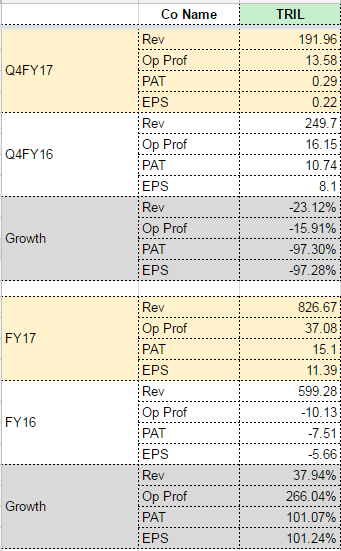

Another order win for TRIL.

TRIL has received order of Rs.153 Crores from Gujarat Energy Transmission Corporation Limited (GETCO). With this the current order book is now Rs 1020 crores.

Another JV. This time for manufacturing of transformer oil regeneration and purification plants

Still wondering whether this is a diworsification or not.

We need to ask this to the management some more details in the upcoming conf call(Q4 FY17) before we draw any conclusion.

No, there is good scope for transformer oil regeneration. The retained oil can be used both for internal company use., for maintenance of on-site transformers & can be sold to other users too.

It is a completely different business with different skillsets required, different raw materials, different suppliers etc. Both backward and forward integration needs to be thought through else it becomes a trap. Overly extending this analogy, every car manufacturer should then become a steel manufacturer, then iron ore miner etc.

Unless this is some very specialised transformer oil which is high margin, I would remain sceptical till I get a better understanding.

You got it completely wrong.

They are not getting into transformer oil production like Savita, Apar, etc.

That requires an altogether different set-up & a huge investment.

They have entered into an agreement with Mr. Gopal Sanasy., for “Manufacturing & supply of Transformer Oil Regeneration & Purification plants”. So, this means, that they will be manufacturing & selling machines, which will do the transformer oil regeneration, to the people who are providing on-site transformer maintenance.

This wont be too much of a burden., as no significant investment is required for the same.

Only thing required, is that the set-up should be such to facilitate easy assembly of bought-out components to build a final product.

Q4FY17 Results and Concal Updates

Q4 FY17 Concall Notes

• 5956 MVA of transformers produced in Q4FY17 vs 6615 MVA in Q4FY16.

• 962 cr order book as on 31-April-2017

• 12.55 cr of provisioning for delayed payment and liquidated damages taken in Q4

• New order received from one the largest utilities in Australia. Initial order was for solar plant transformer, then follow-on order for larger power transformer. Expecting good orders from this company in the future.

• JV for old transformer servicing done with Mr. Gopal Sanasy. He is an expert in servicing old transformers on site. TRIL has no presence in the servicing space, and this will be an initial footprint in that area.

• Co expects margins to be in 10-12% for next 3-5 years

• Debtor days - 144 days

• Overall capacity - 32,000 MVA

• Current total debt is approx 180 cr

• About 20% of receivables would be more than 6 months

Few additional points:

- Australian business will come at 20% ebidta margins - most of the local australian companies are working with 30% ebidta

- Jinke JV - overall GIS substations upto 220Kv market is 300cr market but growing fast (does not seem a big market)

- dominated by ABB Alstom seiemns - total 6-7 players - with current capacity - sales can go upto 1200cr (current sales 802cr)

- negotiating with banks for lower interest costs. It has started reflecting in q4 results

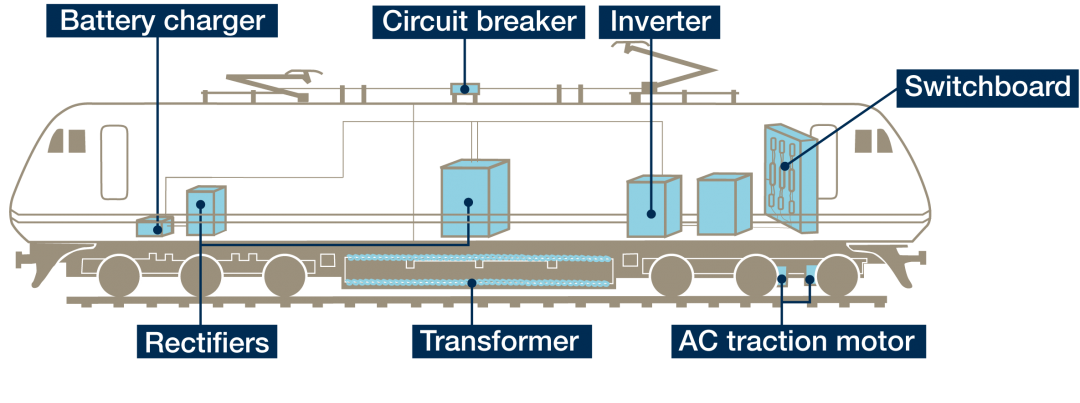

- started doing business with railways. Got approved by RDSO - transformer for locomotive ( I was not clear what the product here is)

- trying to get through a arc furnace transformer deal in indian market - if this deal goes through can open the market ( Arc furnace transfomer is used in steel industry)

- FY18 guidance- 10-15% growth in topline and minimum 10% ebidta margins

company has done only Rs.820crs of topline in Fy17 aginst guidance of Rs.1000crs. Again shortfall.

Prashant

I don’t remember they ever guided for 1000Cr in FY17. Their guidance was around 850Cr. Capital goods can always have some variation. One delayed shipment can cause such fluctuation.

Anyway the trajectory looks good.

Getting RDSO Approval opens up new opportunity for TRIL & will surely contribute in addition to sales.

But the RDSO approval is a product approval., this means., the approved transformer can only be used for its specific application (i.e. building of locomotives) & not elsewhere.

Disc : not invested.

Jitendra Mamtora on CNBC -

Lots of good data points on the transformer industry and TRIL. Seems like FY18 would be the key year to watch out.

TRIL board today approved a QIP of 250cr and a stock split from Rs 10 to Rs 1 face value.

Hello Abhishek,

Would like to know your thoughts on these two points.

- Considering the money from QIP is for large transformer and Arc Furnace transformers, is that something company will be manufacturing in their existing plant? Any idea how quickly this additional capex raised can be put into use?

- Splitting a Sub-400rs. stock into 10 seems more like to add to speculation and increase price volatility. I do not understand the benefit here much.

Disclosure: Invested and positively biased.

For point 1, we need to wait for clarification on concall. For point 2, my personal take is its a bit silly to subdivide a 350 rs stock. At best a 1:2 would have been okay if they really wanted to do anything. Or give a 1:1 bonus.

In an interview to CNBC they said it’s just an enabling resolution.