Planning to buy the stocks on dips where I dont have exposure.

Sr No

Instrument

Sector

Avg. cost

%Allocation

Rationale

1

BAJFINANCE

NBFC

2869.5

4%

Higher net profit growth than historical averages

2

EDELWEISS

NBFC

150.45

4%

Good NBFC at lower PE

3

FCONSUMER

Retail

37.23181818

6%

Strong distribution network of future group, established brands

4

HDFC

Bank

1732.05

12%

housing push, Quality of book, strong returns

5

HDFCAMC

AMC

1171.51

29%

Exposure to HDFC mutual fund with liquidity

6

ICICIBANK

Bank

311.45

2%

housing push, Quality of book, strong returns

7

IGL

Oil & Gas

285.85

4%

Natural Gas push by govt, operates almost all CNG network in Delhi (33% of the indian CNG stations), owns stake in MGL (30% of the indian CNG stations)

8

INFY

IT

1384.1

8%

Leading IT company

9

MARUTI

Auto

8844.9

24%

Low 4 wh penetration in the country, market leader, nexa & partnership with toyota to cross the mid range band

10

YESBANK

Bank

218.79

8%

Attractive valuation at this level

11

Ashok Leyland

Auto

0%

pick up in infra (bharatmala, DMIC, ports) and mining will drive CV growth, also prebuying for BS IV

12

Britannia

FMCG

0%

Market leader in descritionary spending, increasing offerings, rural penetration, higher PCI, consumption story

13

Havells

FMCD

0%

Strong FMCD company with Loyd and Havells brand, penetration of gyser, fridge, air purifiers, appliances will increase in tier II cities

14

TCS

IT

0%

Leading IT company

15

HUL

FMCG

0%

Rural penetration, higher PCI, consumption story

16

BAJAJFINSERV

NBFC

0%

Had attended a presentation from company CXO, about how they are innovating to cross sell

17

ACC

Cement

0%

Infra, housing push will drive the demand

18

DMART

Retail

0%

Business model, penetration of retail spend in india, able management

19

RELIANCE

Oil & Gas

0%

leading Oil & Gas company with NCI complexity of 14 one of the highest in the world, will continue to export refined petrochemical products

It is general practice to also provide your conviction and reasoning for investing in each of these stocks, so that the much required perspective is clear to the reviewers. Kindly edit your post and add in this detail.

I notice that several of your picks have a weight below 1%. I personally don’t think that’s very helpful. As in, if any of those stocks went 10x in a decade, the net effect on your portfolio would only be a 10% increase.

Have you thought about consolidating your holdings? If not, I’d love to hear why you’ve allocated your capital this way.

Generally my underlining theme is consumption led growth

FMCG & Retail - penetration, increasing portfolio

Banks - Inclusion, Homes

Cement - infra, housing

Auto - again penetration & increasing income, aspirations

I am following market from a couple of years but didn’t really have money to invest. Now that i have money to invest, I am investing in good companies in these sectors (aligned with my theme) when I these stocks are available at attractive prices.

That is why some of the stocks have even 0% allocation, I am tracking them but waiting for a good price point to enter.

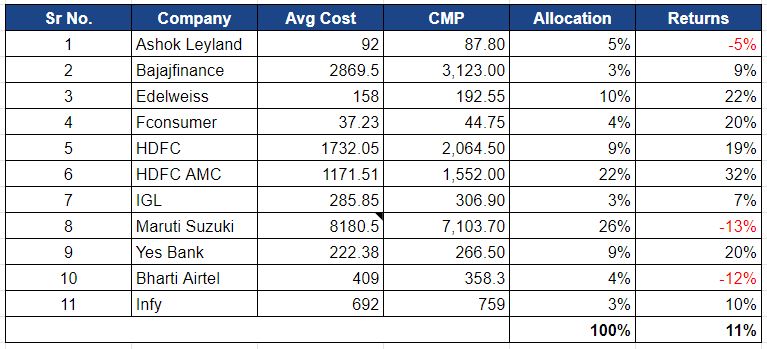

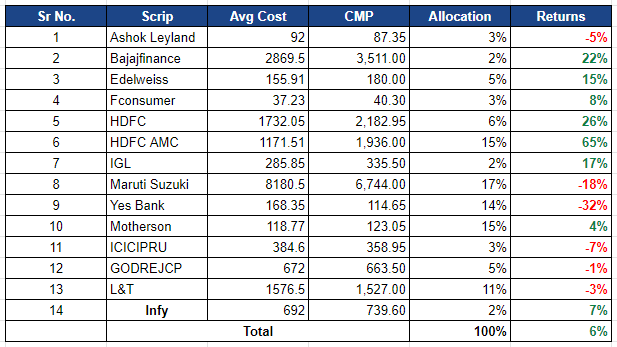

Added Motherson, GodrejCP, L&T and ICICI Prudential

Averaged Yes bank

Will average Ashok leyland near & below 80

Will average Maruti near & below 6400-6300

Might add ITC, Indusind, Indiabulls at lower levels

What happened to Britannia and HUL? Did you not find a good entry price?

As these are big FMCG companies, they always trade at premium, so why not create a position like you did with Bajaj Finance and IGL and average down when they fall?

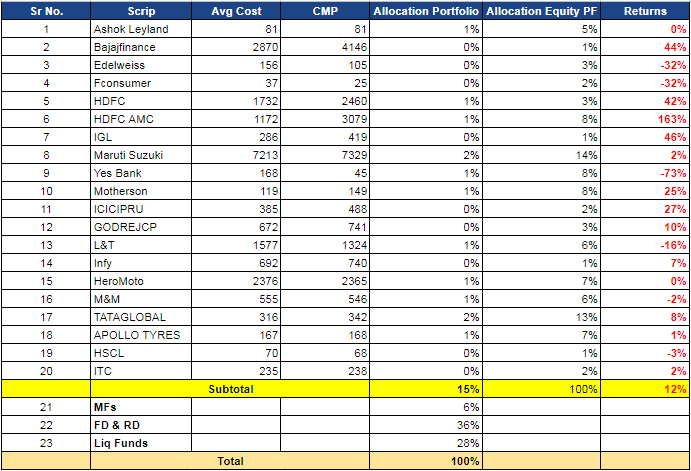

Currently holding 80% cash & 15% equities, 5% in DHFL NCDs

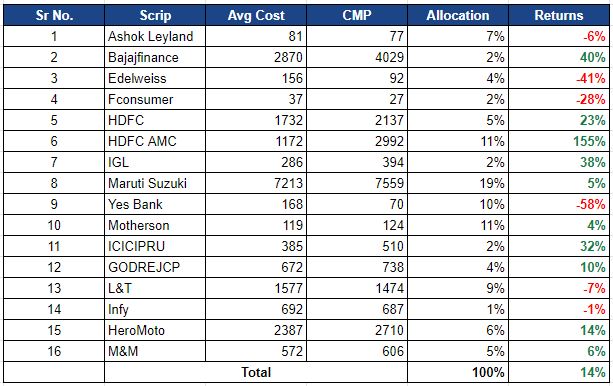

Will start SIP in auto - every 1.5% drop will add 10% of portfolio in M&M, Maruti, Hero, Motherson (I ‘believe’ downside for auto is now limited - 10-15% )

Axis and Indusind on radar

Will start Brittania near 2600

Adding Bajaj Finance if it goes below my cost price