EcronAcunova - Become marginally profit. Q3 and Q4 will see increase in margins.

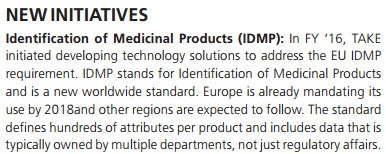

They see more significant opportunity for next 4-5 years in Identification of Medicinal Products (IDMP) standard rollout as FDA will shortly enforce this norm. IDMP provides a common, global framework for identifying medicinal products, creating full transparency between regulators, manufacturers, suppliers and distributors, and ultimately ensuring greater public safety. As such, any life sciences organization that intends to manufacture and/or market medicinal products within the European Union is required to comply.

Partnered with Sparta Systems. Got access to 250+ pharmaceutical clients. Plus 1500 prospective clients to be reached via this partnership.

FDA to implement Track and trace serialization .

Manufacturers have to be compliant with supply chain security act and they have time till end of 2017 for 1st phase. 2nd phase by 2020 and 3rd phase by 2022.

Clinical data integration and aggregation

101 mn. Order book compared with last year 60 mn. 10 new clients. PharmaReady. 21 new BioSimillars projects.

Roughly 750k came from large deal. Will double in next quarter. 12 million annually by FY18.

Margins will be impacted in next 2 – 3 qtrs by 2 to 3% due to one time consulting/advisory services and increase in sales force. Tripling of sales force will happen in next 12 months. Impact on revenue will be in seen in Q3/Q4 of FY18.

$96.4m. $76-77m LS H1 FY17. 54m H1 FY16

EA done 73 cr in H1. 28% higher. H2 will be even stronger seasonally.

Seeing good growth in US and Asia. Europe is flattish. Will not have any impact on revenues. Especially UK clients like GSK, no impact. Only 8% from Europe. 12-13% in Asia. 80% in US.

EA is only little over 10% of total business.

Expect some wins the 10m big deals pursuit in Q3.

Tax rate – 14% to 14.5% guidance for this year.

Plan for inorganic growth in next 2 years. But nothing on the table yet.

I guess you are referring to analyst meet and not AGM.

I have been tracking take since almost year now. I had met Ram and sachin and the scope of business and customer stickiness made me looked into the same.

The best part of the company is, it is not other company in IT space.

If the management is able to achieve the 2021 target and with EBITDA of 24-25%, I guess it can get a multiple of a pharma company and not IT company. (Anyway according to me it a substitute to pharma company)

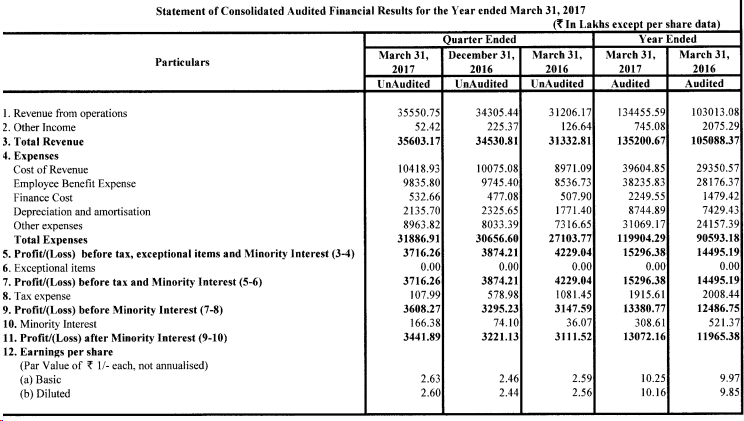

Revenue - Rs.343.1 Cr. YoY : 38.4% up. QoQ : 4.5% up

Net Profit - Rs.32.2 Cr YoY : 34.3% up . QoQ: -1.4% decline

6.6% life science growth QoQ. Marginal degrowth in SCM business

Enro Acunova - Rev 40Cr. QoQ 8.5% increase.

19% vs 18% ebita promised. This is inspite of $1.4mn strategic initiative expense.

H1B - We are not affected. Only 6 H1Bs of total 1600 employees. Those 6 are of delivery people - Consulting & Technology people. US - Momentum is good. Manpower. Local hires in US.- Citizens or GC. Nobody from 7 banned countries.

Extent of offshoring - 30% to 35%. Best case 50%.

Order book $129 mn - Main: 116.4Cr (EA share would be 20Cr) + SCM: 13 13% groth QoQ.

Significant deals in Europe and US.

Management additions - Current CFO Shobana moving to US. New CFO - Subhasri Sriram (Ex CFO Shriram City Union Finance). Sales addition in US to accelerate revenue trajectory.

CFO change - Part of operations changes. So important Shobana to be in US as she was part of it from beginning.

In India - Subhasri - well known face in the industry.

IDMP - Eurpean medical agency. Impacts whole industry, every pharma company.

Track & Trace - US centric. End of 2017 for manufacterers. Wholesale / retailers - 2022.

Apart from this there large opportunities in Bio similars, clinical etc

Large deal going smooth. Already few delivery happened.

SCM sale: Possibility of part stake sale before Q4 end. Another part by 2017 end.

Middle East(??) part of business - No propects yet.

Pipeline: 1 large deal - We may hear decision in couple of days. Another 2 larger deals.

FY18 - Organic growth - 23-25% forecast. EBITA margin - once strategic initiative expense over, there will be 2% increase in.

Will be improvement in Europe business in few quarters.

Strategic initiative for redefining the business. : To be completed by FY18 Q2. Total 31 crores.

Nature of costs. 1. Cost of consulting engagement 2. Cost of agencies 3. Capacity cost (Bench cost before they become hunters.)

Ecron Acunova - Focus is to move them from T&M base to Technology base for margin expansion. Takes time.

Vishnu bhai - Your ability to connect the dots is amazing (as to what path TSL was probably going to take post EA acquisition). Though, i am not exactly clear as to how TSL is planning to use EA’s assets to their advantage; they are giving contradictory signals. There can be two paths-

Boosting EA’s CRO offering (clinical trials segment) by developing Data Analytics capabilities (No CTMS?Risk-based monitoring?) and integrating with their regulatory offerings, which they said they will do in your call with Take IR

Just focusing on integration of EA forte (biosimilars, stem cells therapy, imaging) to their existing Regulatory software.

In Q1 2017 concall they said -

Regarding office closures… may be Take already has presence there and they don’t want redundancy? To improve sales, they are scaling their sales team.

In Q4 2016 concall, mgmt said -

Excerpt from one of Mr. Srinivasan’s interviews (June 2016) -

So, this is the directional change? Development of support for regulatory filings for biosimilars, imaging and stem cell therapy? What is the progress made here in last 3 qtrs? How is EA helping them here (knowledge-base probably?)? When will they attain full functionality?

Some questions/observations -

a. [quote=“crazymama, post:67, topic:2709”]

Say, if you are a Big Pharma co. and u have a choice to select a vendor for doing a clinical trial between -1. CRO like Quintiles2. CRO using Medidata platform3. TSL + CRO (with no CTMS or Analytical Platform)It most likely ends up between options 1 or 2.

If Navitas+EA follow the Quintiles template, then they could take it to the next level given the complimentary capabilities they bring together, the low-cost pricing by having trials in India, and hopefully much more conducive regulatory environment.

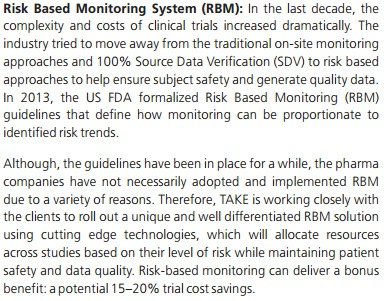

What are the gaps for the future?- RBM: Risk Based Monitoring which requires emphasis on real-time data for drug safety during and post clinical trials. RBM Infographic a better approach to risk based monitoring.pdf (105.2 KB)- EDC + EHR/EMR: Patient focus to help create data repositories for faster and more efficient recruitment (This is a differentiating factor for Quintiles to win customers confidence)

[/quote]

So TSL, even with Ecron present, doesn’t have good CTMS and Analytics platform at the moment. Whenever next acquisition happens, it should probably be to plug this gap? i.e. on the clinical trial execution/analytics side. As EA previously was using CTMS from some other vendors?

b. They have started publishing result of subsidiaries separately, but i see the results of foreign subsidiaries have been audited by the same Chennai auditor. Isn’t that odd? What are the rules here in case of foreign subsidiaries?

c. Ecron margins are still struggling, even little less than what they originally were just post acquisition? How are they going to improve here?

What does this mean? I understand such strategic acquisitions takes time integrating into the overall culture of the acquirer, but still it has been around 5-6 qtrs since this acquisition. EA topline has slightly improved from 130 to 160 odd cr…so not much here!

d. Mgmt in Q4 2016 concall said - [quote=“crazymama, post:106, topic:2709”]

Rollout of unique clinical data aggregation platform. Further plans to build new solutions on top of this platform such as Risk-based monitoring applications.

[/quote]

An exceprt from 2015-16 Annual Report

Any development on this front? What’s the opportunity size here? Quintiles already offers this feature.

e. Contribution from Europe is still not increasing is a big negative. Mgmt in last concall said it would take another 2 qtrs and said they have cracked significant deals in US and Europe. Any info about what the deal size here is?

f. How much working capital is tied up with SCM division. Were they not able to generate free cash flow due to SCM division (unlikely), or it was due to s/w development costs and acquisitions in LS division. Development cost is going to remain high in future as well, and so is amortization? Why don’t companies like Take add s/w development cost to the expenses rather than capitalizing it? It’s going to impact PAT either way. Is this to keep EBIDTA higher? or there is any other reason?

g. [quote=“whipsaw, post:196, topic:2709”]

Pipeline: 1 large deal - We may hear decision in couple of days. Another 2 larger deals.

[/quote]

Any insight on the size? What is actually helping them win these large orders now? What has changed now? Are these deals coming from existing clients, or these are new client additions?

h. [quote=“whipsaw, post:196, topic:2709”]

Strategic initiative for redefining the business. : To be completed by FY18 Q2. Total 31 crores. Nature of costs. 1. Cost of consulting engagement 2. Cost of agencies 3. Capacity cost (Bench cost before they become hunters.)

[/quote]

What are these costs for? For Europe expansion, or to merge Ecron properly, or generic to give direction to the overall business? For instance "Capacity cost (bench strength) isn’t a one time cost, but is recurring, so why say this is one time expense?

i. In another interview in June 2016, mgmt said - [quote=“crazymama, post:134, topic:2709”]

Brief Highlights:

Ecron Acunova for the year we should expect to do business of about Rs 160 crores vis-a-vis about Rs 130 crores for the previous FY.

But over the next two to three quarters, I think we should see a strong uptick in the margins of Ecron Acunova as well.

Update on IDMP: This product is based on a particular legislative requirement in the European Union. It is called the IDMP or identification of medicinal product. So it is a regulatory requirement and we hope that we will be launching this product later this month.

[/quote]

They stated this as well in the Annual Report (2016) regarding IDMP development.

They succeeded on point 1, failed on point 2, what is the status on point 3 i.e. IDMP product launch? Has any of Take’s competitors already developed IDMP solution?

j. Goodwill is ~250 cr, (big % of net worth). Does it need to be amortized? What is the usual way IT companies deal with it (keep it forever)? I have gone through a recent concall where mgmt said this is usual industry practice. What i am trying to find out is if it is going to impact bottomline at some point in time and does market discount that. Or can the company keep this as such forever unless this is impaired? How about knocking off goodwill against security premium account/general reserve, which seem to be the best way for shareholders?

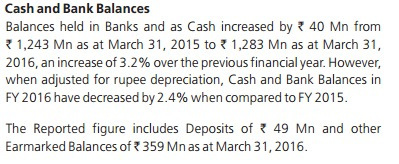

k. There cash and cash eq. shows a big number (in excess of 125 cr, but investments show a meager 17cr. This is odd. If there is no immediate use of cash (they said they want to remain liquid for sudden future acquisitions opportunity), why aren’t they putting this cash in some better yielding asset class?

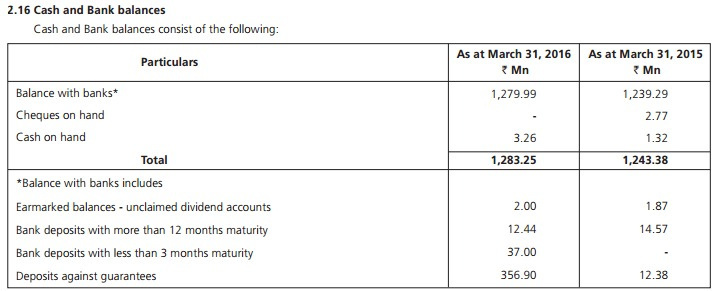

From Annual Report (2016),

INR Depreciation is hurting them on Forex front.

Also, in 2016 Annual report, they are counting “Deposits against Guarantees” as Cash eq… Is this the normal practice? Also, where does remaining cash reside i.e. which bank, a/c, country? This is extremely important info for us to believe this cash is for real! -

l. Mr. Srinivasan doesn’t draw any salary from the company? Is he taking salary from any of the subsidiaries? I know he is holding major stake in the holding company in Singapore. But why doesn’t he draw salary directly from Take?

Overall i think the stock has not given any returns in the past 2 years, but it is much-much better placed in terms of performance and balance sheet than it was 2 years back.

Much better TTM topline ~1300 cr …against ~730 cr in March 2015,

Much better TTM bottomline ~127 cr …against ~70 cr in March 2015,

Long term debt has been retired at the cost of around 9% equity dilution (i will take it, more so as dilution happened after 8 years),

working capital debt is at very low rate (USD Libor + 2%), which i think is around 4-5% total,

getting into bigger league with large order wins and a much better order book visibility (~129 mn) - double of march 2015…roughly ~55-60 mn),

improved debt/equity

QIP (in which marquee investors/PE funds like Apax Partners, NT asset mgmt, Sundaram MF and Max NY Life etc. participated) took place at 166. Stock currently trading at 136.

Peak P/E 5 qtr back was ~23-24, which now is 14. Peak market cap was 2450 cr at that time, which now is 1800cr. EV/EBIDTA at that time ~13, which now is ~7.

Stock after a big rally from sub 40 levels to 200 is consolidating, which is normal after such breakthrough rally. Fundamentals have significantly improved, while valuation (mkt cap) remains stagnant (from March 2015), which makes me believe this is clear case of undervaluation (becomes big time undervaluation considering growth prospects for next 5 years).

TSL to me currently looks like at an inflection point due to the following -

SCM division divestment materializing in 2017 end (topline will take a hit due to this which is a negative obviously),

Bigger opportunities opening up in form of eCTD/Track and Trace (what’s the opportunity size?),

Ecron acquisition to reap benefits gradually,

Biosimilar filings (as their major revenue is coming from innovators, not generics),

Sparta partnership (How exactly this will contribute as Sparta being into QMS?),

Subsidiary structure improvement (how many will be gone with SCM?), as you said earlier, will be much cleaner post SCM sale,

Margin improvement,

tripling of sales force,

Management getting more cash to deploy from SCM division sale (any estimates on the value of their SCM division at the moment?) for another good acquisition in Life Sciences space, if an opportunity presents itself at some point in future. Whole industry is consolidating and competitors are ramping up their capabilities.

Assuming bottom end i.e. 20% CAGR organic growth (mgmt are confident of 20-25% CAGR for next few years), they can attain close to 2700 cr topline in 4 years i.e. March 2021. They are growing their topline at more than 30% in last 2 years. Any acquisition in between, and they can topple this number.

What i see from the recent interviews is that TSL is transforming itself from a mere software company in healthcare domain to a knowledge based (consulting) company with its own software solution. They are trying to package their consulting services along with their internally developed software solutions in pharma space. EA Acquisition was all about scaling quickly in the domain EA was in (Biosimilars, Imaging, Stem Cell) and their Human capital.

Some good points from the recent interview -

How has synergy with Ecron impacted Take?

Ecron’s FY16 revenues were 116 crore. This year, they crossed ₹105 crore in 9 months. To build revenue synergies, I have to apply my sales capacity, products and solutions I have and give a consolidated offering to an EA customer. This year, EA will see 30% organic growth, much higher than its earlier growth rate.

On SCM

Has 3 parts - one is 100% owned by us. Two are co-owned by partners. We are trying to find the right value. In the next couple of months, we should have something that translates to value. Two-thirds of our supply chain business may be sold.

You acquired Ecron Acunova last year. Any gaps in your offering that you would still like to fill?

Organic growth will be the larger part of our journey. When you buttress that with M&A, it makes capital sweat better. Ecron got us new capability in biosimilars, a booming area. They had done 10 new studies. It is easy for them to get the eleventh. Reaching $500 million is very transformative. We have seen companies stagnate before they reach this milestone.We don’t want to overestimate our capabilities. If we want to run faster, we need a coach – which muscles to develop, how to develop stamina…

We can now sense the direction Take is eyeing i.e they are seeing big opportunity in Clinical Trial Outsourcing (CTO) segment, which has been discussed here on the thread time and again. Important thing to note is that these clinical trials occur over a very long period (8-10 years), prior to regulatory submissions.

Earlier, Take was confined to a very small segment of the whole life sciences pie (Regulatory submissions). Now, with their acquisition and molding of Ecron, they are targeting this new lucrative and lengthiest segment in medicine discovery i.e. CTO.

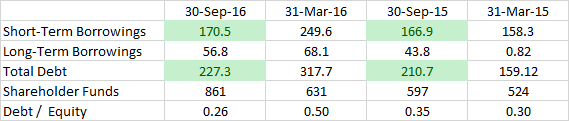

Guys - need your help in understanding the debt for Take Solutions. The FY17 (6 M) balance sheet shows reduction in both short-term and long-term borrowings and D/E has come down to 0.26 i.e. 50% improvement in just 6 months (assuming QIP funds used to retire debt)

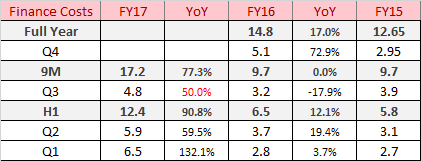

But if I look at Finance costs in the P/L for FY17 - finance costs have almost doubled in 9M YoY comparison. And every quarter Q1 (assuming they retired debt in Q2 so this Q1 number may be fine) , Q2, Q3 the finance costs have been much higher YoY - I really don’t understand the divergence in these numbers.

With all the talk of retiring debt from QIP funds and manageable $ debt (assuming lower rate of interest) - how are the finance costs higher every quarter YoY?

It might be better to compare QoQ interest cost in this case. Interest cost of Q1FY17 was 6.49cr, it reduced to 5.91cr in Q2 and 4.77cr in Q3.

Remember that Take increased its Debt a lot last year for an acquisition and most of the finance cost increases took place in second half of FY16 which carried themselves to FY17

@sachit - Have updated my post with a bit more information on debt level from past 3 years. Your point about looking at the numbers QoQ does make sense except for Q3 numbers. As of 30-Sep-16 and 30-Sep-15, the debt of the company is extremely similar but there is still a 50% increase in Finance costs in Q3 FY17. Now I’m not sure if this is a one-off where a potential repayment was made ahead of schedule or some anomaly like that. I’m basically trying to build a case for increasing my PF exposure in Take but any management recourse to debt is a big turn-off and finance costs are eating into profit margins. So I’m trying to understand when long-term borrowings will again come back to zero like FY15.

I think Take bought Ecron Acunova in November 2015, so probably some debt (50-100 crores or so) was taken in Q3 of FY16 the impact of which was felt in Q4 of FY16 and Q1 of FY17. That’s why finance cost increased from 3.25 crores to 5.08 crores (from Q3FY16 to Q4FY16). Then maybe they have periodically started winding it down the debt. That’s why September 2015 debt was 210, which jumped to 317 in March 16 and then fell to 227 crores in September 16. Not totally clear though.

I was thinking of asking this question for a long time. Are there any new negatives that has surfaced for Take in past 2-3 months (except aggressive accounting)? Reason I am asking is that the stock is declining in a bull market so trying to understand if I am missing anything that market knows.

I will take a look at qtrly numbers closely. What i know is that their debt is dollar denoimanted, so forex fluctuations can impact that.

@fundoo - Mukul , The news flow is positive. Recent mgmt interviews are insightful. No negative triggers other than INR appreciation. Please read my long post above where i have listed all the positives at the current valuation.

This has been one frustrating experience holding the stock for the last one year. No amount of earnings or attractive growth plans seem to make investors interested. Some pain points that I observed recently.

FIIs and DIIs were not happy with frequent equity raise. The recent one happened despite enough space for debt.

They said many big contracts lined up but what they got except one is underwhelming. No investor update on biding of these contracts.

They wanted to wrap up sale of SCM div. which did not happen by Q4 as promised. They should refrain from giving any timeline on this.

Self inflicted wound in form of engagement of consulting firm which keeps margin recovery postponed.

Overall bearish undertone regarding IT earnings. Take gets bunched up wrongly there.

Now Rs appreciation will hurt margins in the short term while repricing should help recover later.

Take so far :

300+ successful drug launches. 200 innovative + 100 generic.

40+ clients on pharmcovigilance

2000+ consulting engagements

320+ clinical studies

1000+ bio-available / bio-equivalent studies

Audited by 25 different federal agencies globally include FDA in current FY. Zero observations.

LS grew by 39% in this FY

Profit of 130.7cr (vs 119cr. 18cr addl income)

EA - 50 Cr rev in Q4. EBITA margin 16% compared to 9% previous qtr.

Full year EA rev 167 cr vs 115 cr YoY.

Order book stands at 144 mn end of Q4 (87.3% LS and 12.7% SCM). Up from 103 mn yoy.

Added 9 new clients this qtr. 2 mid-size clients ( 1 multi country and 1 Germany) in EU with deal size of 10 mn. spread out 2 years. 1 was the deal that was mentioned in last concall. 1 is new. Going fwd seasonality will come down as all new deals are bundled with EA also.

2 senior hires. Krishnan Rajagopalan - US. Chief Growth Officer. Michael Garber - Sales.

Need to hire leaders in clinical space.

Expecting surge in Orders and pricing.

FY18 rev outlook - 20-22% organic growth.

Strategic initiative (Pinnacle) expenses - Total 31 crs. So far spent 13.1 crs. May not spend all.

SCM - Its been frustrating so far. On documentation stage. Expect 1 to get over in Q1. 1/3rd will be sold. Not entire.

SCM proceeds to go into working capital.

Not in a hurry to pay USD debt.

Tax - 15%

Currently 200 mn USD company. Expecting to grow to 500 mn by 2021.

Jump in receivable days - Because of billing happened in the end of march, it has pushed up receivables. it will get back to normal from next qtr onward.(may be below 100 days)

Was anything around overall debt discussed? I’m still very curious on how the Finance costs for FY17 are up 50% YoY when the Balance sheet shows a significant reduction in debt both at 6M FY17 and full year FY17.

These folks are not presenting true margin picture. Look at the balance sheet details -

70% of assets(~400cr) are actually illiquids like goodwill, intangible etc. I think being a services company it is prudent to expense their spend on developing new consulting framework etc. They are unable to dispose off SCM biz which suggests that there is no ready buyer of those products. If it is true, we have to brace ourselves for impairments in FY18. They claim that they make low double digit EBITDA margin in SCM and if we expense product development expenses they hardly make any money. I suspect that’s why they are unable to sell. They are repeatedly showing rosy picture about revenue growth and 25% EBITDA margin in life sciences biz. I think they should disclose expected EBIT margin which is the practice followed by IT majors.

Hi Sumit,

I take your point on the balancesheet. They have a lot of intangibles on their books. This includes a substantial amount of 235 crores as goodwill. But on your point of software and product development expenditure I have a different point of you.

I was approaching this problem from a balance sheet point of view taking cue from your point and found that when you compare Net Block (including tangibles and intangibles) of FY16 and FY17 - the figure has moved from 542 crores to 554 crores only - this implies to me that whatever they are spending on incremental software expenditure is rapidly also being expensed off in the P&L. This is verified by the increase in the sum of Depreciation and amortisation figure in FY17 to 74 crores to 87 crores.

No comments about SCM as I don’t track it closely. Working capital also has deteriorated which will be a key monitorable as the management has said something about bumper billings in March.