Joint Venture agreement with Jingke Chinese company.Its Logical foray for diversification in T&D segment.

TRIL has come out with excellent set of numbers in expected lines. The balance sheet is also become more robust. Interesting to see QoQ consistent improvement in Industrial Segment sales and now it is 76% compared to year back coupled with revenue growth.

With the Chinese JV they are following approach of companies like ISGEC by offering the infrastructure and manufacturing facility and then gradually trying to get a hang of the technological intricacies. Gas Insulation Substation is an interesting area though margin would depend on the kind of agreement they have with the Chinese partner.

Only overhang with the company is the proposed QIP issue. else, the company seems to be on a right path.

Attached the presentation and quarterly report.

Presentation of company : http://corporates.bseindia.com/xml-data/corpfiling/AttachLive/B91D9201_88FB_4E37_81BA_9FFFEBE5D506_134418.pdf

Disc.: Author is SEBI Registered Investment Adviser. This is not a buy or sell or hold recommendation but solely for purpose of discussion and review. I am invested in the stock. No trading in last 30 days. The stock has been recommended at lower level to paid members of our advisory service https://aveksatequity.com. Recommendation was given in Oct 2016.

5 Likes

This is due to the third party export order which is in full swing. Post that the industrial segment will fall. But a very good set of numbers.

3 Likes

Transformer and Rectifier (India) Ltd_Steller Performance_Q2FY17 Result Update_BUY (2).pdf (547.5 KB)

1 Like

I was looking at Voltamp Transformers and its valuation looked more attractive than TRIL. Voltamp is trading at 15 pe , no debt and a healthy 1.75% dividend yield compared to TRIL’s 25 pe, 0.49 d/e and no dividend for last 2 years. I am sure these are not the only parameters to look at.

- 2 cents from a novice investor.

1 Like

Voltamp can put up capacity without any pressure on BS or dilution while TRIL need to dilute.TRIL also need to have decent order book to service the debt which is a risk in my opinion.

Disc: Invested in TRIL and gradually adding Voltamp as well.

One important distinction is that TRIL has capabilities in the higher voltage power transformers. The engineering and manufacturing complexity is more the higher up the KV range one moves.

2 Likes

There are three important things here:

a) Capacity: Setting up capacity normally takes 2 years.

b) The technology.

Voltamp: The thing that Voltamp specializes in is ‘Dry Transformers’. The company has a 60%+ market share in this segment. This segment is mainly dependent on industrial revival and is not so much used for SEB distribution purpose so I do not see so much impact because of govt. schemes like UDAY or Deen Dayal Upadhyay scheme. As far as distribution transformers under 220 KV is concerned this technology is as good as commodity.

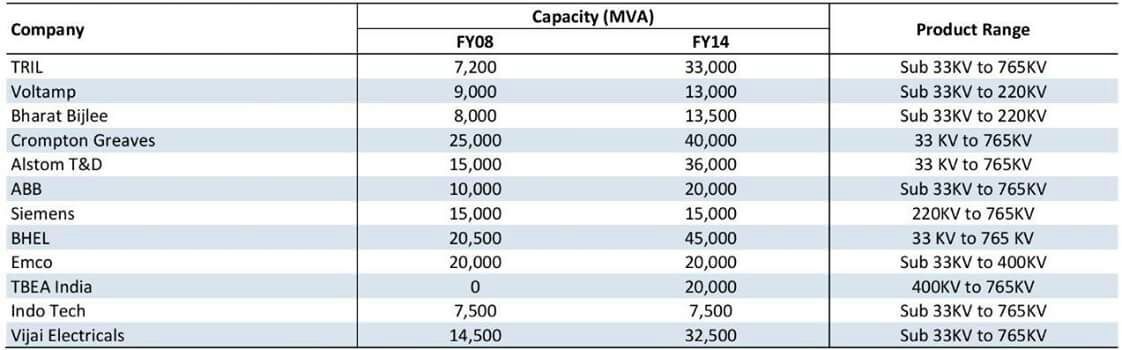

TRI: On the other hand TRIL has continuously expended its technology capabilities from being sub 220 KV to 765 KV. Further TRIL has expanded into full 765 KV range of reactors and has supplied them to PGCIL. The technological prowess of TRIL can be accessed from their capability to design 1200 KV for Bina UMPP. TRIL has further expanded into complete range of Arc Furnace Transformer which is a 20%+ EBITDA margin business and is currently dominated by 3 to 4 European players. The Arc furnace transformer business is $ 250 Mn a year and the company plans to break in top 3 in next few years. They have a huge cost arbitrage here. Also TRIL has recently tied up with a Chinese company and entered into a completely new but related area of GIS switchgear below 200 KV. The best way to look at TRIL is their partnerships with various international companies like ZTR Ukraine (765 KV Transformer), FUJI Japan (765 KV reactor) and very recently with Jingke China (GIS switchgear).

There is very little to compare between the two, they are just doing different things. The last few years have also shown the different mindsets of the promoters of both these companies. Voltamp has been sitting on tonnes of cash and using it for Working Capital needs and elsewhere, playing it safe whereas TRIL has continuously expanded on capacity and technology at the risk of its balance sheet.

I am not saying that Voltamp will not do good but I would rather go with a promoter who has risked to grow and ventured into newer things rather than the one who played it completely safe.

14 Likes

@basumallick

Yes it seems so as of now. but I won’t take it as a huge lead (may be wrong in my assumption).

Let me add a disclaimer first that I have no experience of Transformer design. But most of the times these claim of technical design capabilities are hugely exaggerated. You have a tie up with a big MNC who has given you all specifications and you just go ahead and scale up/down based on need and call it R&D. This activity need some skill not a big R&D capability.

Having worked in mechanical design for 10 years before moving to IT, I have seen how the basic engineering drawing references are converted into new products. Had the privilege of being part of first rocket launching pad for ISRO and first 6-Hi indigenous rolling Mill.

Anyway let’s see how things progress.

Disc: Invested in TRIL…and started with voltamp

1 Like

Thanks Anant for details. I have only one three issues with TRIL

- Too many TV interviews these days…

- Upcoming dilution through QIP

- Stretched BS as they probably need 600Cr+ sales to just service the debt.

Anyway the order flow is strong and till they are coming all the above can be neglected.

Voltamp will certainly take time as UDAY impact is still away.

1 Like

Generally I too do not like too much presence on business channels. Having spoken to the promoters over conf calls and in person during AGM twice I do not see much concern here. Mr. Mamtora is a technocrat and a very good person. During my conversation he regretted raising capital at higher valuation (he diluted around 3% later in favor of minority shareholders when the 75% SEBI regulation came). Both his son and the Sr. Mamtora actually took a salary cut last year (after increasing it) after realizing that the business is not doing well. I asked the salary question in one of the conf calls and he apologized for it.

I think the dilution should be to expand capacities for distribution transformers because of the upcoming UDAY opportunity. Also until now it is more of an enabling resolution. I would like to look at the actual amount of dilution (ofcourse the approval is for 125 cr) and take a call.

The best returns in turnarounds/cycles are made in companies with a little stretched balance sheet. The balance sheet should be stretched enough to survive through the downturn but not more. At the same time I agree with you that a year or two more in recovery could have been very dangerous, but you wait for definite signs before moving in.

6 Likes

Thanks Anant for all clarification. You have done extensive work so your confidence will be much higher than mine.

But still I will keep watching the order book levels very carefully.

Regards,

Raj

The company has been awarded the order for 40 No. of 15MVA and 40 No. of 20MVA Power Transformers with Natural/synthetic Ester Oil of 66 kV Class amounting to Rs. 92 Crores from Gujarat Energy Transmission Corporation

Limited (GETCO).

With this order, the Company’s Order book as on date stands around Rs. 960 Crores.

Hi,

Please have a look at the cash flows which has deteriorated significantly over the years. On the other hand competitor voltamp has managed its balance sheet very well with practically nondebt

2 Likes

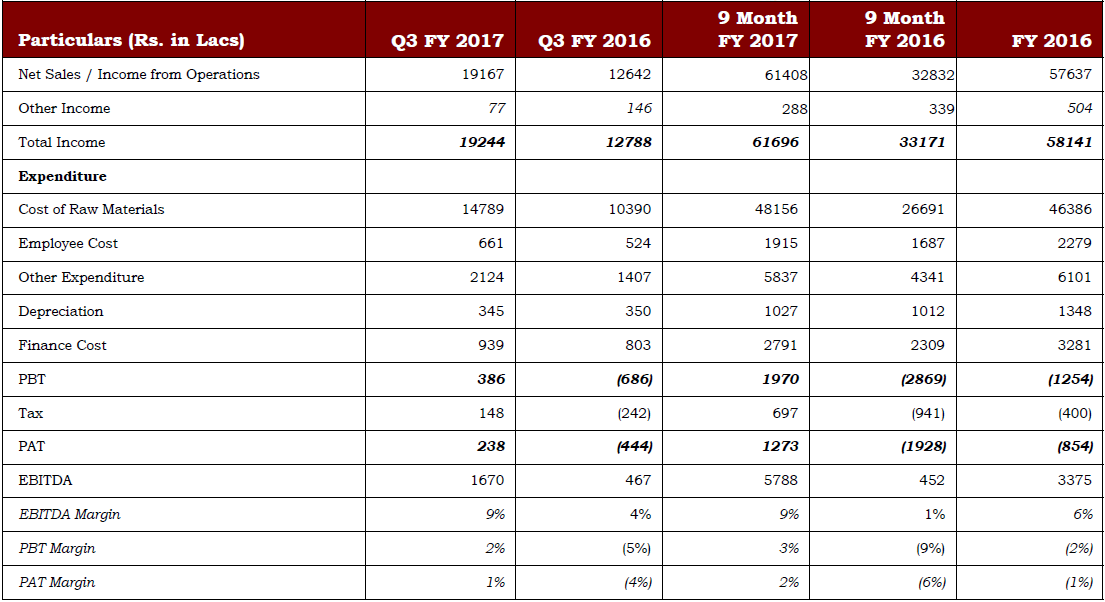

Q3 FY17 Concall Notes

• Last quarter may be better than Q3 but not as good as Q4 historically.

• Target is 800-850 cr revenue for Fy17

• Expectation of 1000cr of revenue for FY18

• Expected EBIDTA is close to 10% for FY17. FY18 expected EBIDTA is to be better (~12%)

• Strong order book in the 400KV / 765KV Transformer

• The Chinese JV will start contributing to revenues from FY18

• There is an expectation of strong order inflow from the SEBs

• The margin profile is increasing; current margin for unfinished orders is around 10-12%

• The debtor days are around 140

• Current capacity utilization is around 80%. Current capcity can support around 1200 cr of revenue. However, company is going to expand capacities in some areas

• Co has done around 100cr from the renewables space and is expecting around 20-25% growth from this segment next year

• Total debt on the books is around 300cr

8 Likes

Small correction @basumallick … Total debt on books is about Rs. 200 Cr… Rs. 300 Cr is total funded + non funded liability

7 Likes