Came around to read the HDFC report and observed the below passage -

looked very familiar…

One might call it a coincidence, but probability of that is low IMHO.

Anyways, idea is not to boast but to take (pun intended) it as a compliment… ![]()

Came around to read the HDFC report and observed the below passage -

looked very familiar…

One might call it a coincidence, but probability of that is low IMHO.

Anyways, idea is not to boast but to take (pun intended) it as a compliment… ![]()

Mgmt gave another interview today on ET Now

Below link also has the video interview available.

Brief Highlights:

If i were paranoid, then the recent spate of interviews in quick succession gives me cause of worry. Is there an intent to spike up interest in order to have good participation in a possible QIP round?

Or, maybe they are wooing buyers for their SCM segment. Though that looks less likely as most of the interview focus is on LS and hardly any mention of SCM.

IMHO, i would rather the company consolidate and improve the operating cash flows rather than continue to embark on an acquisition spree.

@crazymama Where can I find out the details where management has mentioned that they would go for QIP?

Thanks.

It was one of the questions I had asked Take’s IR, Sachin Garg.

I had heard rumors from 2 sources which made me 2 ask the question in first place.

While he did not commit to a QIP, he did say mgmt is keeping their options open.

One could always call up Sachin and fact check.

This news about there involvement in state cricket league isn’t giving a very good feeling to me.

Anyone from TN follows this tournament, is it like a IPL ?

I think on a ballpark basis, buying a team would have cost around 4-5 cr. (not a small amount in Take’s context) and then maintaining it and the kind of mgmt. bandwidth these kind of things need is all unnecessary drain on scarce resources.

We are extremely pleased and excited that the reins of our team are in the highly capable hands. We are sure that a coach of his calibre will be invaluable in making Dindigul the toughest competitor in the tournament,” said HR Srinivasan, managing director of Take Solutions.

Also, TakeSol is not a B2C business which can leverage from these kind of branding activites. So am not sure what the mgmt is upto with this. Any ideas ?

This is not surprising given that they have associated themselves with various golf tournaments too

Resonating @crazymama thoughts - What worries me more is the frequency of interviews. I feel its overpromotional. Globally companies in this space have been on an acquisiton spree. I do hope that TS does not indulge too much into it.

I am also concerned about their margin. EA has lower margins than the SCM division. How they increase EA margin is yet to be seen.

Hello Raj,

I think it is par for the course given the longstanding association with Golf. They had a dedicated page in FY15 AR for their “Golf Initiative”. While it may have begun with humble intentions to promote the sport in our country, i think it is pretty popular now and one could further argue that it is mostly an inclination for the affluent.

Coming back to the cricket bit, found the below article which provides the exact purchase price.

TAKE Solutions (Rs. 3.42 crore) named Dindigul

While the base price for a franchise was Rs. 1.25 crore (per year), the lowest successful bid, by Chettinad Apparels Pvt. Ltd., fetched TNCA Rs. 3.3 crore.

As many as 22 tenders were purchased but only 17 actually bid for the franchises. In all, the TNCA got Rs. 33 crore — 3.3 times the minimum bid amount — from the exercise.

IMHO, there are 2 ways to look at it:

They find Golf too expensive to sponsor now and are moving towards Cricket which i think is relatively less expensive than say holding a Golf Tourney.

It is a dangerous precedent for us to be wary of given the past scenarios with DCHL.

With respect to the need for marketing being a B2B co., one could make a stretched argument that they are doing it promote their TALL Academy and trying to attract freshers. If that is indeed the case, then it is a convoluted way of going about it.

Either ways, another bogey to be added to the list of negative concerns about the management.

Honestly I wasn’t so bothered by their support for Golf. IMHO, in India there is lot money and support for Cricket at the cost of other sports. So a corporate making a case for supporting some sports other than cricket is acceptable to me. Even some small sponsorship for Cricket related things is also acceptable.

But Cricket on other hand, is a sports where the rich & mighty mostly fall over each other for sponsoring as it gives bragging rights like no other sports. We have all seen how badly some of the previous owners of such franchise have ended up.

I am in the camp to count it as negative on mgmt.

Disc: Holding

I too am not able to justify this move when there are talks of QIP for further investment in the business and plenty of debt sitting in BS.

Anyway, we are little more than a month away from the Q1 result and the conf call. Let us ask their rationale in the call.

Regards,

Raj

Disc: Holding. No transaction in last 30 days.

As per info I have, cricket investment is promoter’s personal. Take solution, the listed company has no connection with cricket.

Reg investment in cricket team: I spoke with Sachin Garg and he has confirmed that the investment is not from the listed Company. It is from Take Solutions Pte Limited (the parent that has a 57% holding in listed Company) but the media has got the name wrong. He confirmed that there will be no outlay from the listed Company on this account. You can independently verify - sachingarg@takesolutions.com

Also regarding goodwill, Accounting Standard only requires a Company to test it for impairment and not provide/write-off unless it has been established that it is impaired. Hence, I would not treat it too negatively. In-fact, they could just knock -off goodwill with equity and show high RoEs next year onwards but they are not doing that.

My 2 cents: IMO their spending on Golf is actually positive. Golf course is the place where you get to socialise CXOs, the decision makers. Most of the consulting and investment banking firms sponsor Golf events. One can certainly question why should Hero group spend on Golf

Even if the listed entity spends on street cricket through CSR funds, I will ok after it being disclosed appropriately and within limits.

A senior prodded me to take a look at Take Solutions.

Went thru this entire thread and was again amazed at the effort put in by folks like @rajpanda and @crazymama Vishnu to bring everyone on the same page. You guys truly live the VP spirit …thanks it makes it easy for anyone to get upto speed, quickly.

While I haven’t done any diligence, excuse me for pointing out that I don’t get a “good” feel for the future.

Positives:

Concerns:

It might have been okay for an Opportunistic bet at some earlier point. And many folks may be sitting on decent gains. I cant find much that gives comfort on a long term bet, however.

Good points.

Few points that make me think this is not an Opto Circuits:

Basically, the still photograph perspective (past financials) is untidy. But, that is the result of they being stuck in a commoditised business (SCM) and making investments in lifesciences which were not yielding full potential revenues. The unfolding movie perspective is that they are getting out of SCM and lifesciences opportunity is now playing out (25% organic growth guidance - capability corroborated by USD 12 mln recent contract win) - almost the inverse of the last few years. In these circumstances, selling out at 13x FY17 earnings does not seem appropriate.

Welcome counter opinion.

Thanks Donald for taking the time and giving a concise review.

Agree with ur assessment on most of the points.

On the other hand i also agree with Rohan with regards to the Opto Comparison.

I have taken the liberty to use the excellent thesis u had done on Opto way back in 2009, to clarify my point of view.

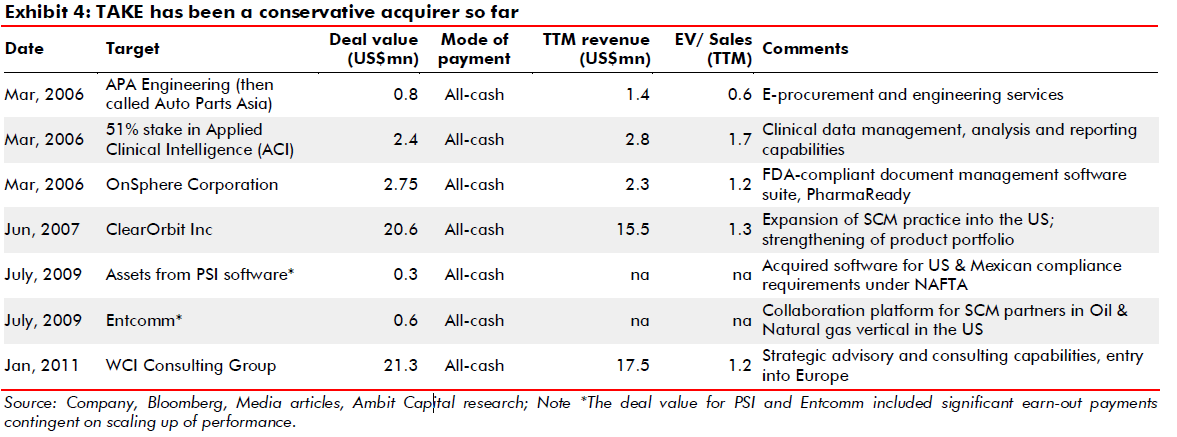

Unlike Opto, which had made acquisitions at far more higher valuations (in terms of EV/Sales), Take haven’t paid too high a price. Below is a snapshot from Ambit report.

While the big acquisitions made by Opto were higher-ticket sizes and some of them at higher valuations.

Opto has recently completed (April 2008) the $70 million acquisition of Criticre… reported revenues of $19.4 million in H1FY2008 with an OPM of around 10%.

But, the larger point of a poor record with the acquisitions is again debatable as one could argue that the lack of better numbers from the inorganic pathway is due to the low margin SCM segment which has far more subsidiaries than the life sciences, as well as the higher share of acquisitions.

PharmaReady was acquired through OnSphere (which I initially thought was homegrown). WCI has been mixed, while Applied Clinical was divested this year due to differences in opinion on future strategy.

It was only last year that all the subsidiary results were disclosed separately.

Applied Clinical had actually tripled their Net Profit.

Again, given the complicated capital structure and above average number of subsidiaries, it is difficult to say where the working capital is tied up/dragging on the OCF. Is it with the SCM or LS?

Having said all of the above, i had begun my investment 70:30 in favor of the mgmt (given the Shriram group pedigree). Now, i am pretty much neutral. While i don’t expect the business to go kaput in the next 6 months due to cash crunch/fraud (this is where i feel Shriram group acts as a natural check, as it impinges on their integrity as well), there is a good chance that the momentum in earnings from the last 3 quarters can continue.

I feel the divestment of the SCM will be a very good trigger as lot of the subsidiaries would be done away with and we could have a much cleaner balance sheet which is the biggest hurdle right now for anybody to do a full-fledged analysis, esp. a non-financial guy like me (Frankly, i get a headache every time i have made an attempt to read the 212 page subsidiary report)

To summarize, there are 2 tangible things which we can track in the next 2 quarters:

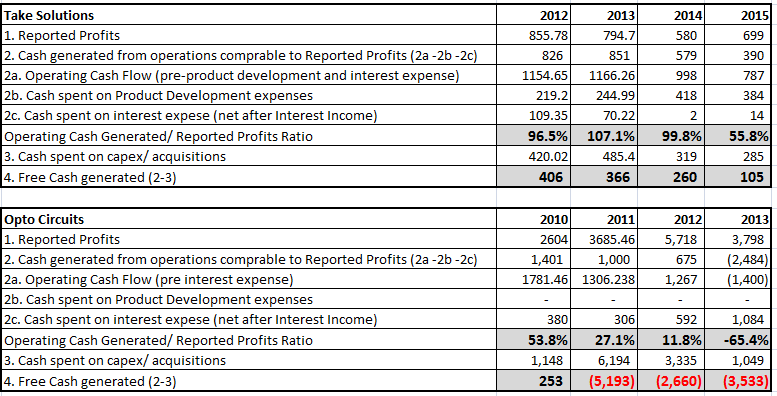

Just taking the argument forward, I have tried to explore similarities, if any between Take and Opto. For comparison, I have taken Financials of Take from 2012 to 2015 and the same for Opto from 2010 to 2013. Financials for Opto are taken before it was established that there are some issues (taking post that would be biased). Basically, there are two important metrics that point out a probability of fraud: the most important one being a very small conversion percentage over a long time of Reported Profits into comparable operating cash flows - this is the biggest indicator of reported profits just not being present. The same ratio for Take from 2012 to 2015 is 96.5%%, 107.1%, 99.8% and 55.8% - indicating that reported profits largely accrue to the Company as cash as well. On the other hand, the same for Opto from 2010 to 2013 was 53.8%, 27.1%, 11.8% and -65.4%. Now, this clearly indicates that profits are an accounting gimmick but do not really translate into cash flows. This ratio needs to be tracked for Take - if we see this coming down - well - it would be a deal-breaker.

Second indicator is capex or acquisitions being done well beyond the Balance Sheet and internal accrual capability of the Company. Basically, over a long cycle - if a Company can grow fast and not need any money for capex or acquisitions - great business which Take can be over time but is not currently; if a Company can grow fast and meet its money for capex or acquisitions through internal accruals - good business; if a Company can grow fast and meet its money for capex or acquisitions through manageable debt - ok business but need to track closely; if a Company can grow fast but needs to resort to heavy debt or heavy dilution to meet its money for capex or acquisitions - extremely risky business as when the funds dry out, the business dies as well.

Take in the last 4 years has had positive free cash generation each year. Look at Opto - heavy negative free cash for three out of 4 years. Mind you, Take’s 2016 numbers would be negative because of EA acquisition but we know that EA is a real Company with a reputed promoter and this should not be a fraudulent acquisition (like some fraud acquisitions used to deploy non-existent cash). However, if Take resorts to such acquisitions every year and shows numbers like Opto (big negative free cash), again - this would be a deal breaker.

INR mln

So, my conclusion is that let us monitor these numbers closely but this does not look like an Opto at this point of time.

![]() No need to defend.

No need to defend.

Please take my side-comment on Opto dejavu - in the context of Mgmt penchant for acquisitive growth and caution on what could go wrong - subsequently running out of bandwidth and depth in handling unrelated product/market competencies - that’s what I think was the real reason behind the downslide of Opto business - other aspects were manageable.

While it is good to focus on the emerging picture - obviously that is encouraging - else, you & me wont be wasting time here, I have learnt to step back - and consider very seriously What can go wrong. In the same vein if we are to rate Mgmt Quality, we have no option but to downgrade that based on the past record - there are no two opinions that past capital allocation decisions were sub par.

Yes, we can see things are getting better and hope things will be much better - but that’s hope - that’s not visibility. I like to temper HOPE with the RISKS that one can see in the business/investment thesis future.

Since there is an opportunity cost to every investment, I want to be convinced myself that the ODDS are stacked very heavily in my business favour. In Take Solution’s case I am clearly not convinced of that, at the high-level itself. So I wont bother to dig down further. But that’s my view. And different views make the market ![]()

My intention was only to draw attention to perceived average rating on Management Quality (I can be totally wrong), nothing else.

Thanks @Donald for stirring a good debate on this. I get following pointers to keep track of.

Cash Flows: Clarified in many posts that it is not as bad as it looks. I find that even working capital is ok. They are clearly past the stage of net cash (ex depreciation) injection in product development.

Balance sheet: Yes, a great deal of goodwill (170-180cr out of 255cr) has been accumulated during the last 2 yrs so we need to give sometime to execute. Their acquisitions have been small which are easier to turn around and indeed they are helping build capabilities.

SCM or enterprise solution is a hyper competitive business and needs scale. IBM and Accenture beat TCS/Infy so Take doesn’t stand a chance to build a large and sustainable business here. They are much better off to have niche stuff which can remain away from attacks by larger peers. We need to keep in mind that they started in 2000 itself so this is not a very old in IT industry. We could forgive any strategic mistakes if they finally find their destination. I think they have found their clarity and willing to exit SCM. Capital allocation is working as we need to keep in mind that Srini is SCM expert seems to be giving Ram free hand to build

Growth: I think this is the least of all concerns. Cherry on the top is that there is no competition on the horizon.

FY17 will remain another year of transition given their intention to exit SCM. Balance sheet and earnings will look much cleaner or steamlined but valuation may not be what we are seeing today.

Dear @Donald,

Disclosure first:) - I am one of your big fans for the kind of detailed analysis you do. I started following your footsteps and for some ideas I spend about a few months to develop conviction.

Ok now business -

Take is one stock which I follow very closely and I have spent about a year analyzing their business.

To your comment on RoE:

I have a feeling the way we look at numbers should be a lot different as numbers follow business execution and not the other way. We should ask questions about what led them to win a large $12mn order against the likes of big IT guys & pharma consulting folks and what is the likelihood that they will win future orders. If any one of these orders work out, your RoCE numbers will look different. There are a lot of soft aspects of this business which we have to dig deeper into.

If you look at a tree halfway through the growth and count the number of fruits it has yielded, you will be looking at a wrong #.

I have comments on your other concerns too, I will definitely detail it when time permits.

Both views make the market.

**And one humble request:**This below comment looked like a reco to my eyes and I did cross check my understanding with a couple of VPers - which we at VP dont do. This coming from a senior forum member wasn’t apt.

“It might have been okay for an Opportunistic bet at some earlier point. And many folks may be sitting on decent gains. I cant find much that gives comfort on a long term bet, however.”

Edited some portion above to take out reco part to ensure new visitors don’t get biased.

Apologize if any of my comments are not in the spirit of the forum.

Thanks,

Ravi S

Disc -Take forms a large portion of my portfolio. No trades in the last many months.