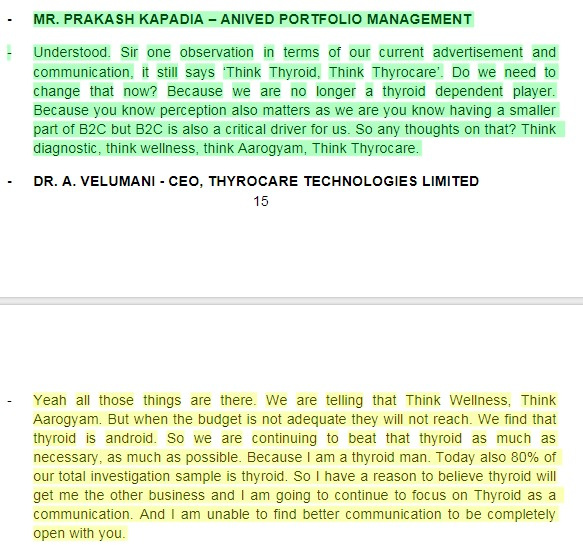

@dprashant Here is what Dr Velumani replied when was asked a question on similar lines in Q4 concall. I don’t go by his logic, though as even i think they should have something more general. But his argument, they don’t have that sort of budgets to connect/reach the audience with a changed headline.

7 Likes

Wonderful presentation Vivek. Nicely covered.

The only point I like to highlight is, no doubt being low cost is great model. But in some industries where if you cannot bring the scale quickly and gain control on supply side or have a model to reach acquire new customers quickly, you will be constantly forced to fight with new entries.

Also low cost works in commodity kind of business such as transportation, retail, logistics.

Ex, Ola/Uber created new supply, squeezed out supply from other players and built a very powerful model to acquire new customers

Walmart created new low cost suppliers from China, built a better supply chain management with good logistics to become lowest cost retailer

Amazon again, very powerful model to acquire new customers, better vendors

Thyrocare we have to see, where do they have clear advantage in being low cost and because of which newer players will find very tough to compete if they want to do similar to Thyrocare

@Mridul, Thank you , not sure why he is so much focused on present revenues coming in from thyroid segment instead of what might be required in term of Ad/Tag line for expansion of business with diversified tests etc. anyway lets wait and see.

Hi,

I was just checking Screener…Noted Dividend Payout ratio for the Dr Lal is ranging 15 to 21% year for last 4 years where as for Thyrocare it shows 50 to 150%…

Can someone is this right??? Iy yes how these guys able maintain such a high payout ratio and stillhas low multiples vis vis Lal

Thanks

Yes- this is more or less right. Dr. Lal pays a smaller dividend and has retained cash on its books (about 550 Crs) which it has said it would use for acquisitions. Thyrocare on the other hand pays big dividends. Its core bio chemistry diagnostics business has a ROIC of 50-80%. Some of the cash has been utilized in its imaging subsidiary and the rest it has been paying dividends. It is also planning on a buyback. See the link below.

1 Like

Kindly go through this interview of Promoter in response to Bloomberg coverage of comparing thyrocare with Dr Lal Path Labs.

Have not expected this much anger from promoter and even felt like I am watching some politician replying to zee tv media guy though that is my personal opinion. he gave 5 year CAGR target of 20-22%.

Was tracking the company after excellent presentation from @vivek_mashrani not invested.

4 Likes

From the video, it seems that the business is a tough one and competition is eating out the revenues.

Disc - not invested and not willing to invest at these prices.

1 Like

Dr Velumani should not be worried about the opinion of analysts. He should just keep focusing on his business and market will decide the share price. Thyrocare is the lowest cost operator in this area with a very long runway.

Disc - invested from IPO and still accumulating. 15% of my portfolio

Hi all,

Researchbytes has earnings con-call pdf transcript for only last 2 meetings. I am looking for transcript for all con-calls.

Will apreciate if anyone can point me to pdf transcripts, if they were made. I would rather read than listen to an hour long calls.

Thanks,

Amit

I have links to the latest 4.

4 Likes

Q&A

60% of Cash will be Used in Thyrocare

Buyback, 40% in Capex for New Businesses:

A Velumani

Since the stock has been down for almost six months and is almost 20% lower than its peak rate, we felt it

is the right time for a buyback, A Velumani, chairman and managing director & chief executive officer,

Thyrocare, tells ET Now. Edited excerpts:

What prompted the company to come out with a open offer? Is this an indication that you feel the

stock is underpriced and you need to use the cash?

There are three things about this buyback. Number one is dividend. Roughly around 30% of cost is in

getting the dividend into pocket. So, that is a costly route to take the profits out. Number two, the stock has

sold at the lowest price for the last three months. So, we felt that it is right time for us to buy back. The

third thing is there is no better avenue of utilising this money. So, we felt that buying back is better option

and we have gone ahead with it.

Your promoters would also be participating in this tender offer/buyback?

No, promoters are not permitted because in the buyback there are two routes. The route which we have

adopted is company can buy only from the third parties and not from the promoters. The promoters do not

want to sell either.

I know your existing business model does not need cash. You have done your capex. It is all about

gaining market share and increasing a distribution reach. But you have also expanded outside your

core business which is essentially in the diagnostic space. You have moved into speciality healthcare.

Those businesses will require a lot of upfront payment. So, when you say you do not need cash, are

you accounting for the cash requirement of other businesses also?

The balance sheet is throwing out around 100

crore per annum. We might need a maximum of 25-30

crore into the capex intensive business and we do not want to put all money there. We have decided either

to declare a dividend or to put it in the capex. Since there are costs involved, around 60% of the cash is

used in buyback and the remaining 40% is put into capex in the nuclear business.

Will this be a regular thing? Are we going to see a buyback announcement at intervals of almost a

year from you?

It is difficult to predict but this time we felt we will buyback and the next time, if we do not need more

funds for the nuclear business, we will be buying back. But we do not want to commit to that right now.

You do not want to commit on that but you pretty much have that as part of your plan

1 Like

When you can earn very high ROC by deploying CASH into the business , Why management decided to buyback at very high valuations ? Dalal street pressure or what ?

When today all PE fund pouring out Cash into Diagnostic space, its sad to see an public company due to pressure from analysts doing what is good for short term.

Disc - Waiting for stock to come in F&O

Buy back is the best thing to do at this stage and that too on-market buy-back. Reduces the number of shares outstanding and increases the EPS per share. Promoters are not participating, their stake will go up.

Owners don’t want to sell and they are prepared to give market price to sellers to increase their stake indirectly - what does it signal to you? They are thinking long term…

Discl - hold a decent chunk, accumulating…

1 Like

Also annual (growth) capex requirements are only Rs 30 crores according to Dr Velumani. Profit is 90-100 crores! Such a wonderful business, hence the premium valuation. Thyrocare is churning out cash well in excess of growth capex requirements - in such a scenario only 2 things are really worth doing, dividends or buy back shares… For dividends tax will have to be paid, buy back no tax issues…

1 Like

Members need to look at broader picture. There ate only two diagnostic players. With rising disposable income people tend to incline towards branded players. Hospitals in order to save costs and accuracy will opt for branded players. Eg. Alchemist Hospital in Panchkula has started using Dr Lal Path Labs. After A point accuracy and speed become more important

2 Likes

We can expect listing of SRL diagnostics 56% owned by Fortis healthcare soon.

SRL has crossed 1000 cr reveues and with the ongoing settlement of Fortis healthcare we can expect that soon the new promotors of Fortis healthcare will list it so that PE players owning 30 off percent can get decent exit.

That may help rerating of industry players .

On other side govt is working on price cap of few diagnostics tests that may further help organized players as it will become unviable for unorganized players if price caps are applied by govt ( assuming govt will apply aggressive caps on prices of few common tests ).

Will be interesting to see how things shapes up in next few quarters.

This is one sector where I personally believe that competition will only help more to industy in it’s transition from unorganized to organized.

2 Likes

Not applicable to Thyrocare in any way. Thyrocare is not into pathology (tissue specimens for cancer/other disorder diagnoses)…

1 Like

Nothing related to numbers , just a bit of scuttlebutt

Had to do some diagnostic tests . Called up apollo customer care on Saturday for a appointment on Monday , confirmed that they would call back . Nothing happened till sunday evening 3 PM . Decided to call the hospital directly got transferred to 2-3 departments and finally got the list of tests and charges. The tests asked for came to almost 10K .

Decided to try thyrocare , downloaded app , gave a call to custome care(sunday 5.30PM) as i did not see few tests, the guy said he would check and call back , received the call in 15 min with the details and the technician was there right at my door step this morning at 6.30 AM for sample collection.

checked with him how many people are there , how many samples do they collect,

he said 2 years back there were 37 technician (his ID no) and now there are close 110-120 .

Before they sued to collect 3-4 samples a day , today they collect 6-7 samples . Weekend there are more collection . This is only the individual sample collection from residences apart from what they collect from most small centers.

All these are only for Bangalore city alone and yes on the cost , it came to 6K.

Oh yes and apollo did call me just now after 48 hours for booking an appointment  . If Thyrocare can maintain the same level of customer service and scale well across , there could be a huge oppty .

. If Thyrocare can maintain the same level of customer service and scale well across , there could be a huge oppty .

16 Likes

I recently had a totally different experience with the Thyrocare. A few months back I had used their service and was shocked when there own collection boy asked me to cancel the online appointment and go through him instead. He also showed me many reports of clients who were using his services. I had brought this to Dr.Velumani’s notice and he had assured me that he would be looking in to my concerns (please refer to the my earlier post in this thread). I had started using Lal Path Lab, which is more expensive than Thyrocare, but has its own labs even in smaller cities.

Dr.Velumani then took time to inform me that whatever issues I had, have been looked in to and their system has been strengthened. He also told me that I could check this next time when I use their services. I must say that I was very impressed with this. So, recently when I had to get my tests (a ritual I do periodically) I thought of giving Thyrocare another chance. So I booked Aarogyam 8 for myself which covers 100 Tests for Rs.3200. The scheduled timing was 6.30 to 7.30 on 14th Sep. No one came at the scheduled time nor did I receive any communication, so I rang up the collection boy’s number (given in the confirmation message). The call was not answered despite repeated attempts, so I contacted Customer Care. The gentleman told me that he would check and get back why this has happened. Soon I got a call from a different number and the person introduced me as the franchise owner (I don’t really know what does that mean). After taking my details, this person arrived to my residence. It was the same man about whom I had complained to Dr.Velumani. His very presence made me uncomfortable, but I got through the collection of blood samples. The man even left the syringe behind that I had to dispose off. I was told that I would be getting the soft copy of the report latest by Sunday, the 16th. I fixed my appointment with my doctor accordingly for the 17th (today).

The report did not arrive, so I contacted the customer care. The lady sent me the report right away in my mail. But going through the report I found that the report was missing many important tests.So, I called upon the customer care again. This time a different lady replied the call and told me that these tests have been cancelled because of the technical reasons and I’d have to give the blood sample again.

My knowledge about the testing procedure is limited, but in the meanwhile I had found that the date of collection of sample was shown as 15th Sep instead of 14th. It might have been the case that the blood samples were not sent to Mumbai on time and hence were left unusable. The lady did not have any answer to my specific queries nor could she put me on line with someone who could answer them.

I am not complaining about the cancellation of tests. These things can and do happen. But the least they could have done was to inform me about the same. It was not until I approached them (one day after the reports should have reached me) I came to know of this.

It’s not the delay, but the lackadaisical way in which they dealt with their client -taking him for granted- that has pissed me off. The whole experience has left me wondering about their work ethics and how reliable are their test reports.

11 Likes