TCNS Clothing Co. Limited is India’s leading women’s branded apparel company in terms of total number of exclusive brand outlets as of May 2018, according to Technopak. The Company designs, manufactures, markets and retails a wide portfolio of women’s branded apparel across multiple brands. The Company sells its products across India and through multiple distribution channels. As of March 31, 2018, the company sold its products through 465 exclusive brand outlets, 1,469 large format store outlets and 1,522 multi-brand outlets, located in 31 states and union territories in India. As of March 31, 2018, the company also sold its products through six exclusive brand outlets in Nepal, Mauritius and Sri Lanka. In addition, the company sold its products through their own website and online retailers.

The company’s product portfolio includes top-wear, bottom-wear, drapes, combination-sets and accessories that cater to a wide variety of the wardrobe requirements of the Indian woman, including every-day wear, casual wear, work wear and occasion wear.

Mr. Onkar Singh Pasricha and Mr. Arvinder Singh Pasricha are promoters of the company, each have over 40 years of experience in the apparel industry, and the Managing Director, Anant Kumar Daga, leads an experienced and professional management team. The Management team, including Anant Kumar Daga currently has a significant ownership stake in the Company. The shareholders also include a fund affiliated with TA Associates, a marquee private equity group.

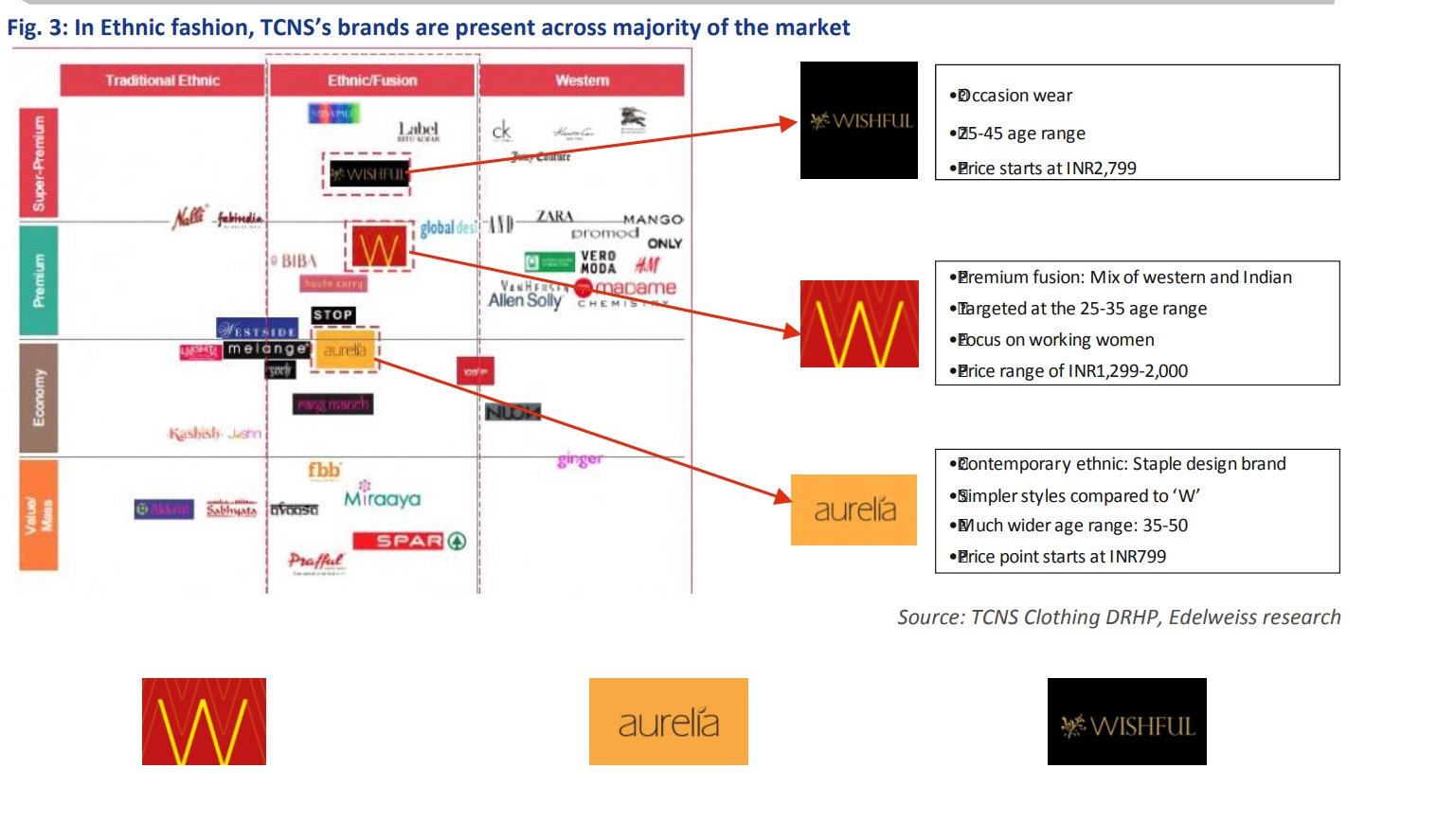

Mainly 3 brands

a). Brand “W”: “ W” is a premium fusion wear brand, which merges Indian and western sensibilities with an emphasis on distinctive design and styling. This brand is targeted primarily at the modern Indian woman’s work and casual wear requirements. “ W” has been recognized as the ‘ IMAGES Most Admired Fashion Brand of the Year : by India Fashion Forum consecutively for past three years between 2015 to 2017 . “W” had 258 exclusive brand outlets and 676 large format store outlets located across 148 cities in India and five outlets outside India.

b). Brand “Aurelia”: Aurelia is a contemporary ethnic wear brand targeted at women looking for great design, fit and quality for their casual and work wear requirements. “Aurelia” had 159 exclusive brand outlets and 629 large format store outlets located across 149 cities in India and one outlet outside India.

c) Brand “Wishful”. Wishful is a premium occasion wear brand, with elegant designs catering to women’s apparel requirements for evening wear and occasions such as weddings, events and festivals. The Company is leveraging their “W” store network for selling Wishful products, however, they recently launched first exclusive brand outlet for Wishful, in September 2017.

Revenue from sales of products under brand “W” , “Aurelia” & “Wishfulgrew” is growing at a CAGR of 48.67 %, 70.82 % & 66.66 % respectively during FY13 to FY17 . Moreover, in FY17 the revenue from “W” , “Aurelia” & “Wishfulgrew” accounted for 61.23% , 30.35 % & 8.41% respectively.

Risks:

Slowdown in demand for TCNS’ products due to change in customer preferences and lower

brand appeal are key risks. Competition from other brands, including from private labels

retailed by channels such as large format stores and e-tailers are also risks. F

Disclosure: Not invested

looking for views from everyone

It is a good play on branded ethnic wear of ladies, good growth in past and looking for better growth ahead