Point taken. Thanks for the insight. I know the PF is not perfect at the way I want it to be. I’m more inclined to a tighter PF of around 10 stocks. I’ve recently exited large caps like Sun Pharma, ONGC and going to exit NMDC.

How about exiting HDFC and LIC HF and entering Repco?

As Peter Lynch said, the best stocks to buy might be the ones you are already holding. Do consider you reasons of holding the current pf stocks and their respective weightages. What kind of growth lies ahead, are there scope of further consolidation - these answers should come from within as you read and learn more about the companies you hold. In this process you will gain the much needed CONVICTION, to hold and add on to your winners.

Not everyone needs to buy the same set of stocks. Investors often feel left out and hurriedly buy into pricey stocks at the wrong point of time. This is not to discourage you from buying into wonderful businesses like Page or Repco but the buying rationale should be more broad based and depended on relative merit basis against your current holding.

Agree with Rudra on building the conviction. You need to build your conviction first before you make changes to your portfolio. Else it becomes very difficult to hold during any correction.

I know that only stock ideas can be borrowed/cloned and not conviction. I myself have mentioned earlier in this thread that “Personally, I can’t just go and buy just because someone says it is a good pick/hot stock etc.”

I don’t like churning PF regularly and there would few changes in the past 1 year unless I’d gone and bought aggressively.

Exited NMDC. PF down to 16 stocks. Added some more Avanti Feeds at CMP yesterday. It is now 6% of my PF. Was not able to add as much as I wanted due to it hitting the upper circuit.

Considering PI Industries/Dhanuka Agri, VST Tillers and Accelya Kale. Am reading the ARs and I like Dhanuka/PI Industries more but the same old catch. Good business but stretched valuations. Thinking of exiting HUL too as I’m not happy with the high royalty payments to Unilever.

Moving to a more concentrated portfolio. Exited HUL. Added to Ajanta, Mayur and Avanti. (All the trading done approx 2 weeks back and not today). PF looks like this now:

Ajanta Pharma

15%

LIC Housing Finance

10%

Mayur Uniquoters

9%

Kaveri Seed

8%

Lupin

8%

ITC

7%

Avanti Feeds

6%

HDFC

6%

Tech Mahindra

6%

TCS

5%

Shilpa Medicare

5%

HDFC bank

5%

Amara Raja

4%

PFC

3%

Tata Motors (DVR)

2%

Cash

10%

I'd bought PFC and LIC HF during the August 2013 carnage and when I was a even bigger newbie than I'm today. Sitting on 140% and 90% returns respectively. Going forward, I would want to move to a better businesses. Should I just hold them and not add any new positions (ride out the MODI-fied rally) or exit and add to cash/other stocks in PF?

It is a work in progress. Adding to ICICI Pru Life, Wonderla and Alembic Pharma as and when I’ve money to invest. [Edit: On second thoughts, what the heck, I can and will add to any of the stocks I hold as and when I’ve money.]

Thoughts

Fully invested. Surplus from my salary and redemption of ELSS funds gets invested. My wife “diversifies” our networth by allocating some money in balanced funds, FDs, etc. I aggressively invest. Even to extend of buying only one share. I feel finding ways to increase income surplus, leading a simple life, investing aggressively is important than finding the next HDFC Bank.

I’m consciously diluting my concentrated portfolio by adding Wonderla and ICICI Pru Life.

Equity investing is hard and difficult but very emotionally satisfying, mind stimulating and enjoyable. Atleast I feel it is with Indian markets. If you see I don’t very strictly follow the “cheap” stocks. I wish to invest in India’s best businesses and hopefully pay a lower price for it. I feel MOS comes for the huge opportunity in front of the business, etc. Even with this mentality I couldn’t get myself to buy Britannia. I added a lecture of Shri Balakrishnan (one of the founding member of CRISIL) who said: “I own Nestle and wish to add more (after that Maggi fiasco) but it is just not cracking!”

Recently bought an iPad and I like it a lot for reading. I’m buying more Kindle books, reading magazine via Magzter, reading atleast one RHP every week, reading documents, etc. Thinking why I did not do this earlier.

@sammy11

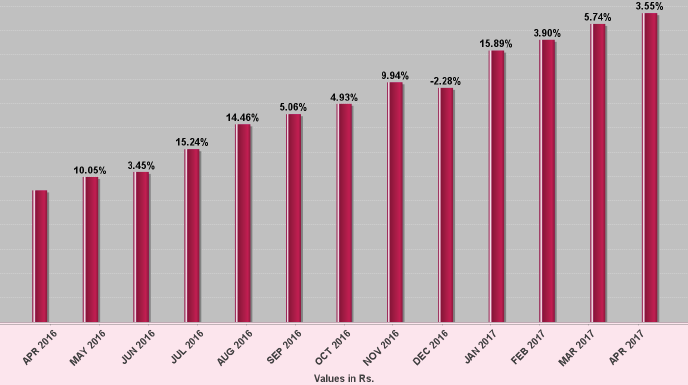

My PF is 3.5 years old now and the trailing year return is 38%. Last calender year it was 21% and on the whole it seems to have returned around ~40% CAGR. Apart from that I get dividends to tune of 0.9-1% of PF value every year.

Well thought investing process. All the best for your equity investing journey. Its important to build right temperament for successful equity investing. Be fearless when your are convinced in your investing thesis, but at the same time need to be equally hard to get convinced first. I believe that one gonna make money in equity investing by only having an edge over fellow investors and most of the times the edge comes from counter acting to market participants irrational behavior. The real winners are those who have guts to stand against the market and behave rationally and logically than those who nod cherry consensus. In addition, other important think is MoS and that comes from your understanding of the industry, company and weakness of other market participants. Remember what B. Graham said " Market is there to serve you and not to instruct you". Don’t let its behavior govern your behavior. Thanks.

Hi, Can you please provide your rationale behind this 3 stocks, ICICI seems very good choice, but not sure about the other two.

As I am novice in share market, your analysis and views will help me to understand the stock picking process. Waiting for your words. Thanks in advance.

]

]