Kagome’s main business lines don’t overlap with PBI and there is only one area “Institutional & Industrial Product Business” which have commonality. Here is the profile of Kagome in detail (and luckily in English

Regarding production, each and every plant of Kagome is in Japan only and 100% owned by them. I am skeptical, if a Japanese company would start manufacture in India for Food Grade item at least in 2 - 3 year time frame of a purchase where they don’t have full ownership control. It is my subjective view and can be totally wrong.

If the Institutional Business they like to grow in India in the longer term, I do think TBEL would be benefitted. On Tomato based product line of Kagome, I guess Pune / TBEL has no edge as biggest Tomato growing areas in India are AP, Karnatkaka and MP (40% of total) and then West Bengal and Maharashtra (14% of total).

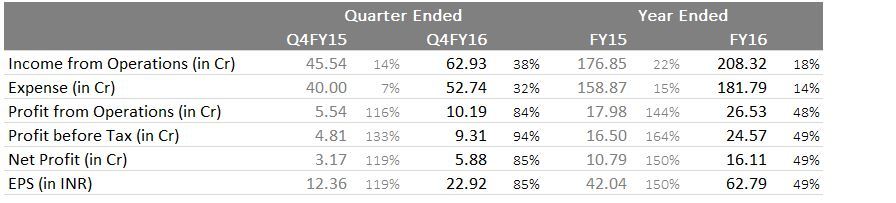

June’15 quarterly results out:

YoY (June 15 Vs. June 14):

Topline degrowth of 10% (36.76 Cr Vs. 40.63 Cr)

Other operating income went down to 20.7 Cr (Vs. 27 Cr.)

EBITDA degrowth of 19% (34.67 Cr. Vs. 42.4 Cr.)

NP degrowth of 15% (21.88 Cr. Vs. 25.66 Cr.)

I am a little confused with regards to the structure of Kagome deal. The deal in a way technically allows Kagome to leverage TB’s US distribution network and sell its products without involving TBEL.

Also, does someone have any idea on what was the shareholding structure before Kagome deal? I believe it was held by PE players and Ashok Vasudevan/Meera Vasudevan and others – pg 3 of http://www.kagome.co.jp/company/news/n_pdf/140415002.pdf.

I understand that this structure would be to give exit to PE players. But in the process, have AV/MV also partially exited? Currently they own 30% - what was their holding pre Kagome deal? And why did they exit partially, if at all – cashing out for years of efforts, especially at a time when they are talking of start of the third innings??

I am not able to clearly understand what good this deal does for TBEL and how different it would have been for TBEL, even if this deal hadn’t happened.

Also, why still continue with this manufacturing (TBEL) and marketing structure (PBI) – why not merge the two? Wouldn’t that simplify a lot of issues. What am I missing here?

a) 5 years of 25% CAGR.

b) Last year US (RTE) Business grew by +25%, domestic business grew by only 8% (FSSAI issue).

c) Aggressive growth in both segments this year. Do not give explicit growth targets,

d) Market reach in US doubled from 8000 to 16000 (out of 36000) outlets in one year.

e) FSSAI issues impacted India launches (Rockr was rejected). New launches this year Rockr Burger (KFC), Chilli Paneer Pockets (McDonalds). FSSAI no longer required to approve products as per supreme court order.

f) Started operation in UK this year. UK RTE market largest in world for Indian foods.

g) RTE market share for Indian food bigger than all other players (Haldiram, MTR, ITC etc.) combined.

h) Limited impact of food price fluctuation.

i) Working with local chains like FAASO’s.

j) Working on complete organic foods and will launch them in two years. Sourcing everything organic is very difficult. Working with farmers to grow organic rice etc.

k) Entered into a tie-up with Wendy’s UAE (15 stores) for QSR supplies.

l) Capacity utilization of various divisions: RTE (80%), Patties (60%), Sauces (50%).

m) New capacity to be added this year in RTE business. Capex plan 5.5 cr for one additional line (existing two lines).

Kagome Impact:

a) Largest manufacturer of Tomato Ketchup worldwide with far superior quality.Looking to develop tomatoes with Kagome help.

b) Will be using Kagome’s research in agricultural technologies.

c) Use each other’s distribution network.

d) Kagome’s name gives an easy entry in quality QSR, example cited was Wendy’s UAE.

Conclusion: Came out highly impressed with management.Entry into UK market +ve for RTE. Newer products with McDonalds, KFC, FAASOS shows traction in QSR. I liked their response on dividends where they said as long as we are able to deploy capital generating significantly higher returns than cost of capital the dividend payouts will be limited. Post that period they will increase significantly.

Anyone has any idea on how one can get PBI Inc. financials. Is there a place where private companies in the US are required to file their financials and these are available at a price?

Hi Bhaumik - Please write to Kagome Japan and try your luck. Being a publicly listed company, they might be obligated to send if enough of us write in.

This is as per Kagome’s Q2 presentation (Apr to June):

Kagome started consolidating PBI into their accounts from end of May this year. Their estimate of sales for the last two quarters (July-December) for PBI is 3.4 billion Yen (185 crores) . This is derived from Kagome presentation that says:

“Net Sales Plan by Segment FY2015 2nd Half: Net increase in sales by PBI (U.S.) (+¥3.4 billion). A weak yen will also have favorable impact.”

This is from Kagome’s 9 months (Jan to Sept) consolidated results:

The performance for PBI is from May end to September end (4 months) is sales of 5.18 billion Yen ( 282 crores). This is derived from Kagome’s statement that says:

“Sales to major food services customers were strong at Kagome Inc. Net sales at United Genetics Holdings LLC were at roughly the same level as the same period of the previous year, but there was net increase of sales at Preferred Brands International (“PBI”), which was made a consolidated subsidiary at the end of May 2015. As a result, net sales in the U.S. were up 37.4% from the same period of the previous year at ¥19.035 billion.”

Comparing this to last year (PBI) again from the presentation: In the period ended March 31, 2015, net sales reached ¥5.0 billion (272 crores), and operating income was ¥500 million (27.2 crores). - Revenue has increased over each of the past 7 periods, with an average growth rate of 17%/year.

Either I am interpreting something incorrect or it looks like PBI is having a dream run with May to September sales being greater than last year sales. For all the data and presentations you can look here: http://www.kagome.co.jp/company/ir/data/fy/index.html

Disclosure: Invested at an average price of 600 it forms more than 10% of my portfolio allocation. No transactions in last 6 months.

It is not listed in NSE.Further, what is the exit plan given the highly non-liquid status.( 2 week avg qty is only 580 shares). Though everything is excellent, how to we address these 2 factors. Nobody can predict what will happen in future.

I am generally biased against shares not listed in NSE. I did not invest in CUPID as I still view that counter with circumspection ( UC now and LC may be later, where one will not be able to get out). Though that scenario is ruled out here but still that worry is there. How do we address this?

I agree liquidity is less and a quick exit is difficult but that is not what I am looking for. Personally for me both of the above factors do not concern with BQ or MQ and are ignorables. Having said that I do look for liquidity at a portfolio level mainly to take advantage of opportunities that Mr. Market provides. Most of this liquidity come from cash or opportunistic bets (a small part of my portfolio) that I carry. For long term bets with high conviction and a long runway I do not worry about liquidity. Good mgmts. sort liquidity out in due course of time. I hope more people have NSE listing as a criteria for investment, I will gladly accept my improved chances on BSE .

Disclosure: Invested at an average price of 600 it forms more than 10% of my portfolio allocation. No transactions in last 6 months

I am surprised no one has noticed or mentioned that Kagome already has a 50:50 JV in India with Ruchi Soya which is engaged in manufacturing of tomato paste & sauce. This would mean that TBE may have very little chance of entering this business.

Excerpt from Kagome profile:

“Ruchi Kagome Foods India Pvt. Ltd. (India)

Established in 2013, Ruchi Kagome Foods India manufactures and sells industrial-use tomato products. because most tomatoes in India are consumed fresh, the consumption of and market for processed tomato products is expected to expand in the near future and Ruchi Kagome Foods India is set to lead the way.”

This is well known and was raised at AGM too where Kigome folks were present too. They did not take up the question and said this is not the right forum. To me Kagome’s tomatoes and Ketchups are small optionalities that do not matter much. Although the management did say that they will be using Kagome’s agri technologies for tomatoes.

CB offers Italian kit too; three pasta flavours. They made it to our kitchen sometime back. Have bad habit of reading details on package. Don’t remember seeing Tasty Bite name in Italian series.

Sorry, no comment on taste. Love to eat fresh food (old school).

The increase in loans and advances and account receivables scare me. It will be good if senior boarders can comment whether it is good or not?

Did not increase allocation after that because I still don’t trust that the parent will let Indian company earn profits as they are the distributor without any margin contraction.

DIsc. Invested from lower levels and <1 of my portfolio.

.

.