This is my first Post on ValuePickr (Though I am following it on & off ), I went thru the most of the post in this discussion of Vaibhav Global & I see Ppls here has Missed feeling about Vaibhav Global.

I have entered into Vaibhav Global recently around 550 levels with Small quantity & following it up to get more confidence on Management (Read Promoter), so that I can put large sum into it.

So, Far I have not see anything wrong with Promoter, he looks very Down to earth Person, understand his Business very-very well (This he has shown in his con-calls & now in AR as well),Reducing Debt of the company (Very Positive things), Declared dividend recently (another positive thing) & I have gone to LInkedin to see their employee profile & saw that they have recruited a big numbers of sales & Marketing ppls from various new IIMS (Rohatak, Udiapur etc), this shows that they wants to have BEST talent available in India in his country (Off course he is not Amazon & Flipkart’s of world that he can recruit from IIM A B C L & increase cost of his operation).

I had read their recent AR & after reading that AR I had few queries, which I thought let me clarify from CS directly instead of asking ppls on various forums & get half-backed info. I got very-very Prompt response from their CS Mr Brahma Praksah (within 2 hours of sending my email he acknowledged the receive of the email & within a day I got response for all my queries), so here are few of them (I can not put all here due to obvious reason):

1.Need more info regarding company’s GDRs Listed on Luxembourg Stock Exchange, are these GDRs are actively traded on Luxembourg Stock Exchange?

CS: There is one GDR holder as on date, holding 3,95,000 GDRs convertible into 39,50,000 Equity Shares of Rs 10 each. These GDRs are listed at Luxembourg Stock Exchange for trading purpose. .

*

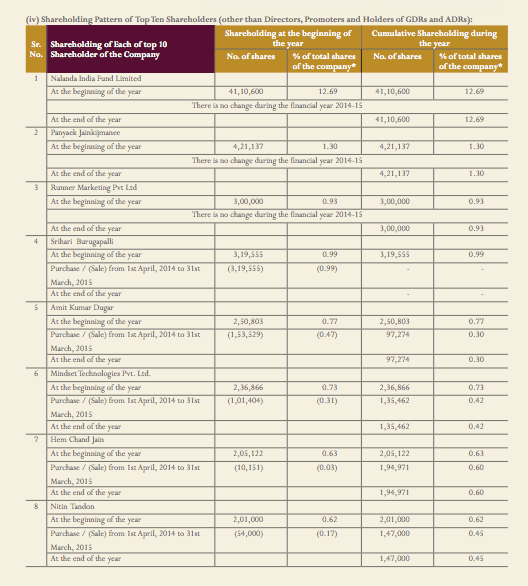

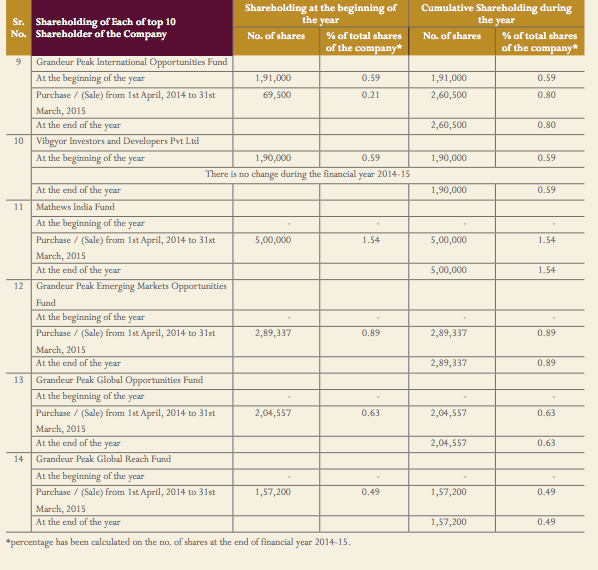

2.There is around 59% Stocks are publicly held (12.44% by Nalanda & remaining with Public) and remaining 41% with promoters including "Sony Mikes Holdings Ltd”, so what is the reason with LOW promoter holding in company?

CS : Promoter/Promoter Group holding including GDRs is 68.60 % and the balance belongs to public.

3.As on 31 March, 2015, the Company’s (VGL Group) employee base was 3,210 could you please provide a break-up of the employees based in india, US & Uk offices .

CS: In UK, over 95 and in USA over 550 people in sales & marketing, customer service, logistics, TV production, e-commerce and support functions.

4.Could you please provide Remuneration of MD/Chairman Sunil Agrawal, as I am not able to find the same in the AR & it is good idea to put Remuneration of all top management persons in the AR for reference & change year on year.

CS: He is not getting any remuneration from the Company.

5.Why we have Variable Tax Rate?? Why it was almost 10 time tax on the PBT in FY2015, than FY 2014, which has affected the EPS for FY2015 significantly.

CS: The Company had brought forward losses till 13-14 and therefore, tax was minimal. In FY 15, the losses were absorbed and resulted in tax of 24.5 cr on a PBT of 127.6 cr i.e 10% PBT.

So, with Above discussion couple of positives I see: 1. Mr Sunil Agrwal not taking any Salary from VGL, I feel its good sign of ethical & honest promoter. 2. Promoter holding in company is actually 68.60% (GDR holding company Sonymikes is the promoter group company registered in Mauritius & they are converting GDRs to VGL shares (1:1), so including that promoter hold 68.60% around 12.69% is hold by NALANDA INDIA FUND LIMITED (which is LT investor in this company), so it makes almost 80% stock are closely held & Just 20% is available in market for trade, so this is the precise reason I see a sudden fall in VGL stock price like we saw in Hawkins Cooker’s stock price as well from 4700 to around 2300 in matter of couple of months. So this problem always there with low float companies…

So, All in all I like this company, specially its promoter & planning to visit them on their AGM day on 28th July.

My other 2 major holdings are Eicher Motors & Page Industry…

But as they have paid all Long term debt, so I feel this should not matter much, if they are not planning to raise debt in near future.

But as they have paid all Long term debt, so I feel this should not matter much, if they are not planning to raise debt in near future.