Excellent! Thanks for pointing out. That’s a mistake, I didn’t realise I had made an inadvertent recco ![]()

Recco-like Comment withdrawn, and being edited out from original post

9 Likes

55.80% is definitely a red flag . The ratio does not go below that extent in good and stable

businesses Shriram EPC is a failure and lot of other failures also. Business risk is different from honesty and integrity. The biggest risk in software is human resource and the next comes the debt.

Scuttlebut : This company is not rated highly in software circles and this competence can be built in a jiffy by big names like Oracle,Accenture who specialize in the same area.

Tracking but lack conviction to invest.

Hi Guys,

I just happened to come across an interesting write-up on Take solutions Ltd.(Good insights on the Industry and Company Level)

8 Likes

55.8% over a 3-5 year period is a red flag. This cannot be tracked yearly because there could be changes in working capital in a particular year leading to a low ratio. But, over a 3-5 year period, things should even out and if it is around 50% on a longish horizon, I would be worried. See Opto numbers - that is a good representative where the ratio was bad for the long-term - that is when you just say “the profits are just book profits not backed by any cash generation”

On market standing, well - how have they managed to win such a big contract - in Q4FY16 their lifesciences order book increased from USD 62 mil to USD 90 mil qoq - even if you say USD 12 mil was one-time and USD 8 mil was due to EA, there is another usd 8 mil contract win even apart from these possible one-offs - this is a 13% growth in order book even ignoring the large order - so, there is definitely a strong momentum which indicate some capability that the pharmaceutical companies see in their offering.

2 Likes

Please consider the following numbers and comment.

-

Debt ( both ST and LT) Rs 318 cr ( Mar 16) ( Rs 17 crs investments is there but we do have details as AR 16 is not out). Rest are bank balances. There is an increase in both in Mar 16.

-

Unamortised Product Development Mar 15 Rs 100 crs. We do not know how much added up for Mar 16.

-

Goodwill Rs 256 cr ( Goodwill is the price paid in excess of BV for acquisitions.

4 The Company has been paying about Rs 15 cr p.a as interest since 2011.

The size of the above numbers raises some concern a) It is a debt fueled acquisition - something can wrong or is it a right strategy b) Why to show a huge EBITDA Margin of 23% without adjusting product development costs as against the Industry practice ( Recall Majesco). The Company has adequate cushion to charge more by way of amortisation but the intention is not there.

As an investor, it is a sunk cost ( Goodwill and Product Development)for me and I would rather see whether the Company would be able to recover this especially where there is a debt. Debt is a strict no no for a software company from a risk point as well as an investor. Here it is about 50% of equity.

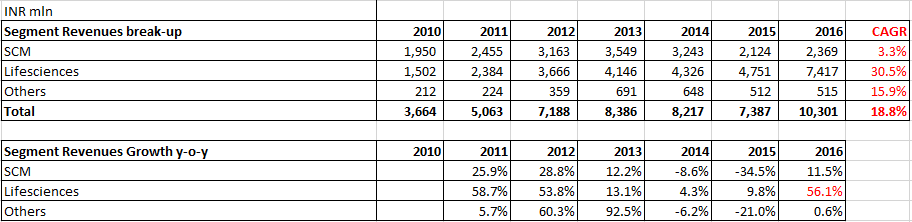

See the CAGR in LS between different years and Mar 15. CAGR is going down but we are yet to have a break up for 2016 as it is available in AR. Winning order alone does not guarantee cash.

From the above, Is it worth taking the risk ? In addition, complicated structure and 38 subs gives a uncomfortable feeling that the risk is mitigated/taken care of at promoter level in case something goes wrong. Shriram is only 10%.

2 Likes

I will comment on some of your issues:

Firstly, product development expenses:

A Company that wants to over-state profits can easily do so by capitalizing legitimate business expense - thereby that expense just sitting as an Asset and not hitting the profits. Between 2013 to 2015 - Take has expensed close to 100% of the amount incurred.

Also, look at the Unamortised Product Development Expenses Asset on the Balance Sheet. In 2010, it was INR 713 mln and the same is INR 796 mln in 2015 - this implies that there is not much under-reporting on this account.

In FY16, the Company has expensed INR 495 mln - on the Q4FY16 conference call, they state that they spent about the same amount in cash - this ratio being more than 90% at-least is important in my opinion.

Lifesciences Versus SCM Growth:

Lifesciences over a longish time frame has grown Revenues at 30% CAGR. In FY16, it grew revenues at 56%. There was a wall that it hit between 2013 to 2015 but things seem to have started looking up again from Q4FY15. Also, this is a business where the management should have good visibility as they have orders-in-hand as well as the pipeline to judge their forward revenues. I would be surprised and disappointed in this light if they do not do 25% Revenue CAGR in the lifesciences space.

Cash Versus Debt:

Well, the financials do suggest that the Company would, at all times would feel comfortable with USD 20 mln or INR 130 crores of cash on books - and is not going to use the same to repay debt. They pay abut 6%-7% on debt and earn about 4% on cash - so, its a negative yield for sure - but they want to be acquisition ready always and are ready to incur this net cost of say 4 crs every year (negative yield of 3% X cash of INR 130 crs). There are two issues one needs to be worried about 1. is the cash not there at all - based on the other understanding, I would assign a low probability to this 2. the Company can be too aggressive and do more debt-funded acquisitions - this is possible and that is the reason, this Company can be a double edged sword where it either creates huge value or can gets tied up in debt and blows up - but at the current debt/ equity and debt/ OCF ratio - their debt looks very manageable - but one needs to track.

About the subsidiary structure, I do agree its complex and would have preferred a simpler structure. But its ultimately a balance between valuation and quality. This is not Nestle quality - but its not Nestle valuation as well - it could grow at a pace far higher than the mid tier IT space where 12%-15% growth is very good - a wave of growth could sort out some other issues automatically - ultimately, if a business creates free cash, most other issues will solve themselves - lets see.

14 Likes

Hi,

Product development costs and Goodwill is a sunk cost for me and valuations have to be adjusted to that extent. We do not have data to verify whether their acquisitions are doing well and also how the product development costs are recovered so far. Here it is more important as they have grown by inorganic route. Whether they expense 100% or more , it is immaterial. Further, it shows an inflated EBITDA Margin. Whether that particular product has become cash positive, we do not know. It is prudent to knock the Rs 100 cr ( 2015 figure and not 796 mln as stated by you) and also GW.

Cash balances lying in the current account cannot be considered as cash equivalents. It may a debtor realised and sitting in the bank account. Your net debt calculation need to be revisited. They have only Rs 16 cr of investments.

Also, why a LT debt is not there much and there is huge ST debt. This itself shows there is a mismatch in financing of acquisitions and product development expenses. Just think any software company will be under pressure not to show LT debt. Just give me examples where a good software company is financing an acquisition by debt. I am not saying something negative here but it is a risk and negative point.

LS , see the CAGR at different years eg 1, 2 3 , 4,5 years and then you will make out. Dont see CAGR from 2010.

The Company may be good for future. The moot question whether risk is adequately covered when they have to compete with biggies.

Subex was the darling of equity investors including some big value investors once. Please read this excellent analysis which shows what a debt and intangibles can do a software company. Subex is a product company and so is another telecom company called i forgot the name it appeared in Valuepicker also.

As an investor, i would rather see the risk in acquisitions by debt rather than growth in acquisitions. This is only to highlight the risk and any investor should be aware of this. I am not not sounding negative here but only highlighting the risk.

The auditor is a small time one and cannot have wherewithal like Big 4.

1 Like

It is Sasken .It also met the same fate like Subex.

Latest interview of Srinivasan HR, Vice Chairman & Managing Director of Take Solutions.

Nothing new. But he has reiterated his confidence of a 25 percent organic growth in FY17 but also of sustaining similar growth for the next three years.

Video is not loading for me. But you can read the transcript.

qip floor price set at 174.84

When was this announced? could not find anything on BSE.

Its there in NSE announcements.

TAKE_QIP_NSE.pdf (170.4 KB)

Take Solutions Limited has informed the Exchange that subsequent to the approval accorded by the Board of Directors of the Company, at its meeting held on May 15, 2015 and the approval of the shareholders of the Company by way of a special resolution dated August 28, 2015 for the Issue, the Securities Issue Committee of the Company July 21, 2016 has, inter alia passed the following resolutions: a. Authorising the opening of the Issue on July 21,2016. b. Approving the preliminary placement document dated July 21, 2016 in connection with the Issue, (the “Preliminary Placement Document”); and c. Approval of the floor price for the Issue. Further, Company has informed that the ‘Relevant Date’ for this purpose, in terms of Regulation 81(c)(i) of the SEBI ICDR Regulations, is July 21, 2016 and accordingly the floor price in respect of the aforesaid Issue, based on the pricing formula as prescribed under Regulation 85(1) of the SEBI ICDR Regulations is Rs. 174.84 per Equity Share. Pursuant to Regulation 85 of the SEBI ICDR Regulations the Company may offer a discount of not more than 5% on the floor price so calculated for the Issue.

Thanks, little confused with the timing unless they plan to deploy immediate in an acquisition. They had cash on the balance sheet along with potential disposal value from SCM biz.

Take Solutions Ltd has informed BSE that in respect of the Issue, the Securities Issue Committee (the “Committee”) of the board of the Company at its meeting held at its meeting held on July 26, 2016, has inter alia passed the following resolutions:

-

Approved the closure of the Issue on July 26, 2016

-

Approved the issue price of Rs. 166.10 per Equity Share (share), [which is at a discount of Rs. 8.74 per Equity Share, to the Floor Price of Rs. 174.84 per Equity Share, for the Equity Shares to be allotted to eligible qualified institutional buyers in the Issue]; and

-

Approved and adopted the Placement Document (PD) dated July 26, 2016, in connection with the Issue

The Issue had opened on July 21, 2016.

Annual Report - 2016 : http://www.takesolutions.com/Reports_Filings/2015-16/take_solutions_annual-report_2016.pdf

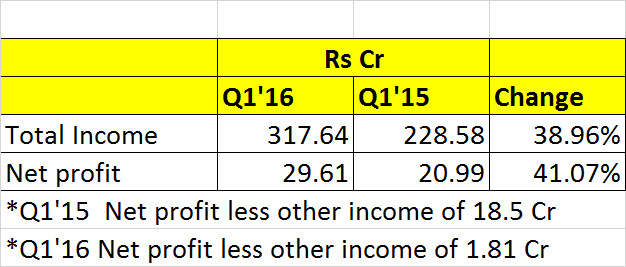

There was a bit of negative reaction, as soon as the results got released and it was unwarranted; what was perhaps missed at 1st glance was the other income of 18.5 cr in last year’s Q1. Once you take that off, it looks like a pretty good result.

4 Likes

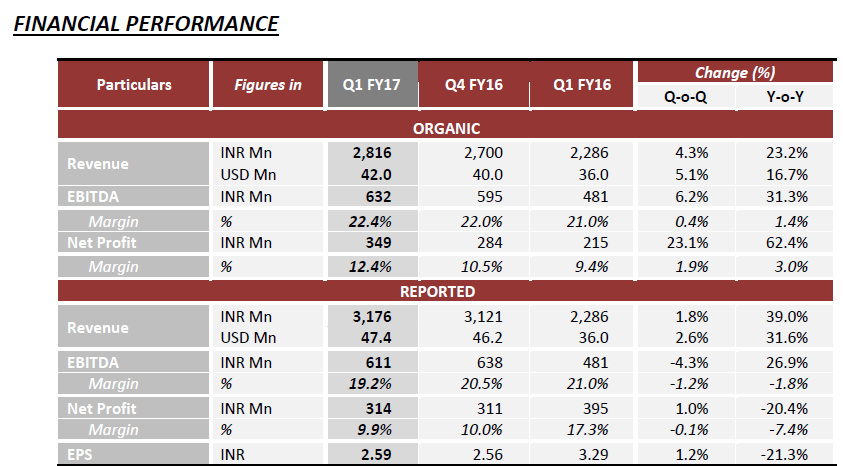

Quick Summary of my notes from Take Concall:

Take Organic Base Business(ex Ecron):

Revenues 281(this qtr) cr vs 228 - 23% yoy, 4.3% qoq

EBITDA 31% growth yoy, & 6.2% growth qoq

Ecron Acunova:

USFDA audit with zero observations

37cr (this qtr) vs 42 cr in q4 fy16. There is a general seasonality in this business. November - March heavy business. So H2 will be usually strong for this line of business.

37cr (this qtr) vs 27 cr in q1 fy16 - 40% growth in revenue terms

with -2cr EBITDA

Looking at 17% EBITDA margins for Ecron topline by FY17. Margin drivers will be lower cost.

Only adding scale will help in improving margins & profitability - we are investing aggressively here.

The following items impacted cost:

a. Closed 5 office in spain, malaysia, italy & czekoslovakia. European office locations are difficult to close. Hence a lot of one off costs.

b. 6 sales leaders joined the business. This is a very important investment.

c. H2 will be strong for Ecron. H1 will be soft for Ecron.

Client additions in small & medium pharma space

Marginal degrowth in SCM business - but was on expected lines

Revenue Distribution:

US - 81.2% Asia - 11.2% Europe - 7.6%

LSI - 77%, SCM - 19%

Looking at divesting SCM business. Working on opportunities to evaluate. Money that comes from exit of SCM business will go to grow to LSI business.

Debtors cycle just improved by 1 day to 98 days.

Take found a place in Gartner’s R&D report. Speaks of quality of business.

New Deals: We won a breakthrough deal in clinical data aggregation space with a large biopharma company.

We won a data analytics deal with a consumer facing company in US. A deal first of its kind for us.

New Offerings: End to end labelling solution for the industry. It is a massive challenge that the industry is facing & could be a large opportunity.

Orderbook: Order book grew by $5mn. The large deal we won(mentioned in March qtr) started from early July, will atleast add $2mn to q2. In q2&q3 we should have another large deal on bag. As of now orderbook is at $108mn vs $76mn in q1 fy15.

QIP for 180crores: A part of QIP will go to debt (80-100cr), next will go to capex and some of it will go for WC. Indian debt will go down.

Dollar denominated will stay on books (8mn LT, 20mn ST debt). This part will stay on books.

Thanks,

Ravi S

Invested, No buy/sell in the last many months.

10 Likes

Income adjustment should always be net of taxes. This 18.5 cr figure is one time income on sale of subsidiary. The rest are kind of part of biz income. I would remove 18 *(1-16%) for comparison. Even on that basis PAT is up close to 30% yoy. Good show overall.

Adjusted PAT comes to around 24.4cr in Q1 Fy15 vs. 31.4cr

Disc: invested

2 Likes