No it’s not trading at ex split price.

2 Likes

Company Mgmt announced few months back their intention to split the stock. Approval and other legal process will take time …My guess is that the the entire stock split process may take 4 to 6 months.

1 Like

Stock split of 10: 1 is not in Intention stage. It has been approved by the board in its May 3rd meeeting subject to shareholders approval , which is expected to be ratified in July 24th AGM. Thereafter it may take few weeks to complete the split. FYI

2 Likes

Have the sales for the value added products started?

In the annual report ,I could not find any revenue breakup for different products sold by the company

Any information on revenue generated by the company split geographically

Also if any of you have the details on how much capacity ,the company is running

I understand that it is a duopoly industry with high entry barriers, can anyone please help me understand regarding the overall demand for PAN worldwide and in India.

I am quite new to investing,so please correct me for any mistakes

Hi Everyone,

I have a question. Rally for this stock has started in 2015 where the crude oil price which is raw material for PAN has started declining and the same is visible in reduction in material costs (expenses) over the past few years which resulted in better OPM and net profit.

But my question is, as per below link on ET

->The improved profit was on account of lower import of PAN (which reduced supply) and higher crude price.

How could higher crude price (raw material) improved profit for the company which is in contrast when we look at the material cost decline in expense. Can someone please confirm if the above statement was wrong in article or my understanding was wrong as even the price chart of crude oil suggests, there was decline during 2015 phase.

->When crude dips, paint companies slow down their purchase of PAN in anticipation that the price of the chemical would soften. The reverse happens when crude price hardens

As per above assumpition, paint companies should have slowed down their purchase of PAN during 2015-2016 phase (2015 -1072 cr sales , 2016-944 cr sales).

But again from 2017 crude oil price has been increasing which should have increased the raw material cost in expenses but as per data in screener.in, its reducing every year which is ambiguous.

3 Likes

True, there is a discrepancy. You have asked the same question, again and again, that Crude price and raw-material price trends do not match. Likely explanation is that Crude can be hedged, as also the impex forex transaction part, both these components can mitigate their direct impact of RM costs. I would rather try to analyze the correlation with the added info that the company can pass on the RM costs and also that the market has expanded, with protection from imports.

Disclosure: 2% stake in portfolio @ average price of 1685, reduced from 4% stake, invested starting since sept 2017, averaged over time.

The following info from AR 2018 will allay some fears expressed by members on crude oil impact.

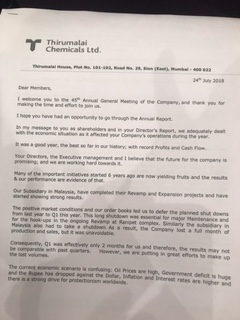

Chairman’s message in AR 2018…

…We were able to competently manage the disruptions and

uncertainties: rising Crude and Raw material costs in the

second half of the year, knee jerk tightening of credit for

our customers after the deluge of bad debts at all major

banks, and the trade hiccups caused by demonetization

and GST.

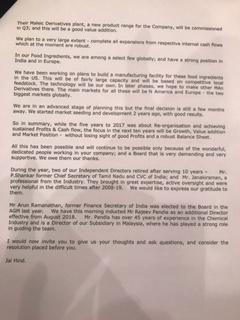

In the Director’s Report…

…The PA business is sensitive to market volatility and business

cycles. We are now better prepared to tackle these challenges

with the policy and operational changes, implemented in the

last few years.

But the large imports of the product into India is a matter of

great concern. The Government has initiated a review of the

Anti-Dumping Duty that was in force from Dec ‘12 to Dec ‘17.

Free Trade Agreements (FTAs) are another area of worry for

the Phthalic Anhydride business. While the existing FTAs with

ASEAN and Korea had a negative effect on Indian industry, the

proposed RCEP could prove to be a more serious threat to all

Indian manufacturing and jobs. Your company is participating

actively in a series of representations to the Government

through different forums.

Notwithstanding these threats, your Company is confident of

its ability to compete and grow.

1 Like

Tipid results for Q1Fy19. Below Mkt expectation.

Appears,to have a negative trend in terms of sales established now. What is the reason?

Is there a fall in demand for Thirumalai products or is there effect of dumping from Korea etc.

Do we have a view on the management .

Some marquee investors have reduced their stakes but have they exited?

Appreciate the groups outlook for the future and reAsons for the declining performance

If you see margins has improved from 18 percent to 22 percent even when crude prices were higher in first quarter. In my view, sales has declined due to deferment of purchase by Paint companies etc. In one of the news paper article (Need to search on google-will post) it was mentioned that if crude price rises then margins improve for companies like Thirumalai etc and sales drop due to deferment of purchases as (paint companies must be anticipating drop in crude oil prices). Even in such a volatile scenario Co. is able to post EPS of 30 plus due to higher margins. Big investors like Dolly, Anil holding is intact… marginally declined in case if Dolly Khanna.

Attended the AGM today. Mr.Parthasarathy mentioned that there was a plant shutdown for nearly a month at Ranipet and also in Malaysia due to major maintenance and hook ups which was essential and unavoidable. This is the major reason for fall in production and sales. Shutdown was deferred from last year to Q1 of this year on account of positive market conditions and order book of last year. They will try to make up for the lost volumes in rest of the months.

I wonder why they have not mentioned this in Notes section in quarterly results.

3 Likes

Ok thanks… Any other important commentary from management?

1 Like

Cannot read the text. Can you post a higher res picture?

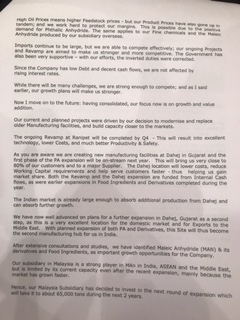

Attended the AGM today, which was followed by an investor meet. As stated in the CMD’s statement posted above, the Q1 results pertain to merely two months of working. The upcoming Dahej plant will be a game changer for the Co., as currently the plant is about a thousand kms away from both the main raw material supplier as well as the main customers / exports. This is likely to add 10 to 15% to the profitability from location change alone.

The current capacity of both the Ranipet & Malaysian plants put together is about 1,85,000 tons. Post the Dahej facility & the Malaysian plant expansion, another 1,00,000 tons are likely to be added over the next two years in stages. The mgt. is extremely reluctant of leverage, & the entire expansion will be funded from internal accruals.

The current margins are more than likely to sustain, as a number of plants world wide have shut down over the last 4-5 years. Even post the current expansions carried out by the Co., as also by the competitor IG Petro, India will continue to be net importer. Apparently, even setting up a PAN plant is a multi year project for a new entrant.

There are only a limited number of players world wide. China continues to be a net importer of PAN.

11 Likes

It is probably posted on the Co. website as well by now. Please check, or I’ll do the needful.

Hi Rajeev,

Thanks for the update. Any specific reason why margins have increased even when crude was higher… In one of the article, it was mentioned that margins increase if crude goes up… Is it true?

Rajeevji - please re-post CMD’s statement again as it’s difficult to read your old post. Sorry, I didn’t find it on the company’s website. Thanks!

Thirumalai AR 2018. Includes Chairman’s message on page 12 There may be some update which was circulated during AGM, which is not yet in public domain.