Dear Rohit,

Can you please disclose the source of this info about increase in Promoter holding.

This will give a good clue about other industries also.

Regards,

Prasad.

Have done some work. Below are the positive, risks and a few questions-

Positives

- Increase in home textiles business. While the sales may not grow much going forward as more yarn is used internally, the margins will improve materially. The margins for yarn move between 12-18%, 22-24% for terry towel and 24-28% for bed linen. Given below is the EBITDA for the segment. Q317 was impacted by increasing cotton prices. The bed linen capacity has increased from 10% on q1 17 to 30% in q3 17. The company expects 40% utilization this year. Terry towel capacity utilizatoin is 50% post expansion in 2015 and is expected to increase to 65% by FY 18. At optimum utilization the company can do 5000 cr of revenue vs 3600 cr TTM which leaves them with some room to grow

-

Paper segment has witnessed increase in realizations as the share of copier branded segment has increased. They have the highest margins in the industry. The company seems to have increased prices despite reduction in raw material (wheat straw) prices. Most of the improvement in profitability has come from paper. The impact can be seen below –

-

The company has been pre paying its high cost debt and now 75% of the debt on the BS is under TUF. As on September 2016 the outstanding net debt was 2520 cr and the company is scheduled to pay 80-100 cr for the next 8 quarters. The net debt to equity has gone down from 3,1 in 2013 to 1.4 in December 2016

-

The company revisited its capex plans on power plant and yarn modernization which shows their intent on reducing debt and increasing ROCE

-

. The company has no capex plans as of now and will only spend maintenance capex of 50 cr going forward. The management expects to generate 400 cr of cash after meeting debt payments. The company has also started paying dividends.

Negatives

- High volatility in cotton and inability to pass on price increases to customers

- Management using warrants to increase equity stake in the past. However the management has assured of no dilution going forward.

- Two completely unrelated businesses housed under one entity. Demerger can unlock value.

- Promoter has political background.

Questions

-

Does being fully integrated help companies like Trident in reducing the impact of increasing cotton prices? A preliminary look at Indocount margins recently shows that the reduction in margins is higher vis a vis Trident due to increasing cotton candy prices

-

Can we track cotton candy prices from any source?

-

The company is currently doing 18% EBITDA margin in textile. This is at 40% bed linen and 50% capacity utilization. The company expects revenue of 5000cr at optimum utilization from both these segments. Then why is it that the management is guiding 18% EBITDA margin despite significant scope of improvement due to shift to high margin and operating leverage? The peers are doing far higher margins - even the ones who are fully integrated

All in all, this does not seem to be a bad bet. Assuming the company reaches its target of 5000cr and does 18% EBITDA in textiles and does 900 cr in paper with normalized margin of 30% - EBITDA in 2019 would be around 1200 cr. Using 8 ev/ebitda multiple and assuming a debt of 1500 cr by 2019 the equity valued comes out to be around 7800/7900 cr as compared to the current market cap of 4500 cr – an upside of approx. 70%. Normally I would look for higher upside bets but in this market with low valuation comfort in omost of the stocks, this doesn’t seem too bad.

Disc. Invested at 79

3 Likes

great job buddy !!.

One thing to note is that for last quarter their paper and chemical business almost touched 50% of total profits where as the total revenue generated from paper and chemical was not even 1/3rd or the total revenue.This speaks of the huge margin they are getting from paper and chemical(I calculate its around 28% compared to 9 to 10 % approx in textile business overall ). I would love to know what is cooking up in paper and chemical business.Hers is the break down -

total revenue textiles - 91552 (total profit - 8312)

total revenue paper n chem - 22334 (total profit - 6335)

total profit - 14600 approx.

All figures derived from balance sheet and figures are in lacs.

Someone needs to find out whats up with their paper and chemical business as we cannot ignore 50% profit generating business at all !!

Disc - invested at varous levels below 70.

removing this post as its marked as spam - not sure why :(. I think too much research is also harmful.

The topline in their paper business is not expected to increase given its operating at 92% utilization…their realizations have improved due to three reasons- a. They got into copier paper in 2016 which has higher margins and now accounts for more than 50% of the paper revenues and b. They have increased the prices continuously as it’s a branded product for them and c. The price of wheat straw which is their raw material has decreased. So a 5% decline in raw material prices and a 5% increase in prices has led to increased margins. I believe they have also benifited from the shutdown of ballarpur but not sure. One needs to assess the sustainability of these margins more than anything else. It’s a big positive that they have some pricing power in the paper segment. They can increase the volume by 15% by debottlenecking the plant for which they need to spend 100cr.

@sagararya some points i would like to share and ask -

- Can u share more info on “promoter has political background” ?

- Its surprising that even with 50% utilization in terry towel, they claim to be the largest producer of Terry towel in the world in their annual report.

- Are you aware if they have any RnD in place and whats the focus?

- Cotton prices are running high - https://in.investing.com/commodities/cotton - Do they hedge ?

As per their concall they can do with it for next 6 months but after that it will be reflected in the price.Also, can we use a cotton mill against the high prices of cotton as a cushion?

The cotton in India is plenty but we still are importing because quallity is low in india check this -

http://www.caionline.in/articles/india-there-s-cotton-aplenty-so-why-are-mills-importing-fibre.

5.Can you share some info on cash flow (not screener data) based on actual balance sheet. - They are worlds largest wheat straw based paper manufacturer which is a low cost process and hence high margin.I will share some more information on this - working on this.

7.Any details on how competitors are placed - I have some details to share on how much has welspun lost due to the fake egyptian cotton issue but not sure how much they gained out of it. - Overall - I think its such a smooth play against the welspun fiasco and ballarpur issue (2/3rd market share of total paper industry in india.)

- Any details on scuttlebutt ? I contacted few who interned at Trident and their initial reaction was that it a old style ‘Lala wali company’ in terms of execution but very loyal to customers… that alone cannot decide how it works - I am trying to get in touch with dealers and others to get an image.

- Last - can u share official info on capacity and utilization if you can.

Disc - Invested at various level below 70.

I have heard from a source that the guy has a lot of political connections and has used it to his advantage. Article below although old, mentions the same.

This is not based on the utilization, but is based on the actual capacity of 90000 MT per annum

The company does talk about some niche products but its all noise in my opinion. The fact is that there is little differentiation in terms of product offerings as compared to its peers. None of them have pricing power for the same reason

Yes they do get into forward contracts. They do not import raw materials as far as I know. India is the largest producer of cotton globally.

I know a lot of players have expanded capacity in the home textiles segment and many have forward integrated into it. Dont have numbers on capacity for each one of them. Will be interesting to find out more about this. Trident has the largest capacity in terry towel and hence one would back them to do well in this segment however they have just entered bed linen. Although they can cross sell products to its existing customers it will be important to monitor the progress of this segment going forward and if they can capture new customers.

Utilization - 30 % in bed linen ; 50% in terry towel ; 90% yarn and 90% paper

2 Likes

Here is a snapshot from Crisil report about capacities of various peers.

Full report is attached.

CRISIL Independent Equity Research Report.pdf (1.0 MB)

More reports are available here.

http://www.tridentindia.com/content/independent-equity-report.aspx

5 Likes

I think this report was published before Trump called off TPP agreement - its not a hugely positive but still since it has been called off, Vietnam is no more in the soft corner in terms of pricing and hence its a gain to India.Below is the report part related to TPP

“Although it is a threat in the long term, we do not see a significant impact on terry towel

and bed linen exports of India as the duty applicable on terry towel and bed linen imports in

the US from India is only 3.3% and 6.7%, respectively; much lower than the duties

applicable on apparel and fabric segments (~10%). Hence, the cost advantage to other

terry towel and bed linen exporting countries is lower than that to the apparel and fabric

exporting countries. Moreover, Vietnam, one of the key countries under the TPP

agreement, currently lacks capacity for terry towel and bed linen segments. Hence, we see

little near-term threat for the home textiles exports from India.”

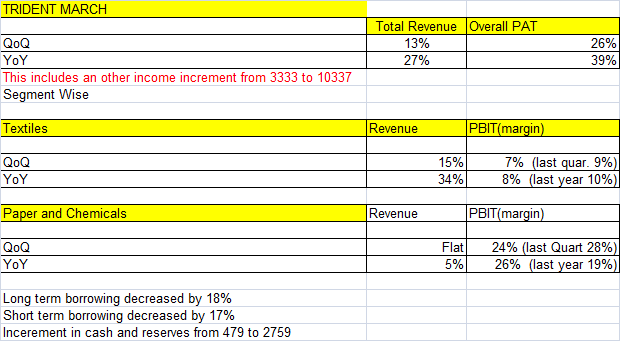

Guys anyone have analysed results?

A little disappointed with the results. Increase in profits is coming from other income which stands at 103 cr this year vs 33 cr last year. The operating margin of the textiles and the paper segment have reduced materially.- almost a 150 bps and 350 bps reduction QoQ respectively. I believe there is mean reversion happening in the paper segment and hence am not too surprised with the margins there. Was expecting better in the textiles segment.

Also the company has announced that it will raise 6000 million in the form of NCDs. Could this be for yarn modernization and power plant?

Well margin will increase as trident entered in high end branded segment in collaboration with Elle Decor so I don’t bother about it as of now…

its a 10 month old news i.e. July 2016. - also if you think so could you please provide breakup on how much will this impact margin and why ? Have they given any additional info on this.

Can there be any segment of forex hedges in the other income? As trident is a large exporter I think they do some hedges. If so, I think other income should at least partly be considered part of operating revenues no? Last year they had some USD 80-90mn worth of export hedges I think

That can be one reason we can think.Cotton prices are running high so hedging in commodity plus currency but to this extent - we can get clear picture only on tomorrows call - call details are below -

022 - 39381059 at 11:30 am.

Well it’s not only ella Decor…Check their old & new quarterly presentation and compare customer list, You will find new biggies as customer…

It’s just a hint…

1 Like

1 Like

My notes from the Q4’17 concal -

Other income component is higher due to the following reasons -

- Highest export in q4

- Change in accounting method, so forex gains are shown under other income. Earlier, they were under other operating income, so weren’t visible like now.

You are right about the lower margins for q4 (16%)…slide from 20%. Reasons were considerable inr appreciation, expensive cotton. Going forward, management has guided for 18-22% EBIDTA margins for next 2 years. Mgmt said cotton prices are going to moderate going forward due to higher acreage. Another point which will be aiding margins in 2018 is higher bed linen component in the overall mix… and better product mix within bed linen segment to value added products. Rebate of State Levies (ROSL) is also going to improve margins for exports division by 2 - 2.5% for home textile exporters). Another factor in margin improvement will be more captive yarn consumption. So overall, net effect on EBIDTA margins will be positive going forward.

Paper - He said there were fewer number of days in q4 (if you look sequentially), and plant was closed for maintenance for some time in q4, so effected paper segment. Going forward, paper production and utilization would improve sequentially.

Bed linen division should break even in q2’18. (at around 40% utilisation). Currently operating at ~29%.

In Q4, utilization per segment

Yarn - 96%

Bath - 54%

Paper - 88%

Bed - 29%

in 2018, target is to improve bath segment utilization by 55-60% and bed segment by 40-50%

4-5 month hedging policy. I think 40% is covered.

Net debt reduced from 3420 cr to 2714 cr by March '17. Of this, around 1500 cr is at 3%. Average interest rate is 4%, which will go down due to -

- Debt repayment (300-400 cr for this fiscal).

- Raising money through NCD/CP to retire higher cost debt earlier than scheduled. Approvals are in place.

No capex planned for next 2-3 years. Depends on utilization levels. Said, once they attain 70% utilization, they will think of any further capex. Regarding yarn segment, no capex planned (usual 50-100 cr will be spent this year to clear bottlenecks). Paper division, pondering upon 100-200 cr capex which will increase capacity by 15-20%. Nothing concrete yet.

Added one big customer. Impact would be visible from June.

Growth in US/Europe is around 3-4% pa.

Risks -

- Currency fluctuation (INR appreciation)

- Higher cotton prices (forms 50% of the costs)

Trying to mitigate the currency risks by hedging receivables. New contracts are negotiated based on current currency and cotton prices. Overall, in yarn there is a lag of 40-45 days to pass on the prices, and in bed/bath, 90-135 days. Being vertically integrated, they are able to moderate any drastic price impacts much better than other players.

What i like about Trident is that they are sort of walking the talk as far as improving the Balance Sheet is concerned. They are continuously adding new customers to fill in their capacity. Management is prudent enough to negotiate and fill the capacity by lowering margins upfront and then gradually work up the ladder on the margin front.

Indian textile industry is still much more competitive than Chinese and others due to various factors discussed already on the forum. I am hopeful of them maintaining 15-20% growth on this higher base for next few years. At 11.5 p/e trailing, with Free cash flows close to 750 cr per annum, they will be able to clear the debt as planned, which will result in better net margins. Some operational leverage will kick in as well with better bed linen capacity utilization and better product mix.

4 Likes