I remember reading in a management interview that Bandhan Bank 100% advances are backed by deposits only. Given how much Samit Ghosh looks up to Bandhan, this is what he may be striving at. If that happens, I will be a happy long time investor in the stock.

1 Like

One reason for IndusInd’s high valuations could be its lack of fragility in situations such as demonetisation. Having said that, Ujjivan as a SFB should be much more robust now. If Ujjivan can demonstrate a consistent return over the years then I think it too would command significantly higher valuations.

Yes absolutely. They are susceptible to tail risk and hence it should and will be reflected in valuations. But p/b of 2 is still low if they get over their issues.

Okay Mayank. The three research reports shared by @lohiyaakshay08 above all talk of a target of around Rs 450 per share, assuming a book value per share of around Rs 190 as on 31/3/20, assigning a p/b of around 2.3. At currently bvps of Rs 147 that would be a p/b of 3. Let’s see how things pan out over time.

1 Like

Samit Ghosh at Annual Banking Conclave held this week in Mumbai-

1)Restrictions on small finance banks should be eased out gradually. If the restrictions are not eased they may end up like regional rural banks.

2)Interest rate hike worrisome for us(due to large wholesale funding). In our case (lending to informal sector), it is not easy for us to hike rates. We have to absorb a lot of it

2 Likes

Here is my investment rationale for Ujjivan:

Currently, AU SFB is richly valued at 8-9 of P/B. however the difference between Ujjivan and AU is the book composition. AU is strictly in MSME whereas Ujjivan is MFI. But as guided by management, over next few years they would like both to be at 50-50.

Also, Ujjivan has better pan India presence. They are targeting 470 branches in 3 years, which is going to be great for a small bank. I believe with decent growth prospect, liabilities outreach and balanced book between housing, msme and mfi, they can easily get p/b of 5-6 in the future. All depends upon management execution.

Ujjivan has high cost of funds currently. Given there is much scope for improvement here, and with ease of restrictions for SFBs, their ROEs could improve meaningfully going forward. Bandhan has an ROE of 28%.

I think MFI turned banks offer the best of both worlds, their coF would come down to lets say 6-7.5% while their yields will remain northwards of 15-17%. Such huge spread! Also, Ujjivan had a GNPA ratio of under 0.5% pre-demon (the group model model). Though such tail risks remain.

Can you please quote the source for the about figures?

Bandhan’s Annual report and their DHRP.

Dont we have a thread for Bandhan Bank? Would be great to dissect it before the upcoming IPO

@lohiyaakshay08 even currently their avg cost of deposits which are almost totally institutional, is 7%.

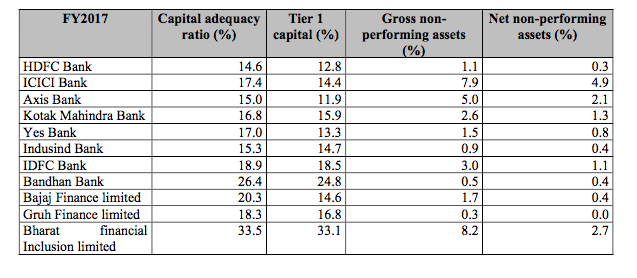

Posting from screenshots from Bandhan’s DHRP. Its a treasure trove on the IndiAN FINance scenario.

Bandhan clearly stands out on all parameters

12 Likes

All the numbers are FY17 based. Just 2 quarters later, 2Q FY18, the GNPA has moved from 0.5 to 1.43%. Haven’t checked the other numbers yet but the jump us quite high (even considering demonetization impact)

Surprised that they didn’t mention SFBs in the NPA colums. Ujjivan had a GNPA of just 0.28% at end of FY17  and look how much they rose across the board from q1

and look how much they rose across the board from q1

In q3fy18, Ujjivan on consolidated basis has GNPA of 4.24%.

1 Like

Budget effect: The finance minister has allocated Rs. 5750 crore to the National Rural Livelihood mission to create employment in villages. Ujjivan caters to mostly rural customers who are self-employed and do not have access to easy credit and thus stands to benefit from this.

Source: Moneycontrol

Update on chart:

Such a clear price channel. Fall below trend-line clearly was due to market selloff. Refer this for patterns: Price Channel [ChartSchool]

2 Likes

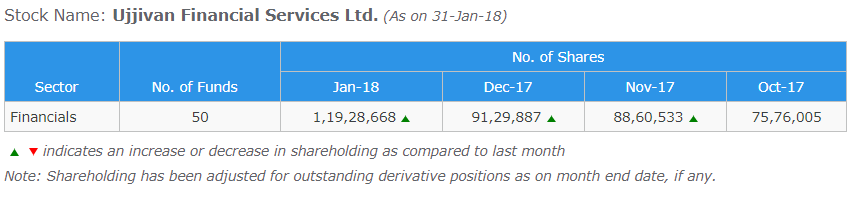

Thanks for the valuable piece of information! The big increase in ownership seems to have happened during January 2018. However, share price did not move up during the month. Any idea whether Foreign owners sold their stakes, which DIIs may have bought?

Yes, CDC Group PLC sold 22+ lakh shares

Hi Akshay, where did you get this information?