Phthalic Anhydride consumption in India is dominated by the Plasticizers sector. In 2017, plasticizers accounted for a share of 74.3% due to growing demand for polyvinyl chloride, PVC, in the construction industry and automotive industries, according to GlobalData, a leading data and analytics company.

The company’s report: ‘Phthalic Anhydride Industry Outlook in India to 2022 – Market Size, Company Share, Price Trends, Capacity Forecasts of All Active and Planned Plants’ reveals that Lurgi-BASF PA Technology is the dominant technology used for Phthalic Anhydride production and it accounted for 88.5% of the total installed Phthalic Anhydride capacity of 0.344 million tonnes per annum, mtpa, in the country.

Dayanand Kharade, Petrochemicals Analyst at GlobalData, explained: “Plasticizers contribute largely as end use application of Phthalic Anhydride in India due to growth of the construction and packaging industry. Phthalic Anhydride is also extensively used in the production of phthalate plasticizers for making PVC to a large extent in the automotive and electrical & electronics industries.”

The largest Phthalic Anhydride plants in India in 2017 were ‘IG Petrochemicals Taloja Phthalic Anhydride Plant’, ‘Thirumalai Chemicals Ranipet Phthalic Anhydride Plant’, ‘Asian Paints Ankleshwar Phthalic Anhydride Plant’ and ‘SI Group India Navi Mumbai Phthalic Anhydride Plant’.

The major companies in the country are Asian Paints Ltd, I G Petrochemicals Ltd, PPG Industries Inc, SI Group-India Ltd and Thirumalai Chemicals Limited. In 2017, together these companies accounted for 100% of the Phthalic Anhydride capacity in India.

The main sectors that consume Phthalic Anhydride in India are Plasticizers, Alkyd Resins and Unsaturated Polyester Resins, UPR. In 2017, these sectors accounted for almost 96.3% of the Phthalic Anhydride demand in the country.

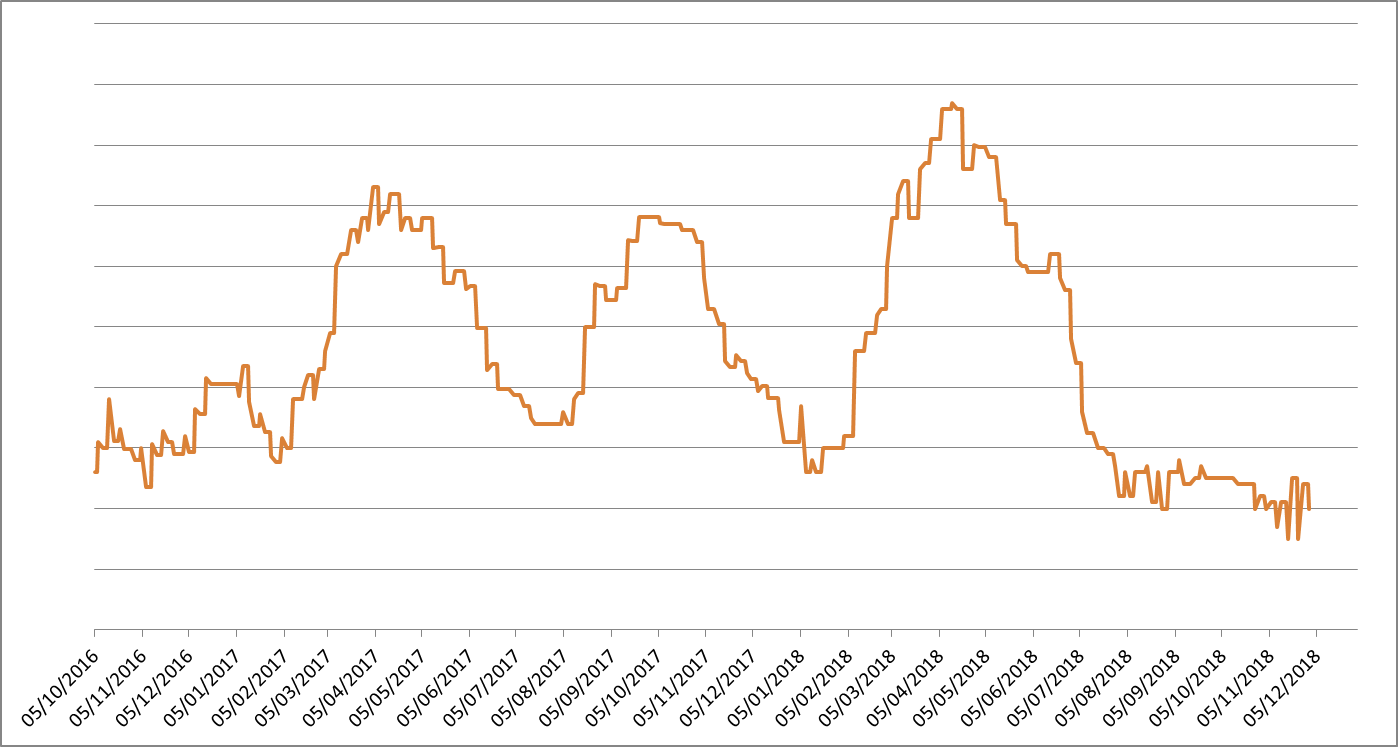

The average price of Phthalic Anhydride, which was $980.7/ton in 2017, is expected to increase at a compound annual growth rate (CAGR) of 3.2% to $1148.0/ton in 2022.

During 2008 to 2017, India was a net importer of Phthalic Anhydride. Imports as percentage of demand rose from 18.5% in 2008 to 35.6% in 2017. According to GlobalData forecasts, imports as percentage of demand is expected to decrease to 19.2% in 2022.