Here is one issue I found in their balance sheet.

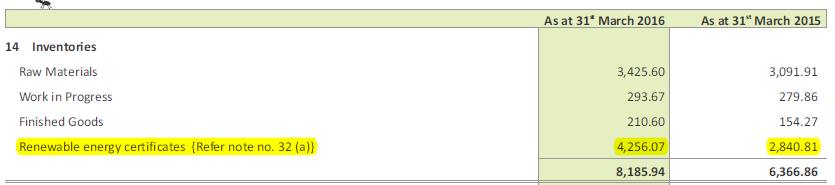

They carry an inventory of 42 Cr as of March 2016 of renewable energy certificates (REC) up from 28 cr last year.

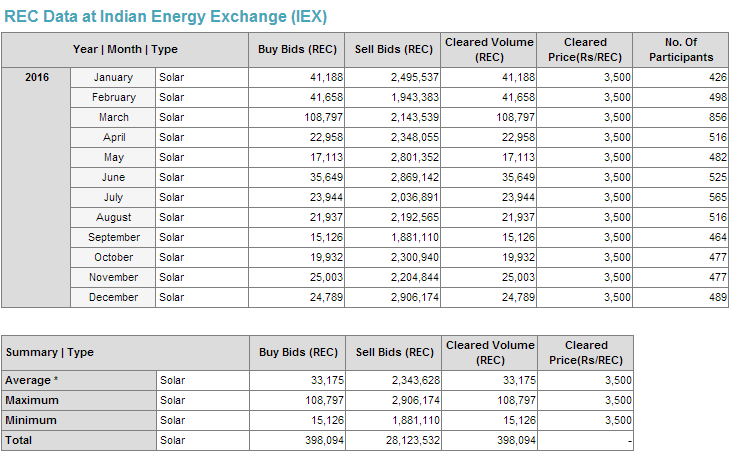

These certificates are valued at Rs 3500 each which is the lowest price set by CERC. These can only be traded on CERC certified exchanges on last Wednesday of the month (tomorrow). In the past, sell offers were 40 times buy bids indicating that there is huge supply of these RECs relative to demand.

One REC equals 1 MWh of electricity which translates to Rs 3.5 per KWh. A buyer who has an obligation to purchase renewable energy has to either buy an REC or buy the renewable energy from the producer. Non-solar RECs sell for Rs 1500 which is also the floor price set by CERC.

Since REC on offer far outpaces bids, Ujaas may never be able to sell its inventory of REC and will have to write if off once they expire. Moreover, in FY2015-16 they capitalized 14 Cr of RECs as inventory. If these were written off, FY2015-16 income would have dropped from 20Cr to 6 Cr or about 70%.

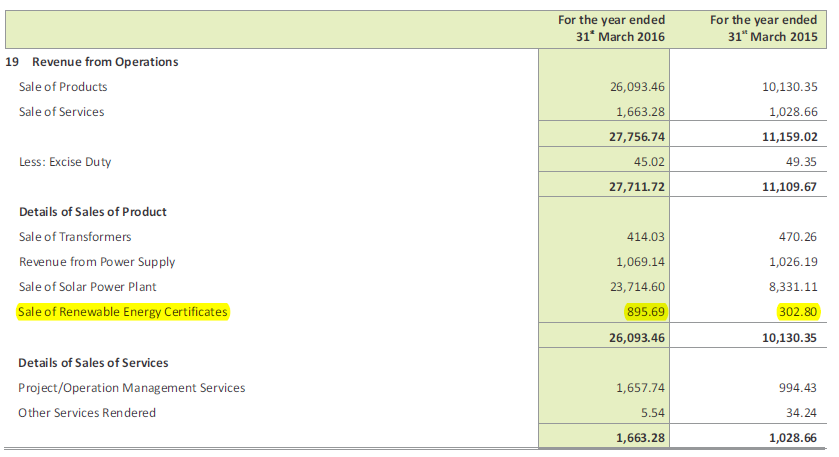

They derived about 8.95 Cr of revenues from the RECs they managed to sell.

This effectively means their EPC business and all other businesses are not even breaking even if you exclude the revenue from sale of RECs and capitalized RECs.

Good point. However they dont have to pay any cash to procure these RECs right? so how will the write off impact them if they havent even paid anything for it?

When inventory goes up cost of goods sold goes down as COGS = opening inventory + purchases - closing inventory. If closing inventory goes up, COGS goes down and operating profit goes up. If they had valued closing inventory based on how much RECs they will be able to sell, it will be much less that 42 cr. My estimate is closing inventory should have been 2 Cr and opening inventory should have been 1 Cr (instead of 28 Cr) so their COGS is understated by about 13 Cr. If you take that out of bottom line, it drops to 7 Cr from 20 Cr.

Today in CNBC, Anurag Mundra, the Jt MD had a chat. There were two doubts

raised. 1) The auditors had put in a some qualification privately with the

company. Was that true. Anurag replied that, not now, they had never got

any qualification from their auditors privately. 2) There is a rumour that

there is a lot of sales recall which is not yet reflected in the books.

Anurag replied that there is no concept of sales recall in Solar EPC

business. And all their projects are doing well with their customers. he

also clarified that their board is very independent and they have a high

ethics in the board. Sounded very positive and it felt to be very soothing

as an investor…

This news may be already known…Not sure Ujaas will participate in this,

since the terms specify that the developer must buy back the power

generated from railways…But Ujaas could be a sub contractor for many of

the companies which will bid for this…

Regarding the REC being carried as inventory, that is compliant with standard accounting practices

and had been discussed in a concall before 1 or 2 years. Earlier the floor price for an REC used to be Rs 9,300. The industry (including Ujaas) lobbied for lower (and more rational) floor price, which resulted in today’s floor price of Rs. 3,500/ REC. In this quarter’s concall management has indicated possibility of still lower floor price of Rs. 1000 to 1500/REC. In such a case, old inventory would still be cleared at old price (as at the time of issuing). Thanks @Yogesh_s bringing up the point.

That’s true Amit, but I’ve seen rumours myself on a whattsapp group which talk about Ujaas Audit report saying no vouchers found for 40% of expenses and other negative remarks. I’ve also read the auditor reports and they did not make any such remarks.

We have to go by common sense and gut feel. If one is not ethical and is a

crook, it takes courage to come on TV and deny any rumour, and if he knows

it is true. Only politicians do it shamelessly. We also have to remember

that nobody has any proof of the allegations. Also, it is very easy to

cross verify what he is saying with their auditors and he will stand

exposed. It could also be that someone wanted to buy huge quantities at

lower prices and floating a rumor is the only way for them to buy it. If

they have to buy it without a rumor, the price will go 10% higher and not

lower.

The only communication from management for common shareholders is their

commentary on media. It is upto the individual investor to accept or dump

the commentary. If we ignore the commentary, we will be shooting in the

dark.

Those are just rumours, so lets stop giving credence to them. The person who forwarded such message made very clear that this is a forward, nothing more or less.

If market believes that such romours are true, it wont pull the stock down

gradually through the day. It will hit the stock on downward circuit on

opening or within 30 mts. this kind of a move atleast confirms that 100% of

market does not believe this news as true.

I find it hard to believe the reason given by the promoters. Getting loans could have been first option or selling stake at an agreed price once you finalize a partner. One can ask for premium as well while selling stake. Equity dilution (almost 3%) in such a way worries me.

Debt from promoters is a debt anyway from the perspective of the minority investors. How can it be different from debt from anyone else? did they say what interest rate they are paying themselves?