http://www.ujjivan.com/pdf/Ujjivan_Annual_Report_2017.pdf annual report

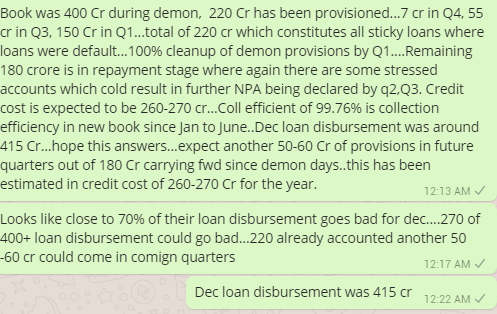

Ujjivan NPA impact in One Pic…Impact of Demonetization on Ujjivan.

Disc: Invested

1 Like

96% is cumulative efficiency…This has been factored in now. Ujjivan should see sharp rebound.

1 Like

If Goldman has no conviction in this stock then it is really difficult for others. Most of similar companies are doing great and in this bull market.

Disc :- Exit complete.

Are you talking in terms of stock price or in terms of results? SKS posted bad numbers too. I don’t track other companies but it will be great if you can detail about the comparison you are making.

My 2 cents

One reason I could think off for Goldman Sachs is earnings visibility… i.e Q’1 18 PAT 75 cr Loss( Still 70 to 80 cr credit loss to be provided)…, Capex for SFB conversation branch cost…for FY18… 170 Branches( 50 cr approx) , and FY 19, 175 Branches and FY 20, …80 branches. Each branch is required 3 millions capex ( per FY 16 AR)., … So literally for FY 18 it may oing report losses or little profit against profit 207 cr FY 17 ( 177 cr in FY 16)… SFB conversion cost still continue for FY 19 also … which is close to 50 cr…

Positives could be savings in borrowing cost ( approx 1.5%)…

With this back drop next two years seems to be little difficult to grow bottom line… However their long term prospect s are still in tact…

If you have time horizon beyond 5 years …I don’t think is there any issues in this counter…

Dis : Invested at current levels.

That is exactly my thoughts…I think it may take a while before Micro Finance companies get the kind of valuations they were getting per-demonitization level. Micro finance is no more a Market ‘favorite’ sector…Look at IT and Pharma…they are great value but then last two years they have practically not done much from the returns perspective. Micro finance companies will have to show consistent growth for couple of quarters to expect re-rating by the market so it looks like a time correction for them for now.

Disc : Exited my positions earlier this year

1 Like

this makes me tad wary as they were very prompt with the data & eff earlier !

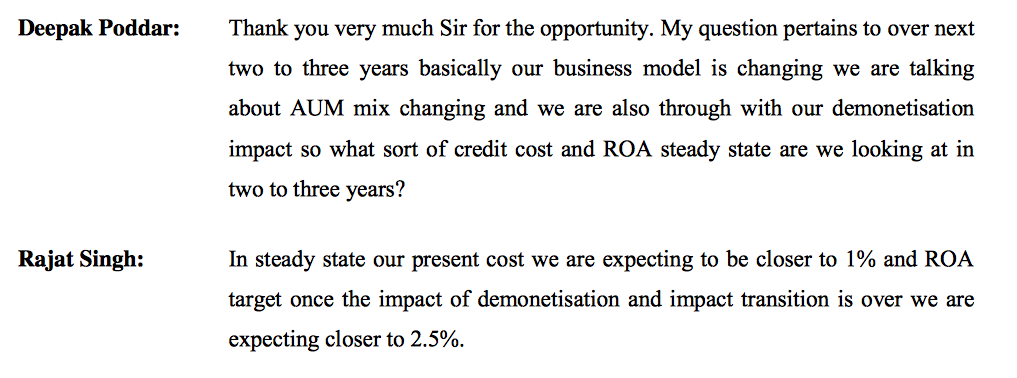

In the opinion of those who have invested in Ujjivan, what is the average RoA & RoE that the company is likely to generate once conversion to SFB is complete?

As the per the latest con-call, the company expects a 30% AUM growth from FY19 onwards. But they also say that RoA number is likely to be around 2.5% which actually makes the RoE probably sub 15% which is actually quite unattractive.

I have a significant portion of my portfolio invested in Ujjivan since IPO days because the crux of my reasoning was strong AUM growth, higher than usual returns on the loans made by them & available at reasonable P/B & P/E. But with average RoA & RoE projections my thesis has come into doubt.

What are the views of fellow ValuePickrs? Why are you holding Ujjivan?

1 Like

2.5 % of ROA is good number to have even HDFC has 2.6% ROA(FY 17).

My thought process to hold this company is: It could growth 15 to 20% in top line and bottom line ( FY 18 should be exception) and ROE is around 15 to 20 % ( average basis over period). With these numbers it could give above reasonable return over long period of time.

Dis.Invested.

1 Like

RoA of Ujjivn and HDFCs my not be directly comparable. With RoA of 2.5%, 20% RoE would imply a leverage of 8 times. This level of leverage appears to be high for Ujjivan, which is mostly into microfinance. HDFC has lower business risks and can afford higher leverage and generate higher RoE.

3 Likes

There is an update regarding the Ujjivan financial services on Moneylife. If anybody have access to premium content please share the highlights.

Most of the information is already in the Investor presentation. Nevertheless, below are some points.

Ujjivan expects to wipe out the credit losses and become profitable in the next two quarters. Mr Ghosh estimates that the SFB is likely to recover its losses by end of the financial year as its provisions have ‘peaked’ in the April-June quarter of the current financial year.

He expects a loan growth of 20% during the current financial year. The SFB’s loan book grew 10.4% during the reporting period.

The margins are expected to improve after it is notified as a scheduled bank (expected in Sep 2017).

3 Likes

Yes…Nothing great in article as such. But will share it with above IDs.

1 Like

Vijay thanks for the Report.

1 Like

Thanks for immediate response

1 Like

Thanks for the mail…

1 Like

Can anyone Explain, what is Ticket size in financial institutions?