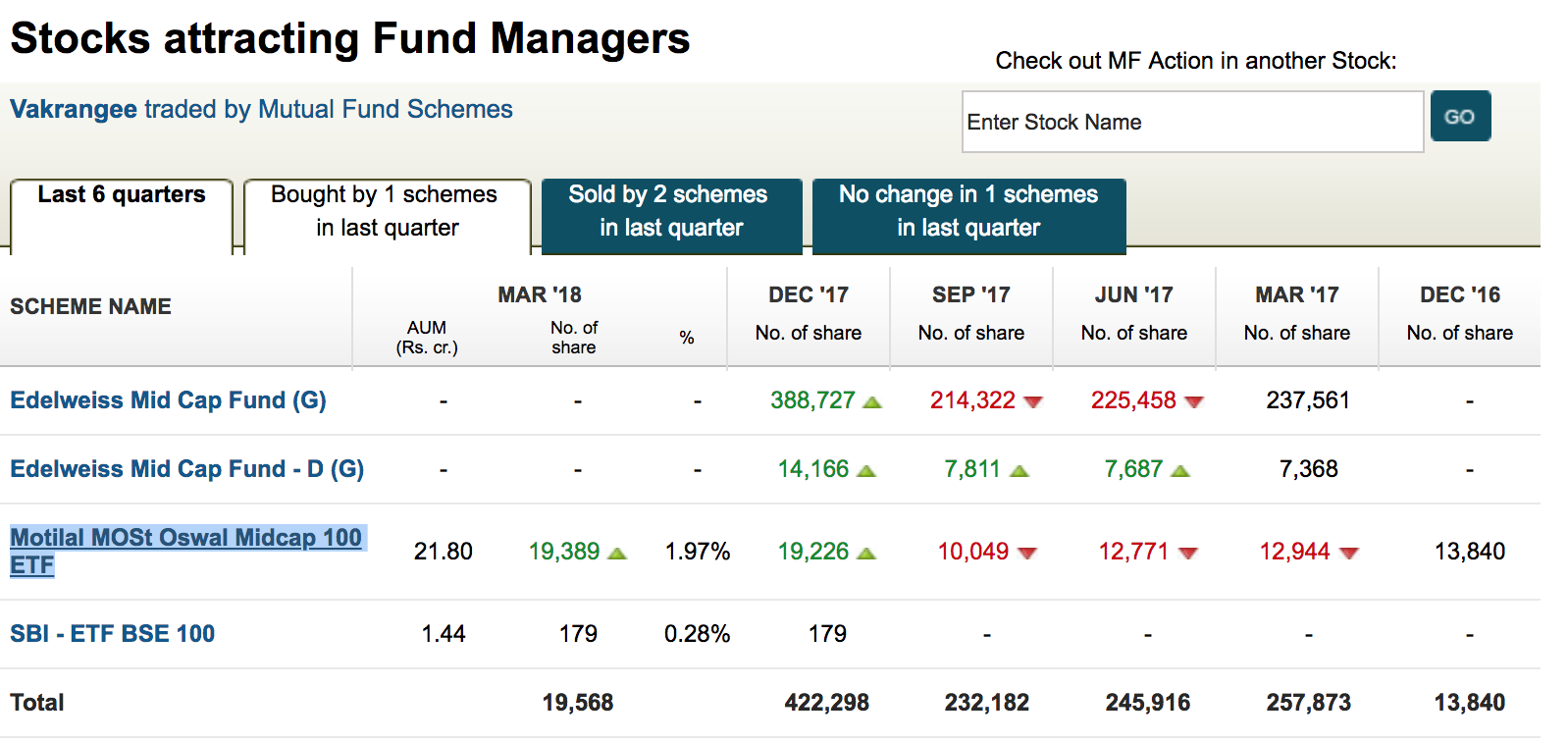

This thread is informative to a rookie like me who wants to spot wealth destroyers. I see Edelweiss Fund selling close to 400,000 shares in one quarter, while the existing Motilal adding just 163 shares. Can I take such huge selling from a mutual fund, as one of the red flags, while analyzing another such stocks

1 Like

Motilal has bought it only because they have to index the ETF to Midcap 100.

1 Like

It’s high time the real issues should have all come out openly and management should have accepted them and declared exact ground situation.

The stock has already fallen so much that it doesn’t justify the reason why management will remain in denial mode.

I think at this stage, they can easily present a verified and active list of franchise categorized with average quarterly sales listed with direct contact numbers, gps locations, photograph of the place and person instead of useless, unreachable list they show on website. Even if the list reduce to 1/3rd it will justify buying in stock.

PWC resignation is said to be based on bullion & election book records.

Bullion, it seems they were selling gold coins via their franchise … this can be other reason for high sales turnover though not for the high margins. They might have shown to auditor bullion sales as major source of revenue but might not been able to justify the profits shown on it. Any business can jack their revenue with bullion sales.

But not sure what does auditor do with election books ? and how its a major concern for auditor… could be for company secretary but why for auditor ?

Dear @peeksden,

In a previous post you had hypothesised the company’s modus operandi of laundering money. Per that theory, they receive unaccounted money, recognise it as revenue and cleanse it. Is it plausible that the profits are indeed genuine?

Because if the company is a money laundering scheme, it must be retaining some portion as commission. So, investors may not be invested in an egovernance company but a money cleansing organisation. In any case, if the profits are real the company is worth something. What exactly? Only time will tell.

The apathetic silence by government agencies raises more questions than answers.

By your logic, even if the profit are real, it was one off due to demon, while stock market is all about sustainability of earnings. So to answer your question, if the profit is commission from money laundering, it is worth nothing now as this money is not sustainable (not even considering the legal implications!)

I think revenues from primary mentioned sources like Aadhaar, Banking correspondent business are not more then 10% of total revenues in last 5 yrs 2012-17. some other business like insurance, ecommerce , atms are very recent ones and yet to be considerable revenue source in annual results.

Money laundering justify many question like high tax, dividend payments but no data to say that with confidence. When more data about issues come out like from auditor, management, employees, investigations agencies we will be able to conclude Modus operandi.

When a company promoter is a CA , it’s expected that regular checks by agencies, auditors, investors will not work. Statutory Auditor is the first person expected to wake up after such allegations and will have immediate access to data for more detailed analysis.

By resigning and not making a deal, the auditor has confirmed the issues of nature that can severely effect their reputation. We need to take hints out of some words coming out from them.

PWC: it got no reasonable assurance whether the financial statements were free from material misstatements, whether due to “fraud or error.” the auditor had sought information from the company on several matters pertaining to its election books, bullion and jewellery business.

What are the hints behind these words ? I think

-

it clearly shouting that financial statements have material misstatements. For investors it means books are cooked. I fail to understand how some in this forum still keep saying that profits could be real.

-

weather due to fraud or error… This clearly means fraud only waiting for evidence.

-

Bullion and jewellery business: it indicate preliminary work by Auditor showed this business as part of fraud modus operandi. Surprisingly this revenue source doensot find much mention in their presentations.

PCJ link gets confirmed here and it’s not just about investing in PCJ but much more.

Bullion business is commonly related to money laundering so it does provide more indicators.

Election books: i am confused on this, why would a auditor have need to mention this.

3 Likes

Dear @peeksden, Thanks for the explanation. My interpretation was probably fallacious. Hence, I’ll delete my post.

I have a feeling this company has the blessings of some one high in the government.How else would a former sebi chairman serve as a director and yet so many frauds are going on.

Thanks for a polite and yet hard-hitting post.

It is not Vakrangee that has anything to earn people’s expectation of high stock returns. It is the people themselves - their dreams of getting rich. They may be coming-up with excuses to imagine Vakrangee as a stock that will give them great returns. This is very common and should go away after they suffer some losses. Obviously, it is better if we learn to appreciate reality without incurring losses.

There is a long documented history of people killing each other for the statues (of females) that they had fallen in love with. A statue could not have given them any love and yet they died for it.

P.S. Interestingly, this does not imply that Vakrangee can not give great returns in future. Everything is possible. Afterall, even with the current business model, the company had reached a sky-high market capitalization.

1 Like