One off topic question.

How many of you are attending AGM on 28th July?

One off topic question.

How many of you are attending AGM on 28th July?

I am going Jaipur to attend AGM Mihir… if you are also going there then lets meet there

can u pls update the group after the AGM - would be much obliged. I think highly of sunil agarwal and am thinking of adding more.

@varadharajanr, Sure Buddy…If you have any specific question in your mind, which I have not already asked from their CS & which I got a very prompt answer (within 2 days FLAT) please let me know,I can ask the same in AGM.

Also, I asked for the Physical copy of the AR from the CS, that I got today (within 4-5 days from my request) thru Courier (not by the Indian Post, which might take at least a week time to get AR from jaipur to Pune). So I fine their CS Mr Brahma Prakash very cooperative & prompt in his response to even an individual investor in company.

Disclaimer: Invested but will take decision to add more after AGM & Q1 results.

They have started 30 day unconditional money back guarantee across all products since yesterday. Of late, I have spent a large time on live tv of liquidation channel and found that products under $10 are sold briskly while over $75 generate very slow response even if product looks a steal.

To me vaibhav global has to built their strengths around being a low cost retailer ( which is evident) together with stretch pay, money back and free shipping for greater customer traction.It shouldn’t be a drain on finances as their products are so competitively priced they can easily mark up against their costs.

Also, if we apply techno-fundamental approach here 400 must be the base which it should not vitiate. Under 400 there must be some hidden negatives which we are not putting attention to.

But as sjain_13 pointed Mr. sunil doesn’t receive salary and as Prof. Bakshi pointed out in January that he advanced a interest free loan when company was in dire straits instills a lot of confidence.

Requesting serious guys to continue scratching surface.

Ashish

Please ask even after being one of the few low discount etailer in whole america and so competitively priced products and such a large addressable market - what is hindering their sales growth.

They are increasing their capacity by 50% with sales stagnating. Do they envisage pick up in sales in near future?

Yes, I also got the reply from their CS that Mr Sunil Agrawal does not take salary from Company, this is positive or negative we need to decide, but on prima facia its looks good and as promoter has 68.60% holding in company (Including holding thru their Mauritius based company Sonymikes holdings) & around 12% held by Nalanda capital, I feel once remaining 10-15% stock changed hands from “Weak” to “Strong” (Read Long Term) hands then I feel we will see less volatility on this stock…

Regarding 30 days unconditional money back guarantee & Free shipping, I feel they should be able to pass that on to their customer with increase on price by say 1-2%, if they can not then I feel they will not able to carry the same level of FCF going forward, lets wait & watch ![]()

@jainaj, sure will Ask this, if he dont share this with us in his opening speech (I feel he himself would like to explain this in his chairman’s speech).

And please make good detailed notes and update here.

This is the only scrip in past five years where I have averaged at a lower price otherwise I always buy on a rising scale

I was going through the employee reviews for LC on glassdoor, and one of the complaints that stood out was poor software to take and process customer orders. I am usually skeptical of online reviews (as the sample size is always biased), but in this case the complaints about software corraborates with management statement of upgrading to new s/w and outsourcing the call centre operations. Their website is now powered by SAP Hybris and sounds promising to me. Anyone here who can provide some insights on SAP Hybris?

more on hybris:

hybris is a software company headquartered in Zug, Switzerland, that sells enterprise multichannel e-commerce and product content management (PCM) software.

its a SAP company…

One of the biggest risks that Vaibhav seems to have is not from competition but rather extinction/disruption. In US hours spent on TV is on decline since last 5 years. US Viewership

As of today almost 70% revenues come from TV.

I have read somewhere that the punishment given to kids in USA nowadays is to take away their phones/tablets and making them watch TV instead…

That is a very long term trend… But it is true that TV is being disrupted by online devices and Video on Demand…

Television is not getting extinct (as per LED TV sales trend), it is getting integrated with the internet.

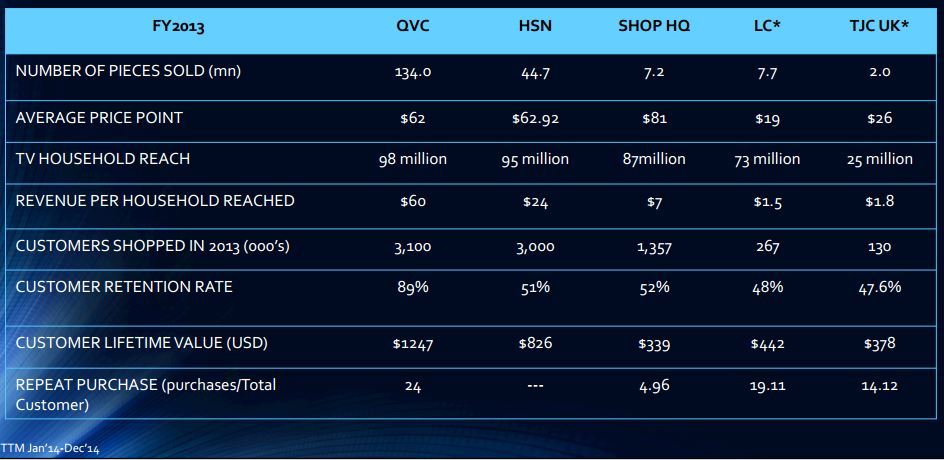

I am new to Value Investing and have started looking at Vaibhav Global. Has anyone studied the competitors HSN and QVC in detail ?Vaibhav Global ~ Vertically integrated value e-tailer of Jewellery and Lifestyle Products PFA snapshot from a presentation made by Mr. Sunil at MDI.

As per ppt VGL sells at average price of USD 20 whereas competitors sell at higher price points. However, competitors are not into just jewellery. They also sell apparels, etc. which will increase the average selling price.

I am keen to understand what is the average selling price of jewellery by competitors ? Is this figure specific to jewellery available for competitors ? If someone has studied this, please share your observations

Hello Ashish

Hope you attended the AGM. Desperately waiting for the details from you.

I attended Vaibhav Global’s AGM today at their corporate office at Jaipur & I am writing AGM updates from Jaipur Airport itself

** AGM Updates:**

1.Promoter (Sunil Agrawal) is very-very down to earth person & he freely interacted with most of individual inventors on one & one basis and answered almost all the question which we may have.

2. Mr Sunil told that Toal Addressable market for their business in US alone is 20 B USD & they have able to reach just 1% (200 M USD) as of now & given a hint that what will be the bottomline once they are able to achieve even 5% of the total Market in US (~1 B USD).

3.They have invested in IT last few quarters & setting up a new facility in SEZ (around 1 kms away from the existing facility & new facility will have almost 140% capacity & most of the work will move to new & better facility. All the Capex for that is already done, so they are not expecting any more capex in near future.

4.Promoter feel with new Hybris based web platform they will be able to serve their web based customer better with data analytics capability available in new web platform, so they can do some analysis on customer behaviour who are visiting their web site & they feel that going forward more sell will move to web based catalogues based buying & that will improve margins.

5.Mr Sunil informed that unlike India, US ppls dont prefer to use Mobile APP, instead they want Mobile & tablet compatible web site, so that they can view & order thru Mobile/Tablets on the go/any place.

6. Promoter wants to keep the EBDITA at least in double figure, So thy are fine with 15-20% revenue growth, but they dont want to grow by 50% plus with low EBDTIA Margin and he mentioned that QVS has 40% gross margin and 21% EBDTIA and they have 61% gross margin but 11% EBDTIA… So they feel that once they increase sell even by 15-20% but EBDTIA margin will improve more than that due to Operating leverage.

7. Promoter were very optimistic for their business post Q2 this year, as they have already given guidance for softer Q1 & Q2 and robust results Q2 onwards.

Promoter arranged a factory visit for 7-8 shareholders (including me) without prior appointment & Mr Unnat Gautam (Who guided us in the factory visit) was very-very open to discuss/disclose anything which we asked and after visiting their factory I am convinced that gem stone Jewellery making process is very specialised job (need very Skilled labour) & can not be replicated in any part of World including India very easily with same level of economics. They treat they Workers very well (both permanent & contract workers) & pay higher side of salary to retain them with Vaibhav Global.

All in All I an say it can be good 25-30 CAGR grower & if they are able to shift more & more customers from TV to Web then we can see even better margins…

Anybody has any other questions then let me know, if I know that already then I will try to answer those…

** One more thing that they also started Stretch pay in US market to counter competition poised by JTV in US & they said that they will increase price by 1-2% to recover any addition cost incurred by them for Stretch pay and as these payment will be done by Credit Cards for 3-4 instalments, so these are relatively safe transitions & very less (1-2%) risk of default on EMI/Stretch payment…

Thanks Ashish. Much appreciated. Is this 20 bn opportunity only for jewellery or includes other fashon accessories , apparels, etc. As posted yesterday, QVC and HSN also sell apparel etc. which tends to push their avg ticket size and market size to higher value. Please advice

I feel this 20 B opportunity for total market Size which Vaibhav Gloabal, QVC, HSN etc address ( I feel its including accessories as well)…I feel he mean to say if you add up revenues of its competitors & Vaibhav global it should add up to 20 B or so…So, with Jewellery & Accessories they are looking for to capture around 3-4% market share, but it can take sometime as they are not expecting to growing more than 20% at the cost of EBDTIA margin…so it may take maybe 5-10 years or more than that…

Results for FY16-Q1 declared : http://corporates.bseindia.com/xml-data/corpfiling/AttachLive/63ECDAEF_6451_45DE_B1A7_0D764F8114C5_191420.pdf

not so good results & be ready for hammering in stock price tomorrow, if this kind of results is not already priced in

{kind=link}