Take Solution Ltd(CMP Rs 46) - Dark Horse - A multibagger in making - Business recovery to strengthen from the coming quarter

Company background

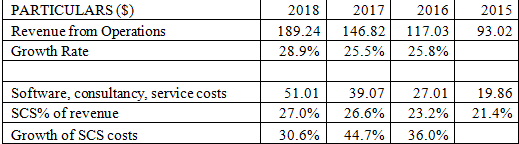

Take Solutions Ltd (NSE: TAKE & BSE:532890) offers domain-intensive and technology backed Life Science services with a unique combination of Clinical, Regulatory and Safety segments. The company derives 50% of its revenue from Clinical and remaining 50% from Regulatory & Pharmacovigilance (PV). The company’s clients include large and small innovator biopharmaceutical companies (approx. 90% of clients) as well as generics manufacturers (10%). According to geography-wise, 70-75% of the revenue is derived from US and 25-30% from Asia Pacific.

Investment Rationale:

1.) Liquidation & write-off in step-down EU subsidiary helped conserve cash: Navitas Life Sciences (subsidiary of Ecron Acunova Ltd) was bleeding cash on the back of events arising out of COVID-19. Management decided to liquidate the stepdown subsidiary in Q1FY21 and a loss of Rs 156.6 crore of net assets was written-off in Q1FY21. Also, closure of EU business helped the company in conserving cash and improving liquidity. Like for an example, loss in EU business was $2.3 mn in Q4FY20, which would have expanded to $7-8 mn in Q1FY21 and eventually would have turned into funding requirement in Q2FY21 if the management wouldn’t have liquidated the same.

2.) Exit of Supply Chain Management (SCM) business in Q1FY21 to focus completely on life-sciences business: The company sold its 58% stake in its subsidiary APA Engineering Pvt Ltd for Rs 17.4 crore in Q1FY21. As this would help the company to completely focus on its life sciences business portfolio.

3.) Sharp rationalizing employee costs to aid profitability: Management had reduced the employee headcount in western geographies where the wages were relatively higher for cost saving purposes. Also, many off-shoring initiatives were also taken up as a part of cost restructuring. In recent conference calls, management stated that the company had an employee cost run rate of $29 mn per quarter in pre-Covid times, it has come down to $18 mn in Q2FY21 and will further come down to $16 mn per quarter by Q3FY21 and then it will increase gradually as revenue expands in the life sciences portfolio.

4.) Reduction of debt to deleverage balance sheet augurs well: The management’s primary agenda is to reduce debt burden (approx. $71.9 mn as of Nov 2020) and improve cash flows through the combination of liquidation of Europe business, sale of stake in SCM business, headcount reduction, off-shoring of work and office footprint reduction. Management indicated that opening balance of debt in FY21 was $76 mn, of which the company has paid off $4.1 mn until Nov 2020. Also, rationalizations and restructurings have led to reduce employee expenses from approx. $29 mn to $18 mn and SGA expenses from $24 mn to $5 mn between pre-COVID to Q2FY21. Going ahead, one can expect management to sell off non-core assets (with minimal impact on revenue) to further reduce debt burden.The company had Monetized some real-estate to decrease the debt burden.

Going ahead, management has indicated that no further write-offs are expected and green shoots for business recovery would be visible from Q4FY21.

Conference call Q3FY21 highlights indicates business recovery to strengthen in the coming quarters

(i) Due to COVID in 1st quarter, capacity utilization had fallen to as low as 15-20% and clinical trials had come to a complete halt as patient recruitment had fallen by 95%. However, management has indicated that capacity utilization has now improved to 60% and RFP activity is now back to pre-COVID levels.

(ii) The rationalizations and restructurings in the business effectively mean that the normalized quarterly revenue run-rate has fallen to 60% of the original pre-COVID run-rate of Rs 600 crore per quarter. Therefore, at peak operating capacity, the company will do approximately Rs 360-370 crore of revenue per quarter.

(iii) The book-to-bill ratio which was deteriorated till the last quarter will gradually improve as activity returns to normal over the next 2-3 quarters.

(iv) 32 active trials are going on at the moment of which 25% is in Oncology, 19% in COVID and balance in CNS and Immunology.

(v) Current order book stands at $190 mn (vs. $280-290 mn in pre-COVID times) of which only $150 mn will be executable over the next 12 months. Management indicated orderbook at $220 mn for Q4FY21 which is approx. 16% growth QoQ basis.

Indicative Order Book Trend: $173 mn in Q1FY21, $185 mn in Q2FY21 and $190 in Q3FY21.

Financial Projections:

|

Revenue |

EBITDA |

EBITDA Margin |

PAT |

PAT Margin |

EPS |

P/E |

| FY19 |

2039 |

384 |

19% |

178 |

9% |

12.2 |

3.9 |

| FY20 |

2213 |

169 |

8% |

-10.9 |

0% |

-0.7 |

NA |

| FY21E |

895 |

-45.1 |

-5% |

-178 |

-20% |

-12.0 |

NA |

| FY22E |

1268 |

236 |

19% |

75 |

6% |

5.1 |

9.0 |

| FY23E |

1553 |

350 |

23% |

171 |

11% |

11.6 |

4.0 |

Valuation:

We feel that the worst is over for the company and improvement in numbers will be witnessed from Q4FY21. The stock currently trades at 4x FY23 EPS of Rs 11.6 which definitely appears bit undervalued.

From FY12-20, the cumulative sum of core operating cash flow stood at Rs 862 crore vs the current market cap of Rs 691 crore, indicating company generated strong cash flow but still current valuation does not factor in the numbers obvious reasons because of COVID-19 pandemic. Despite negative profits in FY20, operating cash flow remained the highest in last 8 years at Rs 170 crore. This indicates strong ability of cash generation. Also, cumulative Free cash flow from FY12-20 stood at Rs 187 crore.

Considering strong cash flow generation, management acting prudently in liquidating European subsidiary, selling off non-core SCM business and rationalizing costs through employee headcount reduction in order to reduce debt burden and improve cash flow in the near future.

A considerable multiple of 7x would give target price of Rs 81 per share (CMP Rs 46) (indicating 76% upside from current valuations).