There is no cash consideration as per the scheme, i.e. receipt of Quess shares in lieu of the HR undertaking. This is important from a tax perspective for the tax man.

But when you are issued Quess shares in the above ratio, and let us say you have 1000 shares of TCIL, you will be entitles to 188.9 shares, but the smallest denomination of a share is 1. So 0.9 shares cant be issued. Typically in such cases, the value of 0.9 shares is converted into cash and given. Or some such scheme may be adopted (I haven’t seen any so far, my swaps have all been cash for such fractions) So there is cash consideration only to the extent of the fraction, and that is necessitated not out of the scheme but out of practical consideration of non issuance of fractional shares.

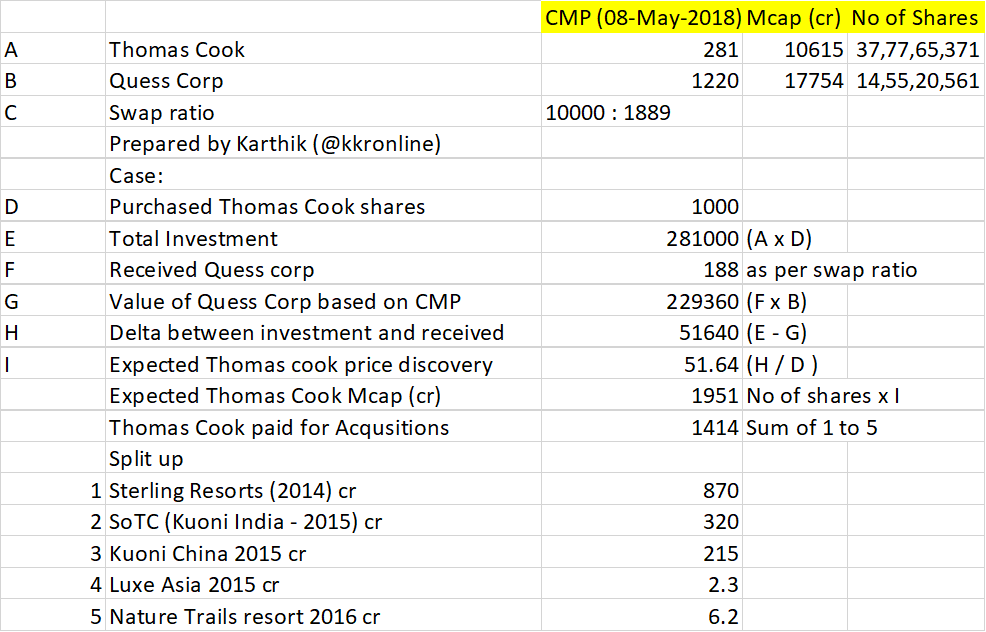

Back of envelope calculations suggest that TCIL after Quess is removed will have a MCAP of roughly 3500 cr with EBIT (excl. Sterling which is being turned around) of about 220 Cr. ROE should be substantially higher if one goes by segmental results of financial services and travel services. Looks interesting as you no longer need to worry about a holding company discount.

Prem Watsa in his shareholder letter after Thomas Cook acquisition a few years back had mentioned that the company has quite a bit of real estate also which will be monetised. Even in their press release they have mentioned about real estate:

“Move aimed at consolidating ownership of Group’s travel businesses, brands and

other assets including real estate”

So that is in addition to what you have mentioned…situation is quite interesting as the fall in implied value of thomas cook is faster than rise in value of quess as swap ratio is fixed. A rally in quess by 16-20% has nearly halved the implied value of thomas cook. with 200 cr plus ebit thomas cook can become very interesting provided quess doesn’t fall. The leverage works in the opposite direction also as a fall in quess price can lead to a much higher implied value of thomas cook making it unattractive.

Thomas cook is expanding thematic resorts via Sterling. If you refer Hotel experts interview shared before, Millennial interested to adventure, wildlife and nature based resorts.

“Holidaying these days is not confined to accommodation and food. People are looking for experiences and discoveries. We have created opportunities for people to explore their areas of interests and make holidaying more enjoyable,” he said.

“We are introducing tourists to local tribes, traditions, cuisines, hand-loom and handicrafts. If there are people who can create experiences, we would love to use their services. Tie-ups with local groups will not only promote destinations, but boost the local economy,” he said.

PS: Quess corp is on the rise and TC is focusing on the rest of the business is good the swap ratio shared by TC mgmt

The recent restructuring announced is trying to simplify its structure. Should give more clarity in the near future with @Marathondreams posted standalone results.

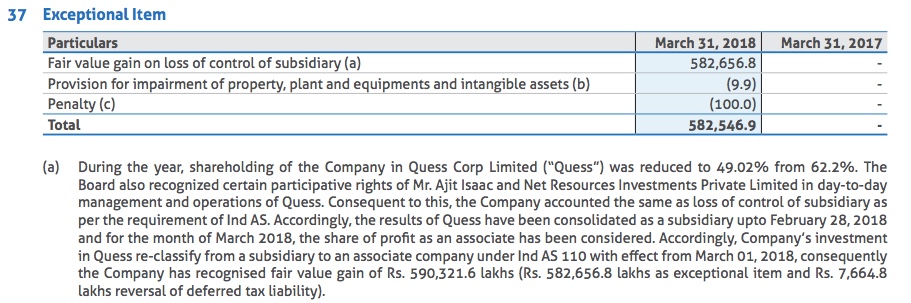

I was looking into the P&L of ThomasCook India and was not able to make out the PBT: the PBT for last year has increased from 248 to 5999 crores, is this because it was able to sell the Quess Corp? Does that mean that the company is having lot of reserves? Other income has increased.

The company has recognized the fair value gain of Rs 5903 crores in lieu of Quess Corp becoming an associate company and in accordance of Ind AS 110. More details can be read in the schedules in the AR of 2018.

Did the share holders of ThomasCook receive Quess shares? I read that Thomas Cook shareholders will receive 1,889 equity shares of Quess for every 10,000 equity shares of Thomas Cook. Is this already done?

What happened to the minority share holders who had less than 10,000 shares of ThomasCook, for eg: a share holder who had 100 shares of ThomasCook?

This is yet to happen, As per corporate presentation of TCIL of 8th August 2018, the corporate restructuring will take place in roughly 9 months ( so by Apr-May 2019) and the shareholders will get Quess shares by Apr-May 2019.