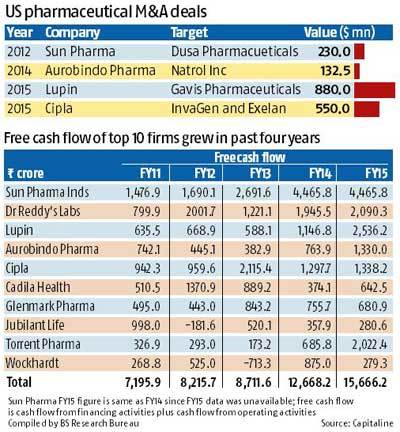

First off, huge thanks to @sharemarketgen_ for an engaging offline discussion on Torrent.

While reading through various FDA presentations, a picture of positive tailwinds was forming in my mind and it made me to have a relook at Torrent.

Future focus on the below 2 areas.

Complex generics

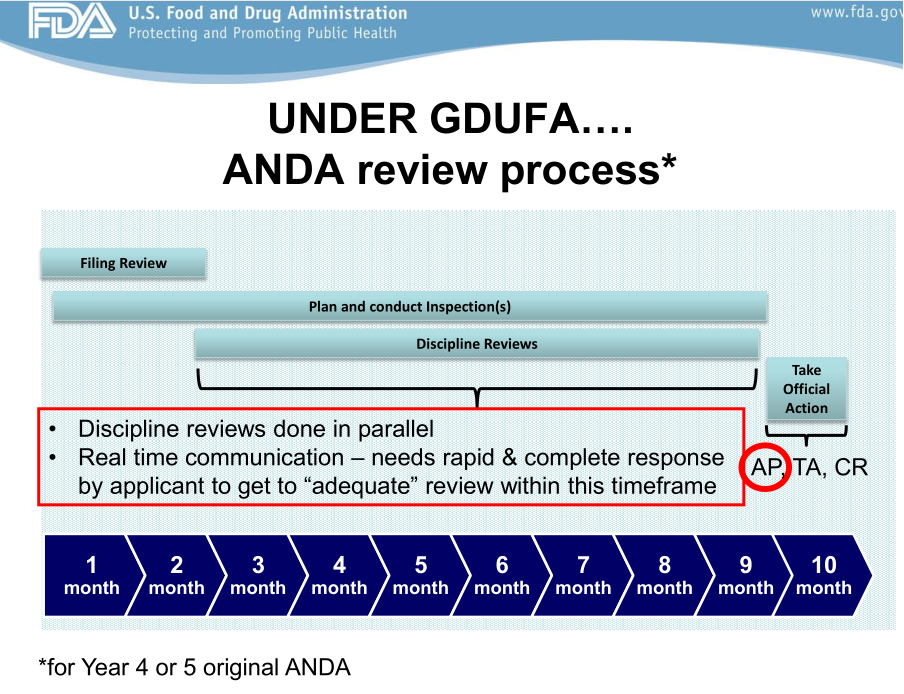

ANDA filings accelerated from Q1 2016-17

Big ramp–up in ANDA Approval timelines from 3 yrs (Y1-Y3) to proposed 10 months (Y4 and Y5) based on latest GDUFA updates from OGD, means the lack of ANDA submissions in FY15 and FY16 is not big impact.

This is backed by the pace in progress of the CDER Platform which has become single point of source for information compared to earlier disjointed systems/architecture. (Will post detailed info on Ananth’s thread in the weekend)

Early signs are positive, but proof is in eating of the pudding!

----------

GDUFA is continuing to spend efforts and providing grants for research on finding methods to determine and define product equivalence of Complex Generics.

GDUFA Regulatory Science 2015 - Robert Lionberger, FDA

http://www.fda.gov/downloads/ForIndustry/UserFees/GenericDrugUserFees/UCM434325.pdf

Highlights of Work in Progress

• Complex Active Ingredients

– LMWH, peptides, complex mixtures, natural source products

– Multivariate data analysis for complex mixtures in collaboration with FDA labs

• Advancing In Vitro Equivalence Methods for Complex Formulations

– 7 grants on semi-solids for topical or ocular delivery

– 6 grants on liposomes/sustained release implants

• Complex Drug-Device Combinations – DPI, MDI, nasal spray, transdermal system

– Adhesion for transdermal systems

Results

• Draft Guidance on Conjugated Estrogens (CE) Tablets (Dec 2014)

• Outlines detailed recommendations on how to establish the pharmaceutical equivalence of the drug substance and the bioequivalence of a proposed generic CE product. This guidance is the product of many years of collaborative work across CDER.

• Other Complex Product Guidance

– Liposomal Injections: Verteporfin and Daunorubicin Citrate

– Sublingual Film: Buprenorphine hydrochloride; Naloxone hydrochloride

– Transdermal ER films: Buprenorphine and Estradiol

– IUD: Levonorgestrel

– Subq injection: Lanreotide acetate (nanomaterial injection)

– Sevelamer Carbonate: Recommended characterization

http://www.fda.gov/ForIndustry/UserFees/GenericDrugUserFees/ucm370952.htm

Recommend to review through the meeting presentations of the Fall Meetings for the next-gen research on Pharma.

Found papers such as “Nano-similars” and “Generics for Oral Inhaled Drugs: Knowledge Gaps for streamlining Bioequivalence approval?”

At the most simplistic level, somebody needs to replace DRL and Torrent looks a strong bet.

Disc: Sold of my low conviction/allocation pick in Rain Industries to buy Torrent last week.

i am sure that a quick validation check is done with the management but any management tends to be positive, so far out into the future

i am sure that a quick validation check is done with the management but any management tends to be positive, so far out into the future