Hi Amay, I had merely gave the highlights of concall, so if any one tracks the co , it might helps them.I am not holding any shares , nor i am tracking this company.Hope this clarifies the mater.

Hi Amey,

The co. is planning to exit the wind energy business as most of their wind capacity is in TN, and its no secret that TNEB is having troubles, to say the least.

I learnt the hard way that the wind farm business model is not asset light and suffers from govt. intervention & policies in more than one way. Going by the pickaxe & shovel theory, if I am keen on the renewable energy sector, I would look for a turbine supplier who knows how to control debt (not a Suzlon). But I think that even this would be a medium term story (5 to 10 years), e.g., in solar energy space, albeit at a very high growth rate, after which growth would subdue. If you are happy with FD and inflation beating returns, then SJVN might fit the bill, but I guess that’s not what you are looking for. I would only focus on the EPC business of Techno as a prospective investor.

Disc.: Sold off long back. These are just my opinions on the renewable energy space, and not buy/sell recommendations.

2 Likes

Co rep. by D P Gupta, CMD & Ankit S, MD.Key takeaways by Capital Mkt

Booked orders worth Rs 800 crore in the last 5 months. And thus order book (excluding L1 orders) as of now stands at Rs 2200 crore. Of the current order book about 30% is PGCIL orders, 10% from NTPC, 10% Industrial and balance 50% is from SEBs. Average order execution cycle for the order book is 20-24 months.L1 orders as on May 2015 stands at Rs 300 crore.Sitting with healthy order book, the company looks a growth of 30% for its EPC business for FY16 with matching growth in bottom-line.

Going-forward the company like to concentrate on EPC as well as T&D business.Green Corridor project with an outlay of Rs 10000 crore and funded by KFW loan is already on in Gujrat, Rajashthan and Wind. In second state states of Maharashtra and Karnataka will be covered.In Green Corridor project executed by PGCIL, the company bagged substation orders worth Rs 370 crore.The share of the company in Rs 545 crore Solapur-Kolhapur-Satna Transmission project is about Rs 300 crore.

The company already sold 44.5 MW of wind assets in Tamil Nadu for Rs 215 crore. Post divestment of 44.5 MW the company has 163 MW of wind assets which worth about Rs 850-900 crore.

Average order size for the company increased and now stands at Rs 75-200 crore from about Rs 40-50 crore. The company has adequate execution bandwidth. The company typically has about 40 project locations presence and that will be maintained.Sustainable EBITDA margin in FY16 is about 14%.

The EPC business is very asset light.REC sold in Q4FY15 was 80000 numbers with realization of about Rs 12 crore. Current REC Inventory is about 2.5 lakh. The SC order given encourage for REC market.

The proceeds from selling wind assets will be used to build BOOT portfolio as well as enhanced dividend payout to share holders. The company will take appropriate decision on special dividend.

CONFERENCE CALL - from Capital Markets

Techno Electric & Engineering company

Sits on strong order book of Rs 2050 crore

Techno Electric & Engineering company held a conference call on Feb 8, 2016. In the call the company was represented by PP Gupta, CMD & Ankit Saraya, Director.

Key takeaways of the conference call

Order book as end of Dec 31, 2015 stood at Rs 2050 crore. In Q3FY16 the company bagged orders worth Rs 160 crore. Further it has put in bids for tenders worth Rs 1500 crore which are yet to open.

Prospects - larger investment in various state utilities and pgcil. But there are differential power cost due to transmission bottlenecks and this situation to continue till we have transmission infrastructure.

The company is in the process of exiting from wind energy business. The proceeds will be used for PPP projects and growth of the same.

Second PPP project is on schedule.

Margin on quarter to quarter basis is not a good idea to look at. Additional service tax and sales tax of 2% commenced from October 1, 2015. Service tax could not be passed on to utilities and the company was forced to absorb. The outgo on this count is about Rs 5 crore. Rupee depreciation in Q3FY16 also hurted. The standalone other expense account Rs 5 crore of forex loss.

On course to attain target EPS of Rs 24-25/share for FY16.

Solar EPC foray of the company is in JV with a Chinese company. The company is targeting NTPC projects especially the 6 modules of 125 MW each in Anantapur setup by NTPC.

Expects an order intake of about Rs 400 crore in Q4FY16. If solar break through happens the company expects to close the fiscal with an order book of Rs 3000 crore otherwise at about Rs 2000 crore.

If solar break through happened this fiscal or early next year the company may touch a sales of Rs 1500 crore for FY17 given shorter execution period for solar projects. Otherwise the company is looking at a sales of about Rs 1250 crore.

The company expects the margin for solar at about 8-10%.

REC inventory as end of Dec 31, 2015 was 2.5 lakh units. Another about 30000 RECs is expected to get liquidated in next 2 months.

PGCIL awarding start happening in Q4FY16.

The company has qualified for 3 BOOT transmission projects for which price bids are yet to be submitted. The company is confident of bagging atleast one of the three projects.

1 Like

Techno Electric & Engineering Company Ltd has informed BSE that the Board of Directors of the Company at its meeting held on July 14, 2016, has recommended the following for approval of the Members through Postal Ballot and e-voting:

- Issue of Bonus Shares in the proportion of 1 (One) Bonus Share of nominal value of Rs. 2/- (Rupees Two) each for every existing 1 (One) fully paid-up Equity Shares of nominal value of Rs. 2/- (Rupees Two) each.

The said meeting of the Board commenced at 2.00 p.m. and concluded at 4.00 p.m.

T&D INDUSTRY

-

India’s energy consumption has nearly doubled since 2000

-

Power demand in India is expected to grow from 120 GW to 315-335GW by 2017 - as per McKinsey study.

-

Coal availability will increase with coal mines leases renewed and forest clearances granted. 10 mines are to be added by Mar 2016.

-

The government is expecting an investment of about US$ 250 billion by 2020. Renewables are set to get US$ 100 billion, while the transmission and distribution segment will get US$ 50 billion, each. Another US$ 60-70 billion will be for power generation, including for restarting stalled projects and for new ones while US$ 5-6 billion is set aside for energy efficiency projects. Besides, US$ 20-25 billion investments would come for associated infrastructure required in replacement of old and out-dated equipments, among others.

-

Key focus area is integration of renewable energy to the grid

-

Discoms have an accumulated loss of 3.8 lakh crores and debt of 4.4 lakh crores (as of Mar 2015)

-

UDAY scheme entails the state govts to take over the debt and future losses (in a staggered manner) from the Discoms

-

Government plans to roll out green energy corridor’ project at an estimated cost of INR 43000 cr to facilitate the flow of renewable energy into the National Grid.

-

Renewable power has been declared as a priority sector for bank lending from 2015

-

215 cr is the sale proceed for 44.45 MW. 4.83 cr / MW sale price. 162.9MW of wind power capacity remaining.

-

Promoter has 58% stake in the company

-

Mutual funds hold 17.2% and FIIs 5.4%

-

The co is involved with more than 50% of both NTPC and Power Grid’s projects; it has relationships with 1500+ vendors

-

One of the first few T&D contractors, who have teamed up with Chinese player Rongxin to participate in STATCOM projects. Have first mover advantage in STATCOM space in India.

-

Govt plans to install 50 STATCOMs in the next 3-5 years with a total spend of 8000 cr.

-

In 2013, the Patran transmission project was completed completely on supplier credit

-

EPC division produces 92% of the revenues

-

Co has a working capital cycle of 35 days vs 66-182 days of competitors

-

The Ministry of Power has planned to provide electricity to 18,500 villages in three years under the Deendayal Upadhyaya Gram Jyoti Yojana (DDUGJY).

-

A few Ultra Mega Power Projects of about 4,000 MW capacity each are in the offing

-

Power Grid Corporation of India is to build sub transmission system of 220/132kV in 6 North East States at an estimated investment of Rs 15000 cr over a period of 3 years. Already bagged order to the tune of Rs 170 Crores to build 400 kV GIS substation at Assam under World Bank funded NER Power System Improvement Project.

-

Got an order worth Rs 600 cr for substation package at Chittorgarh, Tuticorn, Ajmer and Bikaner associated with Green Energy Corridors: Inter-state Transmission Scheme (ISTS)

-

Order book at end of Mar 2016 is 2,600 cr, 69% of which is from PGCIL

-

Co has a zero penalty record resulting in realization of retention money within 6 months of project completion

-

During 2015-16, around 28,000 ckm (circuit kilometre) of transmission lines were commissioned against 22,000 ckm last year. This is 118% of the annual target set and also the highest ever for a single year.

The power sector is transforming with large investments in various govt initiatives. T&D is on focus as well as renewable energy sector. The next few years may see a thrust in this business.

DISCLOSURE: I currently hold the stock.

1 Like

Good results from Techno

http://www.bseindia.com/corporates/anndet_new.aspx?newsid=36dc039a-da07-4f7f-acc0-f24926727e0f

1 Like

Annual report for 2016 is out - http://www.techno.co.in/Content/InvAnnualReport/Techno/Techno%20Electric%20AR%202015-16.pdf

Techno Electric one of the top holdings in top midcap funds

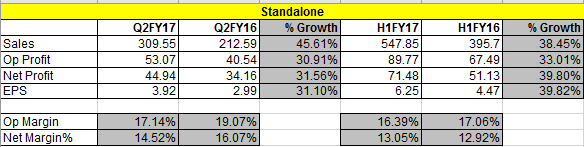

Q2 results - Good growth continues

1 Like

HDFC Sec has come out with a report on Techno – http://hdfcsec.com/Share-Market-Research/Research-Details/StockReports/3020579

Salient points:

Investment Rationale:

Strong track record in EPC segment and specialized in substation commissioning

TEEC has a strong history of selective bidding, thereby chasing profitability over growth and having an asset-light business model, wherein it has the best asset turns in the T&D EPC space. Within EPC, TEEC can execute BOP packages, switchyard/substation works and distribution/rural electrification works. However, it has built a niche in the substation space, which is likely to be the company’s focus in the future. TEEC is also pre-qualified to execute 765kV GIS substations. In comparison to transmission line EPC, substation EPC is low on project management. However, it requires strong designing/engineering skills, sourcing of equipment and a good understanding/tie-up with the GIS equipment supplier. There are only 4-5 players in 765kV GIS substation, thereby, making it relatively less competitive than transmission line EPC. This is also reflected in the margin profile of TEEC vs. KEC/KPP.

Power Grid’s (PGCIL) incremental substation orders to benefit TEEC

Given the long history of sub-par transformation capacity, PGCIL’s investments in substation EPC have increased tremendously in the past 2-3 years. This augurs well for TEEC. With increasing costs/other issues related to land acquisition, incremental investments are leaning towards GIS instead of AIS. With a limited number of players in the EHV GIS substation EPC space, TEEC is well placed for growth over the next 4-5 years.

TEEC (jointly with the Chinese company Rongxin) recently won the first STATCOM order in the country. With increasing contribution from renewables, STATCOM will be extremely important to maintain grid stability. India has been a late entrant in this space. PGCIL now plans to install 50 STATCOMS over the next 3-4 years, with an expected investment of Rs 80bn. Even though the Power Grid’s budget remained at same level for the year but it reflected shift in its investment pattern. Traditionally the ratio of Power Grid’s investment in lines and substation was 80:20 respectively but in FY17 it has witnessed more investment in the substation side which took the ratio of line to substation to 65:35 respectively; which goes well with TEEC’s capabilities and increases company’s addressable market.

Building a good portfolio of T&D BOT assets

Insulating itself from the EPC business’ cyclicality, the company is building a portfolio of infrastructure assets with regular cash flows and decent IRRs. Historically, the company ventured into building on a portfolio of wind assets. TEEC has a wind asset portfolio of 163MW (45MW in the standalone entity and another 118MW in its subsidiary, Simran Wind Projects).

However, given the issues in monetising the renewable energy certificates (REC), the returns have been lower than expected. The company recently demerged 45MW of wind assets in the standalone company and plans to exit the entire business in the next year. TEEC is focused on expanding its T&D BOOM asset portfolio. In the past two years, it has won two projects (equity capex of Rs 900mn, one operational and other soon to be operational), which have multiple benefits in terms of captive EPC opportunity and annuity-based cash flows/decent IRRs. We estimate TEEC projects to have an IRR of 14-15%. Even in the T&D BOOM projects, TEEC is focused on ones with higher substation component and lower line component to maximise the captive EPC opportunity. The company plans to bid for many such projects, albeit selectively. While it is comfortably placed in terms of leverage and operational cash flow, the sale of wind power assets will free up capital to be invested in T&D BOOM projects and reduce variability in earnings over the medium term. This will also enhance revenue visibility of its EPC business.

Large order book provides visibility to revenue growth:

The current order book of TEEC is close to Rs.2600 cr which is almost 2.5xFY16 EPS sales. The order book has grown at a healthy CAGR pace of 25% over FY13-FY16. Though dependence on PGCIL from an orders perspective is large, it plans to derisk its business going ahead by bidding for orders from SEBs and private players too. It has identified north east India as a focus area.

4 Likes

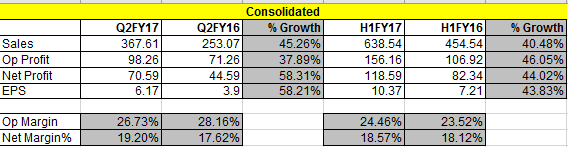

Q2 Concall Summary

- order book as on 30th September 2016 stands at Rs.2,500 crores, which includes our L1 position in 765 kV Substation Package at Raigarh, Indore and Itarsi and the package value is about Rs.150 crores.

- For PGCIL, the ratio of investment between line and substation has undergone change from 80:20 to 65:35.

- In Wind segment the related challenges have eased, we are witnessing improvement in grid availability in State of Tamil Nadu and the overall wind flow has been positive.

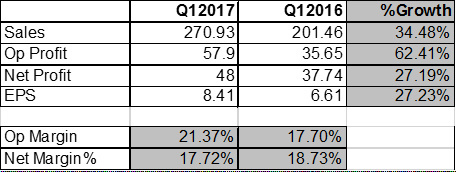

- Revenue from EPC almost jumped by 47% from Rs.202 crores to Rs.297 crores. Consolidated revenue for the quarter also grew by 34% to Rs.368 crores against Rs.253 crores achieved during the same quarter of the previous year.

- Operating profit for the EPC segment for the quarter stood at Rs.45.88 crores as against Rs.33 crores, showing a jump of 38.56%. Operating profit margin for the quarter stood at 15.46%.

- The PAT on standalone basis for the quarter stood at Rs.44.79 crores as against Rs.34.07 crores last year, showing a growth of 31.46%. On consolidated basis, the PAT has jumped by 58% for the quarter at Rs.70 crores against Rs.44.5 crores.

- able to manage the receivables within 100-days cycle which is one of the best in the industry.

- Outlook is very positive. States are now coming more ahead of the Power Grid also in building their own networks particularly the states having more of renewable power with them as well as some transmission networks with the other states. Seeing a strong momentum in the State of MP, Rajasthan, Chhattisgarh, Andhra, Telengana, Tamil Nadu, all are becoming fairly active.

- there is no impact on margins with more orders from state electricity board

- payments are received directly from the funding agencies like REC/PFC/ADB

- Domonetization has not adversely impacted operations. On the contrary, it has helped. Construction material cost is now 10% to 15% lower.

- Consolidated debt is 300cr (275 cr in Simran and 25cr in Techno). Practically, short term debt free (5 cr)

- Cash balance is 225 cr

- expect our PAT margin over consolidated top line to be around 14.5-15% this year as against 11-11.5%

1 Like

Techno Electric sells 33 MW wind power assets for Rs 165.19 crore

Techno Electric & Engineering Company has sold 33 MW Wind Power Assets situated in the State of Tamil Nadu at an effective valuation of Rs 165.19 crore.

Techno Electric & Engineering Company Ltd has informed BSE that the Company has sold 33 MW Wind Power Assets situated in the State of Tamil Nadu at an effective valuation of Rs. 165.19 Crores. Post this transaction, the Company

continues to hold 12 MW of wind power assets.Techno Electric along with its subsidiary, Simran Wind Project Limited will have a portfolio of 129.9 MW of wind power asset post above transaction.

Good move by the company and in line with their stated plans of slowly divesting the wind power assets.

Techno Electric Board to consider Buyback of shares on Feb 10th '17 along with Q3 results.

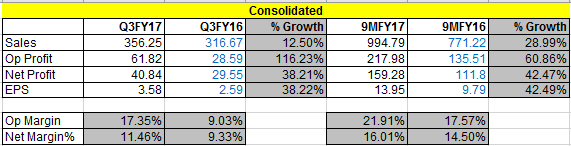

Q3FY17 - Strong momentum continues

Company sent letter of offer for buyback to shareholders. Attaching for reference.

Techno_Electric_and_Engg_Co_Ltd-Buy_Back-Letter_of_Offer.pdf (704.0 KB)

Discl: Invested

@basumallick - Thanks for the regular updates on Techno Electric Basu bhai. Undoubtedly, TEEC is doing very well from the last 3-4 years. I was looking to invest here but what stopped me from doing so was its current valuation - that it is now trading at a trailing 21 p/e. So, as an investor i need to think if this is still undervalued. Well, everything else is very “right” about this company (good promoters, good cash on books, lowering debt, improving return rations, improving margins, strong order book, etc) as has been discussed here on the thread. Imho, undervaluation is very much a subjective term; it depends majorly on the opportunity size ahead along with the trailing multiples, order book size, etc. To understand the opportunity size, i did some more reading and found some interesting articles.

Excerpt from the above article -

The whole concept of India being power surplus is so misleading. In India, 300 million people don’t have access to electricity, and power cuts are rampant. Per capita power consumption is significantly lower than the world average. On the other hand, the Power Ministry says India is power-surplus.Well, surplus or deficit is determined by calculating the difference between the demand for power and availability. It is the definition of “demand” that lies at the base of this paradox. While calculating power demand, only people who are connected to the grid and have access to electricity at present are taken into consideration. “Power for all” is still a far fetched dream.

Some of the growth triggers ahead which will lead to huge electricity demand ahead -

- Doubling the agricultural income (which government has been projecting for 2022)

- The country ultimately has to move to electric technology and electric vehicles (very long term)

- Still over 30 cr people in India are not connected to the grid

- India is increasingly adopting non conventional energy, which is going to open new horizons for companies like Techno Electric. Non conventional energy management require advanced substations.

Another interesting thing is them developing T&D BOT assets to remove earnings cyclicality. Though, what i am trying to find out here is that where we are at the moment in terms of this up-cycle? Still in the nascent stages seeing the opportunity size ahead despite the company been performing very well in last 3-4 years? Or has the majority of up-cycle already played off?

4 Likes

From whatever I have seen, read and understood from the industry veterans, the T&D market is picking up, so its more in the initial stages of an upswing. If you look at near term financials, valuation is fair, with not much margin of safety. However, for investors with 3-5 years horizon, this space does give good opportunity for compounding at the above average rate.

3 Likes

Techno announces the transfer of 12 MW Wind Power Assets to Wholly Owned Subsidiary Company, Simran Wind Project Ltd. With this it takes one step closer to getting out of the wind power business altogether. That will leave the company focusing on the core EPC business.

2 Likes

March 2017 results update:

- Topline growth for the quarter is ~9% YoY

- For the whole year the topline growth is ~19%

- EPS for March 2017 is 3.78 compared to 2.73 in Dec 2017 and 2.77 compared to March 2016

- EPS for whole year is 12.76 compared to 9.35 in 2016.

- The jump in EPS this quarter is due to other income of 2334 lacs due to sell off of the 33 MW of Wind Division Assets.

- Remaining 12 MW of Wind Division has been fully transferred to subsidiary SImran Wind Project Ltd at book value.

- Buyback was completed successfully of 1500000 shares at Rs.400

3 Likes