Got interested in the stock after going through @jitenp presentation … And started exploring in this forum. The concern about the management quality which was raised early on this thread is like an hanging knife on the stock. Is there a new management which is more credible ? If not, the rest of the story may not matter at all …

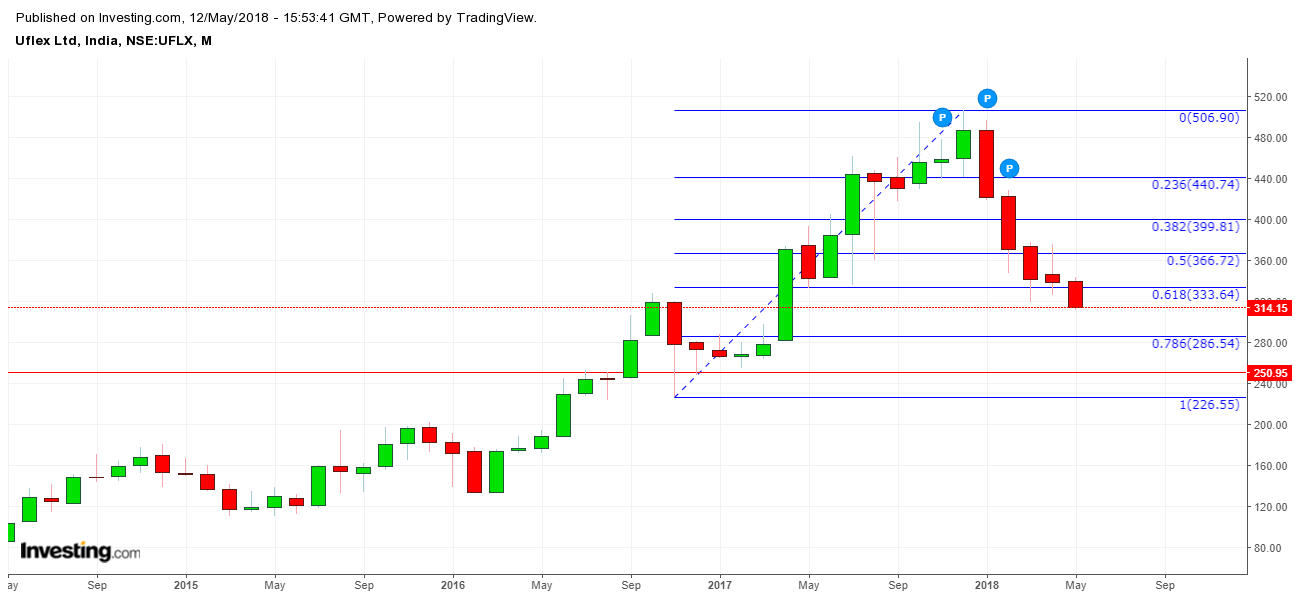

The stock looks bearish technically as it has retraced more than 61% of the prior upmove and next support on the monthly charts is 250-280. Below 220 (on closing basis) will mean a downtrend has started in the stock. (See chart).

Assuming the management quality has improved and credible, the business story remains intact, the falling price is an opportunity. What the technicals indicate is to buy in instalments to average cost or wait for a turnaround in the stock price sentiment.

@Chanrdrab saw in the thread you have significant investment in the stock. If you are still holding and following this stocks, your views will help those in dilemma …

When and where did I say, that my view is short term ? It’s a bit improper to pass judgements like “accidental long term”.

Anyway, coming back to Uflex. Business does face short term headwinds. Crude, stabilization of Asepto plant, input costs of paper, aluminium. There is always a lag element of these in the packaging business. So, this and maybe next quarter, results maybe subdued.

And I want to say explicitly, my views are long term in this business. As I view it as more and more as a packaging company, where share of commodity polyfilm business will keep on reducing.

Of course, these are views. Definitely, not any stock recommendations. One must do, what one is comfortable with.

Hello Shenbal, I have exited completely from UFLEX few months back, and stopped tracking this stock closely. Dec 2016 Consolidated OPM 14.03 %Vs. 11.61 % Dec 2017.Not sure the reason. Share is available @ very attractive price ( P/E 6.35 , CMP/BV 0.55 ). Based on March 2018 result , I will decide whether to reinvest in this counter or not.I believe they are yet to declare March 2018 Qtr. result. Best regards, Chandra.

The results were considerably better than market expected…The stock corrected by nearly 40% in last few months on anticipation of lower earnings due to increase is crude oil prices. LDPE, PP resins, the company’s key feed-stocks are cured oil derivatives.

Dear @jitenp nice presentation sir, looks like a promising bet with current price being half of book value and also at a low PE of 6 before any profit expansion from commodity cycle turning. I am prepared to ignore the promoter issues but a look in the financials threw up 2 points of concern, would like your opinion on those.

a) the tax payment even before deferred tax credit is extremely low

b) related point, inspite of huge profits and healthy cash flow, the company has not been paying dividends.

Coming from the perspective that management has been accused of cooking books, these points seem liek reg flags. your views on the same?

I have been following UFlex pretty closely from almost 1 year now. Being from the Print and Packaging industry myself, i feel the real game changer is going to be the Asepto Plant as there is virtually a huge market out there only running on a single supplier.

They are already one of the top players in normal flexible printing market , though the margins there are not attractive.

Disclosure - Invested . Currently adding to 300-330 Levels to Avg Down.

Q1FY20 concall notes-

Consol sales up 4%, EBITDA 8.6% yoy. Margin 14% and 15% excl engineering division

200cr sustenance (maintenance?) capex is needed for the whole business, higher share on packaging side

Divested stake in real estate biz which had 100cr investment. In Q2 we will have more clarity of deal, in worst case spill to Q3. Non core activity and Real estate has been languishing so lets get rid of it.

Engineering division-Subdued Q. Q1FY19 EBITDA was 25cr , Q1FY20 was 5cr. Capex cycle is put on hold by many cos so feeling the brunt. Can continue for 2 quarters

Ascepto- EBITDA positive already. Currently 43 juice customers, 6 dairy , 16 liquor customers. Better utilization in Q1. Large customers hve not converted, in absence of which we cant give a detailed guidance. Lets wait for next Q and see how we perform with large customers. 50-55% utilization guidance was based on assumption of getting some of top 5-6 large customers. What is hampering conversion… Branding, pricing, slowdown? We still not signed on dotted line…one large reason is testing for certain period of time. They are dealing with monopoly for long time and if they shift and if something is not right? Waiting out teething issues? ( My note: Large customer Can be a positive surprise anytime )

Margins improved slightly because of higher utilization. Packaging industry margins bottomed last year so can expect much better margins in next 1-2 years. Some consolidation also happened, few small plants got acquired, which were selling at low margins. See more consolidation and better pricing power for large players

More capex intensive than films business.

Films- Utilization almost 100% so volumes are static. Scope in Mexico to get more output but largely done with CU.

BOPP margins are better (spread 48 vs rs45 Q4). Q2FY19 was rock bottom for BOPP margins and now improving every Q. There was an overhang of excess capacity which kept prices low for almost a year. Q1 we saw 2-2.5% margin increase in BOPP films. Margins should improve.

BOPET margins also slightly better 8% qoq (Spread rs55). Continue to do good in India and globally. Polyplex, SRF, Jindal Poly also riding the wave. Demand growing 9-10% so new capacity impact on margins will be temporary and limited. Europe in net importer today, slowly we will move to a situation where imports will reduce. Indian players will substitute supplies with their plants in those locations. Eg SRF exports from India and setting up in Hungary.

Shifting BOPET facilities in Dubai to Russia by Jan-Feb. One line to be shifted and 1 line to be retained. This will impact volumes. Will fill orders from trading and other facilities. This plant was already selling to Russia/CIS so will save on import duty, freight, energy cost, shorter delivery times and higher margins. Margin expansion can be 15bps but mainly to protect the market from someone who is setting up a plant locally- SRF probably.

Hungary, Nigeria greenfield facilities (announced in Q4?) are on course. Placed order for machines. Close to achieving financial closure for Nigeria in 2 weeks, Hungary already achieved. It will commission in H1FY21

Low efficiency of domestic plants that were setup in 2003. Old machinery with lower output. New plants have higher output.

yoy growth on films is 35% standalone and 18% consol.

Case vs peers- Pure films players can return lot of cash to shareholders as we are riding upcycle. Uflex will be subdued because of other verticals engineering, packaging drag but there can be times when packaging issues will be resolved. We have to keep on investing because in future there can be regulations for recycling etc. Uflex is more diversified. Pure play BOPET cos riding a good cycle but look at BOPP players, barring Q1 they haven’t done that well. When will Uflex have all businesses doing well? Tough to say, maybe never.

Was hoping to see the ASEPTO branding on a few big brands this quarter. I think that can be the real stimulus to the balance sheet and the stock price too, however the testing periods are pretty long.

Still very convinced in the UFLEX story(Management quality a concern though) . Dividend track record is intact and holograms and packaging business regularly adding new customers.

Will wait for 250 levels before adding more though, what are your views on a 3-5 years perspective?

Asepto will be a very big trigger but as management said, the large customers are still in testing phase it seems. The convincing will take a while I guess. There was also a mention of “teething troubles in terms of new plant” so quality could have been an issue. My guess is that Tetrapack would also be trying to ward them off. But it will happen sooner or later. Once they sign up with a big customer, volumes can see sharp uptick.