Stock hasn’t moved with market recently because of:

- Demonetisation effect(higher NPAs) expected in this quarter(RBI guidelines allowed them relaxation for a quarter)

- Higher investments for 2 years on technology for Small Finance bank

- Overall negativity with the sector after demonetisation

However, over the long term stock should do well as the effect of investments would kick in terms of low cost deposits and business would move from group lending towards SME and housing loans

Disc: Invested

Ujjivan converted 5 of it’s 9 branches to SFBs in Delhi.

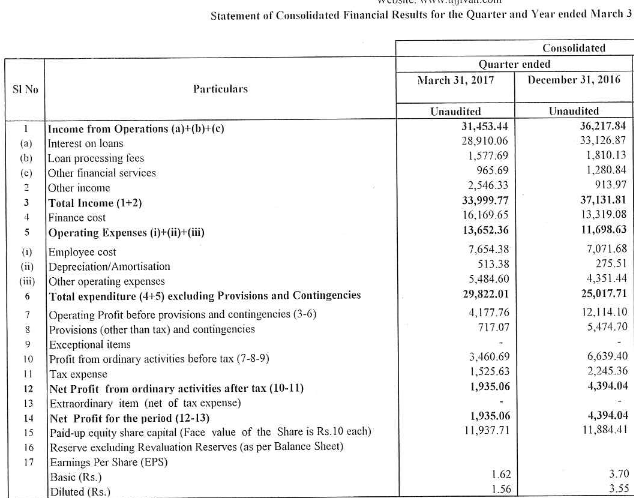

Results for quarter are out and there is a big dip in net profit qoq.

Interest on loans has taken dip of 12% from 331cr to 289cr and

finance cost had increased 22% to 161cr from 133cr.

Provision for the quarter are 7cr compared to 55cr last quarter. I could not understand what could be the reason for increase in finance cost and simultaneous decrease in Interest on loan.

Is it pointing to massive build-up of NPA for which no provisioning has been done?

From what I understand is that it might be that the company has stopped booking interest income on a portion of loans which were treated as NPA post demonetization which resulted in lower interest income than last quarter . The loan processing charges for the quarter are also reduced indicating a slow growth in the loan books and their obvious shift of attention to stepping up their SFB business . Consequently there is an increase as u pointed out in the Finance Costs might be related to the increase in SFB assets development and might be due to some other factor I can’t conclude for the time being . The increase in operating expenses and emp cost can surely be attributed to their increased focus on SFB. Overall feel the results are not as per expectations but haven’t lost any faith in their business model .How markets treat them tommorow will be a point to note . It’s not as bad it looks prima facie but yes cant be termed as good either

1 Like

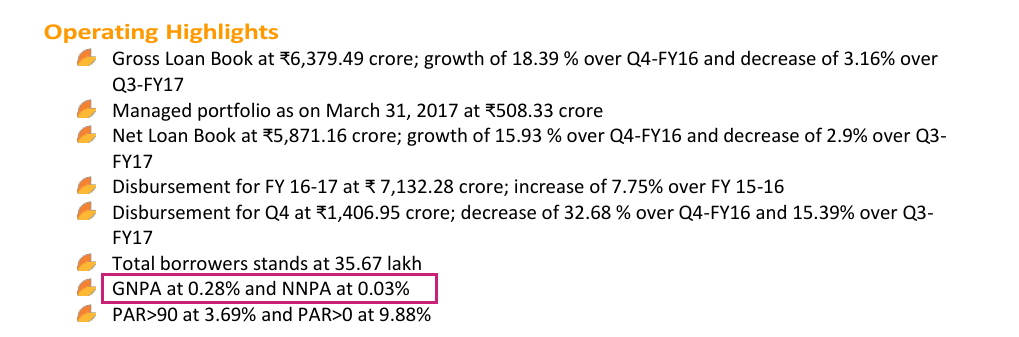

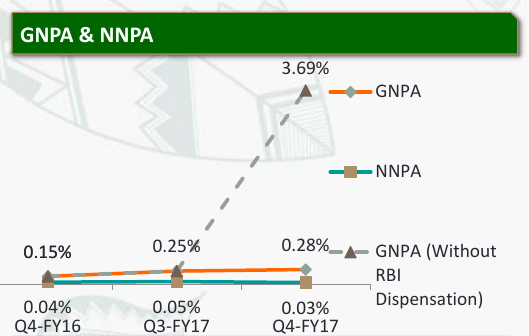

Without RBI dispensation, thet GNPA stands for 3.7%, Big worry.

Profit has decreased from last quarter and so income.

Mgmt has been transparent – > Positive

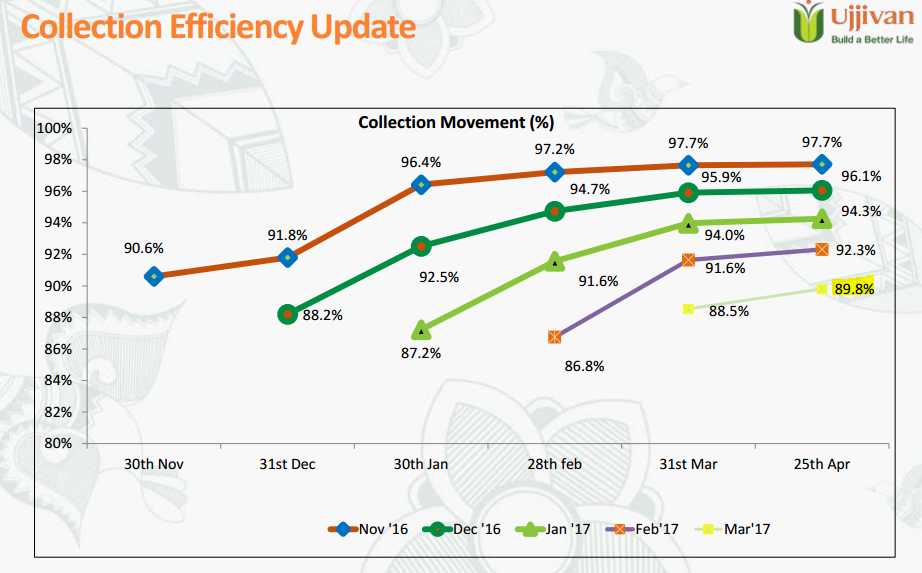

Collection Efficiency does not seems to have improve materially as per the charts below. however, the mgmt is saying they see a significant improvement in March.

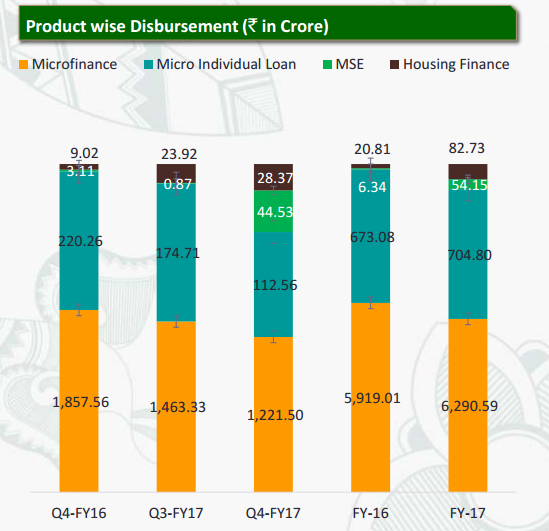

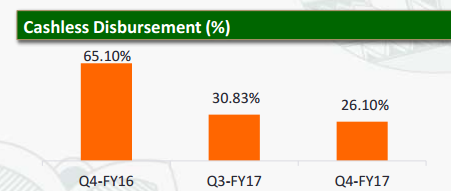

Product wise disbursement has improved. Big positive is MSE, housing finance taking bigger share of pie and thereby slowly reducing loans for MFI and Individual lending. This may further help to reduce risk in terms of NPA issue.

Cashless disbursement continues to improve.

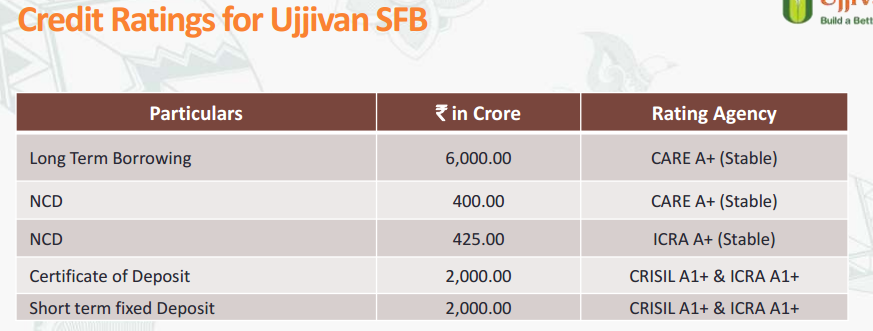

Credit Ratings Stable

Continue to hold. I think Transition to SFB will be a significant driver of future growth with good loan mix to housing finance, MSE, MFI and Individual lending.

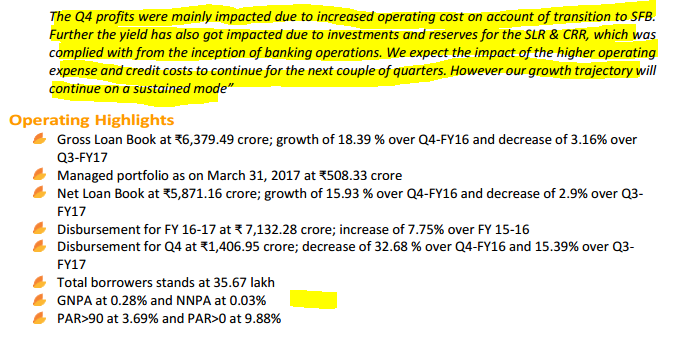

Mgmt has guided that RoAA lower on account of:

Impact of increased operating cost (SFB transition)

Increase of asset base (SLR investments)

Mgmt has guided that next 2 quarters will also see some hit.

Cheers,

Amit

Disc: Hold (Part of Long term Holding)

1 Like

@aammiitt2

Can you explain the collection efficiency graph?

Thanks

Yes today morning when I saw the investor presentation the cash collection efficiency part seems a huge problem to me . I think this is a result of these 3 factors and see that the tide is not over for MFI sector

-

Cash shortage post the demonetization. Even now in cities like Mumbai I see ATMs with boards out of cash which is not the best

-

the farm loan waiver part .

-

the governments thrust on digital payments

I don’t think there has been much of improvement from November to March in terms of cash collection efficiency and hence feel that this needs to be checked each and every quarter . While in the investor presentation they have mentioned 6 or 7 states/ UT where collection efficiency is less than 90% . This included Maharashtra / UP / Delhi

The cash collection graph tells a story and if we are to believe the story does not seems good . Checking it closely u can see that there hasn’t been any improvement in cash collections . I don’t know why their CEO has stated improvements in March 2017 . The chart does not validate her point

Collection Movement graph – > This is collection movement chart. if you see the top line in graph (red colour), it tells you that loan given in Nov has not been fully collected. So, they managed to collect 97.7% of Nov disbursement till April. Usually, MFI does collection efficiency monthly on monthly repayments.

MFI efficiency is better measured by the operating expense ratio. The borrowers per staff ratio measures productivity. The operating expense ratio measures the institutional cost of delivering loan services. The lower the operating expense ratio, the higher the efficiency of an institution. The ratio is affected by portfolio size, loan size and staff salaries costs.

MFI efficiency is therefore better measured through two ratios: Operating Expense Ratio and the Borrowers per Staff Ratio.

Operating Expense Ratio= Operating Expenses ÷ Average Gross Portfolio

The borrower per staff ratio was computed as follows:

Borrowers per Staff Ratio= Number of Borrowers÷ Total Staff

Cheers,

Amit

Thanks.

Does collection efficiency graph means that out of the loan which were due (money which has to come back to Ujjivan from borrowers) in November only 90.6% have come back?

And only 97.7% of loans which were due in Nov-16 have been collected till Apr-17, which brings their GNPA to around 3.x%.

All Nov repayments have come back 90.6%. It does not mean full principal. However, it is coming with a lag. Yes, 97.7% of loans where repayments were due in Nov-16 have been collected till April -17.

Gross NPA means total value of loans on which interest income has not been received by the Bank for more than 90 days, divided by total loan portfolio of bank. Nov interest income which has not been payed is part of the GNPA of 3.7% but it includes other months as well.

Ujjivan will test your patience and long term thesis for atleast next 2-3 quarters (qayamat se qayamat tak).

Amit

I am surprised to see that their collection efficiency was decreasing all the way till February. They (as well as us investors) are walking the tight rope. Management must be under sever stress; fighting demo as well expenses increase due to SFB.

I will believe management is transparent in reports but have tried to present rosier picture during the interviews on TV. In none of their interviews in Jan they have mentioned that their collection efficiency is still going down.

Also once they have chosen not to take RBI dispensation they should have kept-up with that. In one of the interviews I remember MD saying that their GNPA is 0.2x% whereas it is 3.x%.

In future, I will take their words with a pinch of salt.

Gaurav,

I urge you to substantiate your claims (TV interview) with a source. Otherwise it may affect retail investors. You could be mistaken for Net NPA.

Mgmt is doing all the right things to dilute the risk by keeping a better loan product portfolio. Ignore the ticker for 2 quarters if you can and you will see better results.

Mgmt is as good as us, they cannot predict the future. They have guided based on opertional ground reports. Overall, in all investor presentations they will try to paint a better picture. It is us who needs to find faults in there guidance and bring forward but with evidence. I hope you may join today’s con call and get better picture before forming your opinion.

2 Likes

The reason for increase in finance cost and simultaneous decrease in interest on loans could be additional borrowings used for deployment in CRR & SLR. However, the presentation does not reveal how much this is. Someone can please ask this in the concall today.

A couple of more points that need to be clarified:

- What is the absolute level of Gross NPAs as of 31-Mar-2017?

- What were the write offs for Q4 and full year FY17?

3:12 - When asked about collection efficiency. She replied collection efficiency of November has increased from 90% to 95%. She continues and say collection efficiency for December has also increased in January, conveniently hiding that collection in December has fallen from 90% in November to 88%.

6:12 - Anchor asked about NPA number. Trying to dodged the question. On Anchors insistence at 7:34 (Do you disclose NPA numbers or not) She replied (with lot of fumble) GNPA = 0.25% and NNPA = 0.05%

Also look at the page 2 of q4fy17 presentation released yesterday, why do they choose to mention GNPA with RBI dispensation, when they have publicized that they are not availing of the same

It is only when one goes inside the presentation one realize that GNPA are 3.x%

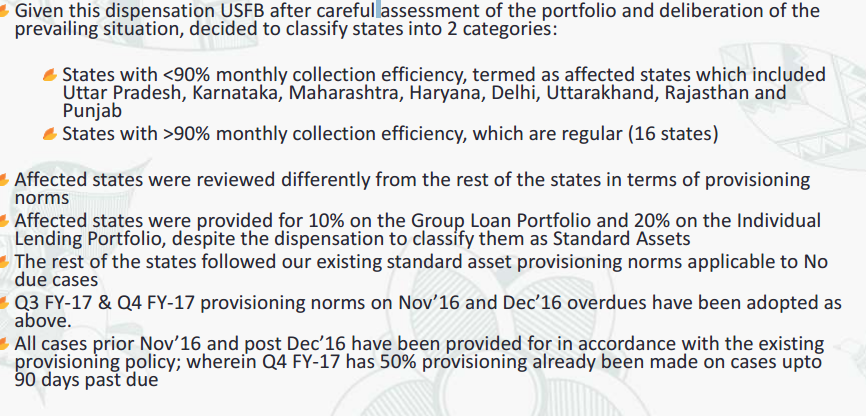

RBI in its circular released in Nov’16 and Dec’16 provided additional 90 day dispensation before

classifying an asset as NPA on Nov’16 and Dec’16 overdue accounts (in effect upto 180 days) .

If they choose to take path of RBI dispensation, it means they cannot recognize their NPA on Nov’16 and Dec’16 overdue accounts for 6 months

Nov Account → Till May

Dec Acc – > Till June

That suggest they have NPA in the books at 3.7% if they choose not to go with RBI dispensation.

Read this v carefully,

For Affected states, they declared 10% on group loan and 20% on Individual loans as NPA despite RBA dispensation scheme to classify them as standard asset. So this suggest more issues on NPA side with individual loan than on group lending,

For affected states, they use RBI dispensation as follows,

Out of group lending provisions they are not recognizing 90% of provisions yet as NPA. They call it as part of standard asset as they are hopeful they get repayments with lag.

Out of individual lending provisions they are not recognizing 80% of provisions yet as NPA. They call it as part of standard asset as they are hopeful they get repayments with lag.

Cases prior to Nov, Dec 2016, they have declared provision as per the provisioning policy. Check last quarter q3 presentation. They chose to declare them as NPAs in Q3 as per my knowledge. I could be wrong.

In Q4, where they have not received repayments past 90 days they raised them as NPAs (Provisioned) to 50% Remaining 50% provisions they will carry forward as standard asset. However, if they will not receive repayments in next quarter for Q4, then they will be declared as NPAs.

From Mgmt guidance, 2 more quarters could get affected. They are conservative mgmt and I expect only next quarter to have more NPAs before story gets better.

Hang on if you can till next quarter and hopefully you will see a sharp V shaped recovery unless Modi ji throws another Demo.

Cheers,

Amit

7 Likes

One thing is very clear from this discussion, that one time black swan events like DeMo do produces definite short-to-medium term troubles for company like Ujjivan. But looking at the overall broader picture over long-term, if one is quite confident of recovery in the underlying business with transformation from MFI to SFB and ultimately with a vision to be a universal bank, over next 5 years or so along with sound management with past track-record, a long-term investor should be more than happy to buy it at any serious price correction, provided the execution remains on track with intermittent volatility

Discl:- Invested since IPO & added during post-demo correction. Would add up more if it reaches or falls below post-demo levels.

7 Likes

GNPA including demonetisation period is at 3.7%: Ujjivan Financial

Concall details are available on researchbytes . If u include the RBI relaxation the GNPA is around 0.30 % while without it the GNPA is 3.7% as u pointed out .

A quick view of the points i can recollect from the concall.

In the concall they have mentioned that PAR of around 41000 accounts who have not paid a single installments since DeMo is around 70 crs. Out of this a provision of round about 60 to 62 crores has already been made in Q3 & Q4. Atleast 53% of the accounts who hadnt paid a single installment post demonatization till Feb started paying atleast 1 installment in March. No new customer additions in any branch where the Collection Efficiency is less than 95% . Stronger growth in coming quaters to come from MSE and HF divisions. Higher borrowing on account of CRR/SLR requirements for SFB which was taken during last 2 months . All the Asset Branches to be in the same premise with Liability branches. Current year around 170 SFB branches to be opened. Branches will be self sufficient in approx 3 years. Operating Expenses to Operating Income to remain high at approx 70% for the current FY. Basic deposit (term/savings ) services to be continued in the current year . From 2nd year onwards secondary value add services to be introduced. Heavy expenditure incured on infra and IT and SFB branches are on par in quality with some universal banks . Problematic areas in MFI West UP and Bangalore . Will look at Prioirty Sector Lending Certificates as income source in the coming months

6 Likes

Very good read and analysis on demonetization impact. An excerpt below-

As Samit Ghosh, CEO of Ujjivan, sees it, “Something like demonetisation impacts the unorganised sector the most. Mr (Narendra) Modi realised that employment for the masses who come in from the countryside is provided by the micro and small businesses. The government had taken such good measures like MUDRA, to promote these sectors, but unfortunately demonetisation impacted them the worst and consequently set back the whole process of providing gainful employment and livelihood through MSME businesses. I think that will have a long-term negative impact.”

1 Like

can’t read the article. paid website

1 Like