Installing Solar Power Plants is the business of Ujaas. However, it differs from Moser Baer:

1.) Moser Baer manufactures solar panels and has some wind farms, whereas so far Ujaas is following an asset light model incurring just opex as opposed to capex.

2.) Ujaas does more than just EPC - procures land, licenses and later helps sell RECs/fulfill PPA, carries O&M. They do this like a MF by buying plot of land and installing say 30 MW - then investors/SMEs can own a small share of this.

You are right in observing that Solar REC is the Indian version of Carbon Credit and that most of the solar modules are procured from China.

Ujaas buys the land, but it is later transferred to the investor. If someone owns 2 MW from the 30 MW park, their land, panels and substation are separately fenced. However, Ujaas still has access to the whole park for O&M. Land forms 2-3% of the total cost of setting up a solar park. Ujaas is not a trader. Any selling (one time) of RECs it undertakes is on behalf of it customers as part of the service package. Ujaas owns some unsold RECs on its own but that is from a 15MW solar park they set up for tax benifit, else all RECs are in names of the investors in the solar parks.

Till recently, for each MW setup, Ujaas would charge ~ 6.5 - 7 cr.(incl. all services mentioned above) of which 1 cr. would be PAT, and further 0.1 cr. annually for O&M with 5% annual increase for 20 years. This is the sole source of revenue.

Management refrained from giving any guidance but said that now they are back on track like the year 2013-14.

They are currently managing 130MW solar plants.

They have bid book of 100MW out of which they are L1 in 60MW (might be that NHPC order).

They’ve bagged 9MW -West Bengal order plus 10MW - Oil India Order.

From long term perspective, Government has target of 100GW by 2022. They said that they would grow 6-7x times of Solar Industry in India. Anurag Mundra did mention that they would be

managing around 5,000 - 7,000 MW in next 5-7 years. i.e. around 50x

Company has not yet entered the Household rooftop market.

For Rooftop business, there are two critical points - a. Enforcement of Net Metering Policy & b. A product which will suit the households with less installation time.

They are developing a solution for this market. In coming 2-3 qtrs, they will try to come up with that.

During the financial restructuring of various Discoms, there’s a condition for them to be RPO compliant. Anurag feels that it will be a good kicker for them. He sees situation improving in coming qtrs.

Apart from these points, other points were redundant though chances are there that I may miss some points

Discl: Invested small amount to track the company.

–> Are the profit margins in this business so low? Only 16%? Till I know this business is very lucrative.

–> There is one company - EIL which is an elephant in EPc works. It ranks no.1 in entire Asia (till I know). It has started entering into solar plants. It provides EPC services as well as owns solar parks like Ujaas does. Being Govt entity, I feel it will have an added advantage over other market players. It has more than 16 patents in its name, good past track record and good govt. backing.

–> This business can be a multibagger…But implementation of REC/RPO, net metering, solar cells manufacturing and only EPC service outsourced by clients going for more than 10MW projects - are issues which need to be taken care of.

–> Who are the competitors of Ujaas?

Disc: Not invested. New to solar business. So please pardon me for any mistakes. Want to have more clarity on this business and its future course.

The 14-16% margin was on solar parks which Ujaas constructs as an end to end service. Going forward, the revenues and profit will surely decrease on an absolute basis as cost of solar panels is decreasing. The margins also face downward pressure due to increasing competition, but not a lot since the demand could be really huge. In the coming 12 months, in particular for the recently bagged orders I expect margin to be lower as the orders are more like EPC.

In May or June RBI announced that solar projects of upto 15 cr (10 lakh for residential customers) would qualify for priority sector lending. This was well known in the market, but I am just reiterating as I saw the same across couple of channels and in an interview by Vikalp Mundra. In particular, what this means is that for new home buyers, they can get a roof top solar loan as part of the house loan package at lower interest rate. For the household rooftop panels margins would be higher, but if they go with franchisee model, the margins could be less. I prefer the franchisee model. Hope they come up with a product where a professional comes to your home and assembles modular off-the-shelf components according to your requirement - in this case your terrace and budget/KW. As mentioned in concall, If they can get the installation time down to 1 day (concall said 1-2 days), it could be a huge hit.

If Ujaas implements about 26 MW in next 12 months then on a very conservative basis they would get 15 cr profit. With the O&M and a few small orders, 20+ cr. is surely on the cards. At 360 cr, on a 12 month forward basis, this does not seem expensive. However, while buying, I always tend to look at the MoS and downside. Bought more in the last week. Call me greedy.

The Secretary of the Central Ministry of renewable power, Mr. Upendra Tripathi, informed that about 16 states have implemented net-metering policy. Watch the following video from 4:10

@chintans

Any idea on the RPO mechanism. Since quarters, there’s no improvement in RPO enforcement.

In every concall, Anurag implants hope through the Supreme Court and APTEL orders but things have not changed on the ground it seems.

To be frank I don’t have much idea. From a big picture perspective, the hope is that if govt. is serious about this, they will find ways to enforce compliance. Coming to the specifics, I am hoping that there will be a rush as March approaches, since the RPO requirement is on an annual basis.

It has a bid book of 80 MW out of which Ujaas is an L1 bidder for 60 MW.

Out of this 60 MW, NHPC project in Uttar Pradesh is of 50 MW. If Ujaas wins this it will be a very big win. Orders expected in the next 1-2 months for these bids.

No plans to raise funds.

Debt to equity ratio is less than 1. No plans to aggressively cut debt.

REC enforcement still remains an issue. However, PSUs are coming out with tenders for solar park EPC orders and Ujaas has decided to focus on these orders in addition to the Ujaas Park turnkey solution (which would benefit a lot from REC/RPO enforcement).

These EPC tenders tend to have lower margins than turnkey solution. For our calculation of forward 12 months PAT, we assume PAT margins of 6.7% for EPC (management says 10-12%) and 10% for turnkey solution (management says 16-17%). The current order book is 40 MW, which comprises mainly EPC orders won from PSUs in last few months, but also some turnkey solution orders. These would be executable over the next 3-6 months. Assuming revenue of 6cr/MW and margins @6.7% for whole order book, we get 16 cr. as PAT. From operation of Solar Plants, lets say a PAT of 12 cr. Last year EBIT from this segment was 25 cr. and these 9 months EBIT has just exceeded last 9 months’. Further assuming 20 MW from turnkey solution in addition to the current order book gives 12 cr. PAT. Total PAT comes to 40 cr. This is very conservative.

As a base case, winning the 60 MW in bid book which for which Ujaas is L1 (including NHPC tender, executable over 6-8 months), would translate to about 24 cr. PAT. There could also be more than 20MW orders from turnkey solutions business (Ujaas Park). I expect 60-65 cr. as PAT for next 12 months (could get delayed by 3 months e.g. if NHPC order is delayed), considering costs incurred in pan-India expansion.

Note that unlike L&T or BHEL, where the order book visibility could be upto 18-24 months, the order book is unlikely to give visibility for more than 12 months here as the execution time for solar parks is typically less than 6-9 months. The total bid book of 215 MW including 60 MW where Ujaas is L1 (mentioned above), and management decision of not incurring further capex, gives more confidence.

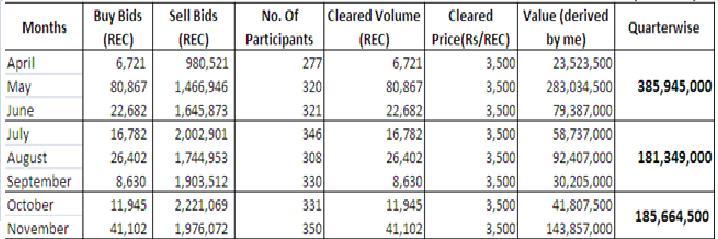

90,236 solar RECs were traded today @ Rs. 3,500/ REC. This is the highest number of solar RECs traded in a month till now. RECs are traded on IEX and PXIL. Since last 3-4 months, PXIL is also getting substantial number of bids; earlier IEX used to get majority of bids.