So the question is how far is tomorrow, right? As pointed out earlier by Jatin, the bet is on 25-30% cagr over the next few years. As for most investments, you ride it till the story is working.

I am hoping to see something brilliant from the management.

Faced with a cash crunch, I want to see how they tackle it - hoping that they do something unconventional.

Example: Should they open only 5K sft stores from now on? The capex requirement will be much lesser. Op. expenses for these stores will be lesser. Inventory will be lesser. Useless if sales also go down by the same proportion… But can they achieve the same amount of sale in a 5K sft store as they can in a 8K sft store? What is sacrosanct about 8K figure? Afterall they are the only organized retailer in town. Their asset turnovers will jump up much higher this way…

Example: Will they launch a new category, that leads to higher margins… Or attach a small cafe/food outlet in their stores. And increase margins?

Even these examples are really incremental types - not the strategic types that can create a 10 year Walmart story. Yet, it is more comforting than the story where they continue the status quo by raising debt.

Real strategic story will be doing cost optimization in the back-end (if you have to be the lower-price retailer in town, and still make good margins, then you ought to have a great backend…) … I havent seen any Indian retailer do that - neither Trent, Future Retail, Spencers, … So, not too optimistic about that…

Even if tomorrow is much later - it is not too comforting… Because today’s picture is not so rosy…

But you are right - you can ride the story for short/medium-term… and then take it as it goes…

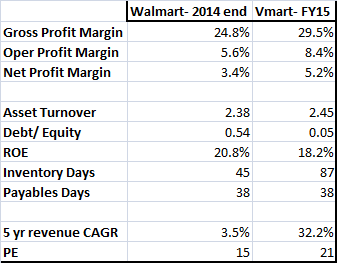

HG,

Would be interesting to compare Wal-mart 30 years ago with Vmart of today. Will try to do that later.

For now, just glance at present numbers of Wal-mart-

( Have taken Wal-mart’s numbers from Morningstar website & Vmart from screener/ company ppt/ own calculation)

Only place where Vmart seems to be lagging is Inventory turn. If they can improve that, then it would be super.

3 Likes

Doesn’t this comparison with Walmart tell you the problem?

In US, the cost of debt is 3% types. Cost of equity is probably 7%-8%…

In India, the cost of debt is 13% types. Cost of equity is probably 18% - 20%

If a business generates 20% return in US and takes on debt at 3% cost - there is no risk in that…

If a business generates 18% return in India and takes on debt at 13% cost - it is not an equally comfortable story… Especially if that 18% return is not quite predictable and certain… If it falls to 10% in a few years, then it starts getting quite scary…

Current 18% return is without debt- With some debt, ROE will go 20+%

If it will fall to 10% in few years, then stock will fall a lot… maybe 50%

Yes, so if management can maintain 18% or higher ROCE it is fine, even if they raise debt… After a while, the internal generation of cash will improve and hopefully they wont need any further debt…

Problem is if the business has a couple of bad years - then ROCE will fall, and stock will take a beating… And business may start going down a negative spiral…

The mental struggle is taking a bet on whether the business will have good years for the next 3-4 years without interruption…

1 Like

To understand the gravity, one has to do a sensitivity analysis…

How much of fall in gross margin will cause ROCE to fall below 13%…

A very quick estimate is that even a 2% fall in gross margin will lead to ROCE falling below 13%… That is really a close-shave margin…

2 Likes

@PP1, you raise a very pertinent risk regarding profit and ROCE if growth tapers down…

Retail is a generally a low barrier to entry business, with low margins. Retail bellweathers Walmart and Walgreen make 3% profit on every dollar of sales, so store management is critical. The problem is that many retailers dont execute flawlessly as these two and burn out as soon as trouble hits. Also the sector is rampant with competition with new concepts and stores being launched everyday. So the way to build a great retail business is to be the low cost leader.

If you look at the data for Vmart – there is enough evidence of management doing the right things, pulling the right strings to steer the business in the right direction. The debt free status, margins ~9-10% for 10 years (except FY09), major improvements in inventory and asset turnover when other players are struggling to breakeven, leveraging further and eventually going down. What really stands out to me about this management is the focus on cautious growth – align backend before rapid expansion of store network and follow a 30%:30%:30% growth principle to increase Sales, EBITDA and pat by 30% every year.

These are interesting patterns. Maybe they can create a brand and with the low cost advantage may become difficult to dislodge? Question is whether they can sustain this growth without too much leverage or dilution and will they manage to sustain margins?

V-Mart occupies a profitable niche in a highly competitive retail market – it is a low cost leader in locations where large store retail formats economics do not work

-

Growth - They can continue to grow for many years – there are total of 600 districts in India

(each of which can on average take 2 stores) – so total of 1200 locations to choose from…so enough room for growth - Competition – organised retail (Shoppers, Pantaloon etc) already exists in 50 districts where they are present in…continue to grow rapidly there as the value proposition of “fashion, quality at a reasonable price” appeals to the target segment + they have low overheads compared to larger stores

- Low cost leader – Please read my post above (V-Mart Retail Ltd - #65 by Naman)

- Favourable Economics – Vmart has demonstrated that people in smaller cities have buying power, where they have been able to sell more than 8000 Rs per square feet, which is comparable to what Shoppers Stop, Future lifestyle do in larger cities; Rent is much lower at <5% of sales, so allows them to make above industry margins

- Gross Margins - I think they have some leverage here, and in the future during a difficult time they could potentially raise prices to manage margins at 30% (they have private label which could be increased to enhance margins)

Just coming back to cash flows – I think we agree that the business can generate ~40 – 50 crores per annum of operating cash, and assuming the economy picks up, it could potentially be higher. The business is debt free currently, and can be leveraged 0.25 – 0.3x (50 – 60 crores) to open new stores in case cash flows do not materialize as planned. As the business scales, the operating cash flows will only increase significantly allowing internal accruals to move up.

Obviously, the risk you mention remains, and the bet is on management capability to maneouver the business in the right direction in times of a slowdown, as they have demonstrated in the past. Any investment in V-Mart (or any retail company) will need to be monitored more closely than the average stock investment. Currently, I do not think the stock prices in very high growth expectations as we may get EPS of ~25 in FY16, so the stock trades at ~16-17x forward. I hold from lower levels, and would be comfortable to buy in good quantities near 13x-15x, given I see a significant runway for growth ahead, with measured risks. If the management executes the way it has in the past, we could see significant positive surprises.

Risks that need to be monitored on an ongoing basis

-

Slowdown in same store sales growth – hurts overall profitability and slowdown the Company

expansion plans - Competition – As larger players enter these markets or even e-commerce companies penetrate further, Vmart growth and economics could be challenged

- Inventory and debt – Any signs of trouble will reflect in inventory and debt piling. Need to be monitored closely

-

New store openings – same store sales growth will be driven by new store openings, and

this needs to keep increasing by 20 – 25 stores per annum

Disclosure : Invested from lower levels, and continue to remain bullish on growth prospects

3 Likes

My background -

I have done MBA in retail management.

I own a apparel / family store in very small place (tehsil / taluka) place in western Maharashtra. (current city population = 2 lakh).

My store is approximately 8200 sq ft and it does psft sale of Rs 6200 (approximately).

Comparison with above discussion -

Store size

- 8000 sqft is nothing much, at least in western Maharashtra. You will find at least one store of 8000+, 4 store of 5000+ and least 10 store greater than 2000 in many cities, with population less than 3 lakh.

SSG rate

As already pointed by someone in above earlier post, inflation is around 6 - 8%. So even with almost same quantity sold, you will get sales increase automatically.

Dead stock

This is biggest problem in any apparel shop.

Smaller or single store like us, pay very close attention (almost weekly). We usually purchase as and when needed, instead of buying everything before start of season.

But even after this, most of us are stuck with dead stock of 10%+

For organized retailer, buying process usually start 6 months before product arrive at store. In this process, there is far greater chance of products becoming out of fashion.

Advantages of geographical spread / bulk buying -

This is difficult to achieve in apparel retail.

Reason being with every 100km, choice changes.

Eg in western Maharashtra, white and sober taste are most preferred. While if one move towards south, karnataka, dark color are more preferred. If one go towards north, Gujarat, fancy work is more preferred.

Also, each caste / religion has their own taste / preference in apparel.

Eg. Hindu / muslim and jain / marwari needs very different types of sarees.

So even if a retailer has stores spread across India, he has little advantages of bulk buying.

This is beautifully explained by Kishor Biyani in his book. Refer to white shirt example.

Competition -

There are low entry barrier to start apparel store and competition is intense.

In late 4 Years, at least 15 new shops (Avg sqft 1000+) has opened in my city.

Then there is also competition from branded segment.

Raymond, Peter England ( i own this one), Cotton King has opened franchise in my city.

Man power cost -

This is biggest issue for me. Apparel is still seasonal business.

You just can’t hire new salesperson and fire him once season is over. This is because you need to give training to sell apparel.

Currently i spend 5% of my sales on apparel and Avg cost per employee per month is approximately 8000 - 12000.

It is very serious problem and organized retailer do face problem on this front.

Other Overhead -

Other overhead like electricity bill, municipal taxation remain same but organized retailer needs to pay rent while most of shop owners have their own property.

Distribution network -

Since fashion keeps changing and customer always want something different from what he has seen last time, it pays to buy from wholesaler, rather than manufacturer.

There are few items for which we do buy from manufacturer ( we go to banaras, Ahmedabad, surat, panipat, Amritsar, Indore, Jabalpur, Erode, Madurai and many other places)

But at the same time, we buy more than 50% of our entire purchase from wholesale market ( MUMBAI, Indore, Amravati, gandhinagar).

Every apparel retailer knows wholesale is least 10 - 12% costly than manufacturer but they also know that it far easy to buy than sell.

So even if organized retailer has edge of direct buying from manufacturers, it doesn’t make much difference.

Opening store in smaller towns -

I don’t precisely know why big retailer (shoppers stop / reliance) don’t open store at small cities but my guess is -

- Local Retail market is too small

- Their overhead are higher, so they need bigger sales to justify overhead

- Strategy (L&T construction division has strategy of not bidding any project below 500 Cr)

So strategy of opening in smaller towns has is no moat or doesn’t give much distinct advantage. IMO

Reducing FMCG / kirana -

Again this is not unique.

Future group is already doing this. I have visited few newly opened big Bazaar where first 2 floor were given to apparel / fashion and last floor was given to FMCG.

Even i remember, one of our visiting professor from future group used to tell that we have decided FMCG won’t grow beyond 25% of our sales. We are using it mostly to attract foot falls.

Disclaimer - I have not visited any v-mart yet but have visited and shopped at other organized retailer numerous times. (Pantaloon, shopper stop, big Bazaar, max, Reliance, more and many other)

10 Likes

Thanks Nikhil for sharing your insights

However if you compare the other group entity v2 retail, it has actually done well in penetrating in tier 2 and tier 3 cities which remains there core strategy.

Plus wanted to check how is the consumer purchase pattern in ur city vis-a-vis lets say a city like Mumbai?

Regards

Sreekanth

Nihil - thanks for sharing!

Sreekanth - while the promoters are related, v2 retail and v-mart are not part of the same group.

Thanks for this valuable input. This was already coming through the financial numbers of the business - but best to hear it from an expert…

Consumer purchase pattern - can you be more specific?

Regarding fashion trends -

Most of time fashion trends starts from Mumbai. Gradually it enters rural areas.

Eg. Printed shirts trend started at least a year back in Mumbai. Retailer from PUNE (130 km away) started selling it from 6 month back.

We will start pushing printed items heavily from diwali (my town is approximately 400 km from Mumbai). But in Mumbai, you will see, from this diwali, printed items being replaced by something new (jeans shirts).

Then fashion will reach border towns of Maharashtra and karnataka (Belgaum, hubli, Gulbarga) ( approx 550 km from Mumbai).

Once it reaches Karnataka border, Pune retailer will stop selling printed items.

And once it reach interior of Karnataka, we will stop selling printed items.

So this way, fashion spread from Mumbai towards interior and it keeps changing every year.

Thus, you may find that very few store in Mumbai selling printed items but almost all stores from our side (western Maharashtra) selling them.

Thus for a organized retailer, who has store in Mumbai, Pune and rest of Maharashtra, it is very difficult to manage trend as it differ from city to city.

Even in printed items, choice of designs / color / material vastly varies from city to city.

So you can’t move out of fashion item / dead stock from one store and sell it to others store easily.

It needs customization on a city level.

So more city you cover, more store you have, greater will be the overhead and backend work, and more difficult to manage it from a centralized office / location.

IMO, this might be one of the reason why other organized retailer (Pantaloon, shoppers stop) are not willing to go interior.

Disclaimer - I have not invested in v-mart or any other retailers.

1 Like

VMart came out with steady results for Q1FY16

Sales for Q1FY16 has increased to 205 crore from 165 crore in Q1FY15 (24%)

Gross profit margins for Q1FY16 have increased to 31.3% from 30.4% in Q1FY15

Operating profit for Q1FY16 increased to 21.24 from 18.21 crore in Q1FY15 (margins declined marginally to 10.4% from 11.2%)…

Finance costs have come down due to reduction of debt in Q4…down from 1 crore to 50 lakhs

Net profit is up 25% from 9 crore to 11.2 crores (EPS increased from 5.03 to 6.21 per share)

Company has not opened any store in Q1, and recently opened one store in UP in July…need to wait for conference call for the reasons management gives for the same and plans going forward

Over 7-8 crores of cash would have been generated in Q1…so total cash balance of >25 crores, which should see rapid deployment in new stores this year…

Disclosure : Invested

1 Like

The results are good. But main point of contention is future. Multiple fronts of competition requiring to be very diligent on each step without competitive advantage may mean tough life for vmart.

disclosure: recently sold after remaining invested for 1.5 years.

1 Like

V-Mart – Concall Update

** Tied up Gartner to advise on tapping online potential and business model. Strategy is still in discussion stage. Targets 5% Sales from Online format by FY18-19.

** Seen consistent growth and lot of improvement on ground, particularly, youth apparel segment showing strong traction.

** Past 6 months not added any store, but maintained guidance of 18-20 stores addition every year. This year entering into Orissa and Bengal.

** Q2 is seen muted as major festivals has shifted to Q3. Further due to “adhik-maas” as per Hindu Calendar falls in Q2 which will impact marriages as well. But likely resort to high discount to improve volumes.

** Lot of focus going on in rationalizing vendors and inventory management. Last year have deployed online vendor service to track key data. No firm target on Inventory days but focus is to improve or maintain at current level of 82 days (vs 86 days yoy).

** Election in UP and Bihar to impact footfalls but management expect post Poll-period to see bump-up sales.

** Q1 saw fall in Material cost which was passed on to customer for improving value proposition to its customer which led to slight decline in realization during the qtr.

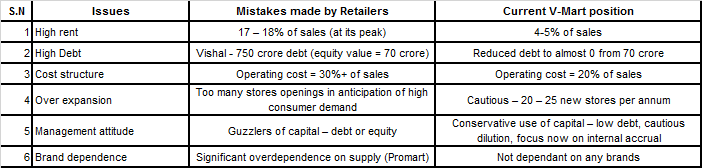

Thought not directly related to V-mart but this article will definitely help in understanding retail (specifically discount store) business better

1 Like

Thanks a lot @nikhildoshi for sharing the article. Am summarizing below some of the mistakes made by these players and where VMart is currently on those parameters. Of course, there is a big difference in the business model of the players covered here – whererby these are all discount retailers focused on metro or Tier 1, whereas VMart is a value retailer focused on Tier 2 and Tier 3 cities.

However, these are all critical metrics that need to be tracked for a retailer like VMart, and anyone invested should certainly keep an eye on each of these including the growth metrics (sales per square feet, store openings) and working capital (Receivables, inventory)

2 Likes

Sumir Chadha of Westbridge Capital in his recent interview summarizes rationale for investing in V-Mart…They own close to 20% stake -

V-Mart – fantastic retailer in Tier 2 & 3 towns selling low-cost apparel:

V-Mart is a fantastic retailer in India serving tier 2 and 3 towns selling low-cost apparel. I was in Haridwar last summer for personal reasons. Then I went to visit the V-Mart store there. The store was packed. It was a better shopping experience than other stores. They have air conditioning. They have prices on everything, so no negotiating. They have changing rooms for women. If you are buying on the street, you can’t try something on. They have very low prices. Literally, their prices will compete with the street vendor because they cut out a lot of the middlemen in the distribution chain. We own a big chunk of the company.

1 Like