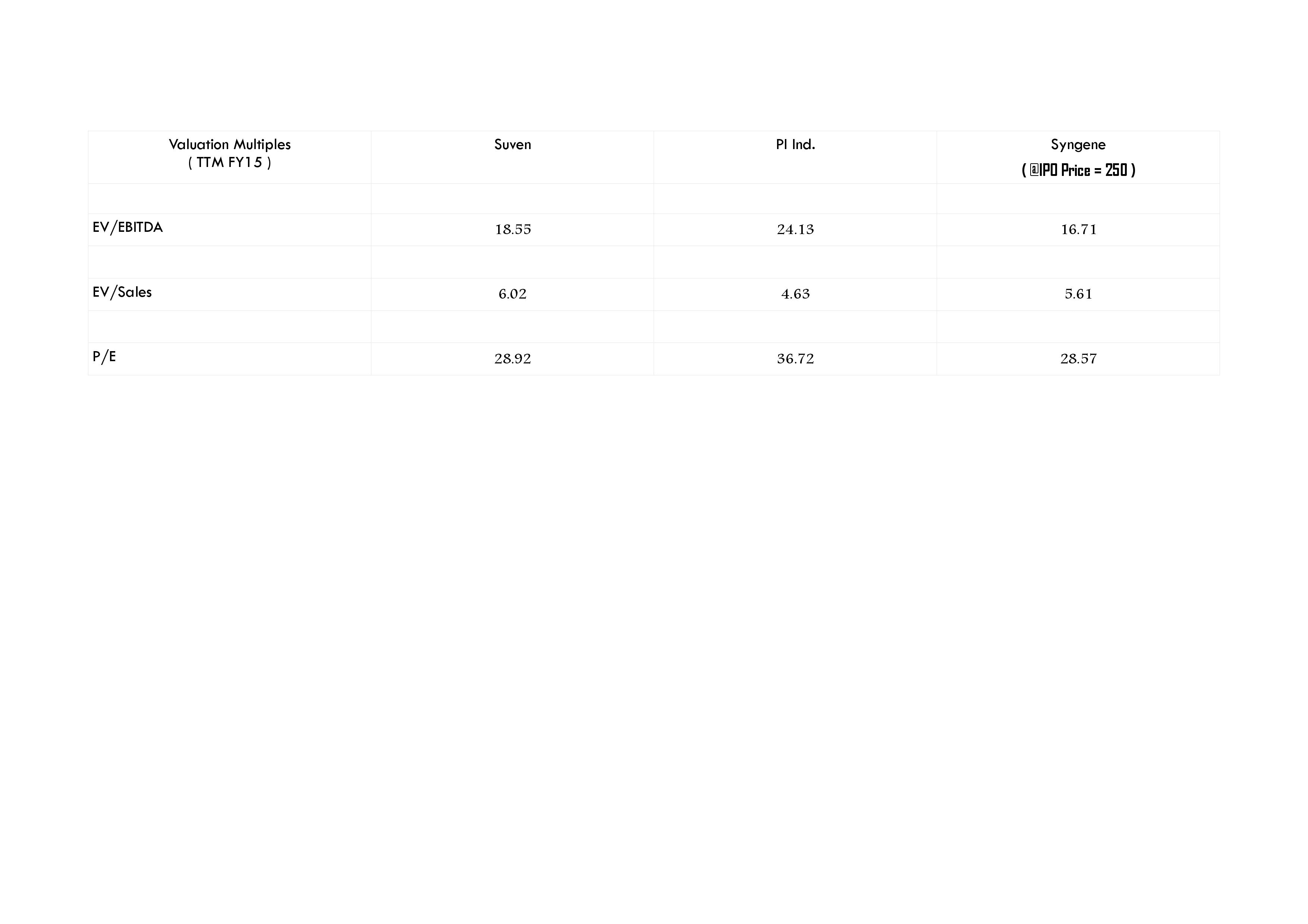

35 pe is expensive by any yardstick is my assessment for a capital eating business with roe of 20 …can learned boarders clarify what does syngene has that suven or granules or even pi does not have ? equity is 200 crs 20 cr shares of Rs.10 each

@manishinlucknow

Thats because in that effect of bonus issue is not included which was issued in March’2015 whereas in DRHP you have BS upto Dec.2014 only…Its advisable to refer final RHP.

@whipsaw

Have not studied in detail history of wuxi so can’t comment on that.

@reacher

As said before also, “beauty lies in the the eyes of beholder” and whether Syngene is expensive or cheap at 250 or 300 or 350 is for the individual to assess based on his/her analysis…It could be expensive and it could be not… but one thing is sure, its an interesting study and after a long time we have good paper like this getting introduced to the market…even RHP’s detail study is important where many hidden things are important to note like almost 7x increase in advances from customers, almost doubling of hedges in FY15 which are usually done in anticipation of future business, etc. Also, while assigning valuation to any stock it is best to look at varied parameters rather than only one specific parameter like P/E as valuation is based on future financials and not past financials.

Suven & Granules have completely different business models…whereas Granules is almost completely focussed on off-patent generic business with it already being very strong is paracetamol & ibuprofen ; Suven serves innovators much like Syngene but has focus on development of its own NME too so that it can outlicense it in future…Also, it has CNS focus…PI’s CSM bsuiness caters to majorly agrochemicals sector where regulatory issues are not that relatively high as also it is involved with the innovator from process research stage and not discovery stage…Each of these companies have their own strengths and weaknesses so has Syngene.

But, since PI & Suven also serve innovators, so it will be interesting to note valuation multiples assigned to them by the market…

2 Likes

Good analysis. no wonder GMP for it is touching 47-49.

Mahesh what r the moat for Syngene and are they sufficient to ensure it becomes a stress free investment for next 3-5 years ala Proff Sanjay Bakshi ??

@Mahesh Nice post.

One point from RHP which caught my attention:

For fiscal 2012, 2013 and 2014 and the nine months ended December 31, 2014, 44.0%, 37.8%, 33.6% and 32.2%, respectively, of our revenue from the sale of services was derived from our largest client, Bristol-Myers Squibb Co.

Discl.: Interested, not invested.

@Vivek_6954

The only major risk factors I can see in Syngene are like Regulatory issues, Client Concentration, management of CAPEX, Sustenance of high EBITDA margins, second lowest YoY revenue growth registered in FY15 (15.88 %) post FY11 (14.35 %), lowest OCF conversion registered in FY15, low taxes paid consistently, possibility of no dividend payment, poor wealth creation track-record of its parent, etc…

Now out of these risk factors, I see real biggest risk factor being CAPEX management as all other risk factors are either external which are common for all companies in the sector, or one off like low OCF due to huge hedge cover taken in FY15…(even low taxes paid is almost similar to its peers)…other risk factors although valid, but I see them slightly thinking far-fetched like sustenance of high EBITDA margins, second lowest YoY Revenue growth in FY15, poor wealth creation track-record of parent, etc. because we have the past 14 years history to see like even at 0.60 asset turn it worked at 30 % margins and after a historically lowest FY11 growth of 14.35 %, it rebounded in all subsequent years to post 25 % + growth each year till FY14…

So, stress-free or stressful that is for an individual to decide for his/her bearable-stress-level, but I see in Syngene ethical promoters which enjoy great credibility in market, industry as well as government circles not only nationally but internationally, a sound business model with good industry prospects and above all the positioning of the company in the industry with it being the largest player in India and now progressing to serve entire lifecycle of an NME…one particular thing would like to mention here --that I was quite impressed with the way Biocon management transparently handled Syngene issue, FY15 results were posted beforehand and even Q1FY16 results of Syngene were declared before opening of the issue (hidden in Biocon) so investors were with complete clarity before going into the issue…

@chintans

Yes client concentration is high and that will remain as I don’t expect top 3 clients contribution going below 40-45 % in near future.

2 Likes

The client concentration risk is mitigated to great extent by the stickiness of client (hopefully) with Syngene throughout discovery and clinical trials of a molecule. Also, for the top client, I read there is a contract till 2020 (which would mostly be extended) and Syngene has a dedicated facility for this client.

@Mahesh Since I am newbie to the market, I am trying to understand what could be the reason for IPO now of all times, especially since the funds raised go to parent. Could it be that Biocon needs funds, or value unlocking for promoters as you explained above?

My main concerns are bit similar to yours - not much wealth creation (till now) in parent & no experience in manufacturing for molecules post launch phase. There are 2 dimensions to the last point:

- Is management able to do capex and keep ROCE high? D/E of 0.23 gives some solace.

- As far as I understood, Syngene would keep working exclusively with innovator during discovery and clinical trial phases for a molecule, so long as the molecule goes to next stage. Why would the innovator continue working/(exclusively) with Syngene post commercial launch?

The main bullish point for me apart ofcourse from the CRO industry growth, is also related to the last point above - namely great visibility of revenues from pipeline of discovery and clinical trials (this could give more visibility than a CRM player like Suvens). I am also trying to understand how the discovery pipeline can be used to forecast the expected revenues from clinical trials few years down the line.

On a slightly tangential note, drug discovery is one field where algorithms will be used a lot more over coming years; though I don’t see any reason why this would hurt CRO industry.

@chintans

Biocon needs funds for its own business and for that it decided to go for IPO of Syngene rather than going for debt as Biocon management is slightly conservative as afar as leveraging goes…value unlocking for promoters could only come from the demerger of Syngene which seems quite away and I will not be surprised if it comes once Biocon shareholding reaches below 55-60 % in Syngene.

Rgdg. your two dimensions…

(1) As I said before, key is how well Syngene manages CAPEX and its resultant financials…with the business generating average more than 50 % of EBITDA as CFO and blended EBITDA margins post CMO unlikely to go below 27-28 %, managing order-backed CAPEX should not be a problem for the company unless it commits a blunder…

Also, management’s conservative attitude towards raising too much debt with a clear cut guidance in analyst meet as well as media interviews that in Syngene D/E will never go above 0.5 gives a great amount of comfort to me as an investor.

(2) In NME, protection of confidential data, IP, is of utmost importance…so, when you have a partner who has very well assisted you in discovery and development, if that partner also has commercial scale manufacturing facilities, you will definitely prefer to go with it for commercial launch…second thing, in the initial stage of commercial launch, say first 4-6 years, an innovator prefers to work with only two or maximum three suppliers so as to minimise compromising on confidentiality…innovator expects and works closely with these two or three suppliers for building dedicated capacity in return of assured minimum off take…

8 Likes

Motilal Oswal Initiating Coverage Report on Syngene (11th August 2015) – Target Rs. 350.

We recommend a BUY on Syngene International with a target of INR 350- valuing the company at 25x FY 17E EPS Unique CRO play: Syngene, subsidiary of Biocon, is a contract research organisations (CRO) with 2000+ scientists working for 16 of the top -20 global innovators. Syngene offers integrated discovery and development services to over 211 clients globally (103 in CY12) in pharma, biotech, agrochemical and other industries. Long-standing relationships with customers have been a key strength. Some of its strategic collaborations are with Bristol - Myers Squibb, Baxter, Endo Pharmaceuticals (pharma), and Abbott Nutrition.

Business diversification to drive value growth:

The company has shifted from CRO to contract manufacturing (CMO) of novel molecules. Six of its partners’ molecules are in advanced stages of clinical development (five in phase-3, one has completed phase-3). It has signed a commercial supply pact for three of these molecules with a large innovative player. More importantly, its partner has already filed an NDA with the USFDA for commercial launch for one of these three molecules a year ago.

Well positioned to leverage from growth in global pharma R&D outsourcing trend :

Global pharmaceutical players are facing structural issues such as profit pressures arising from impending patent cliff, drying product pipeline and rising R&D costs. Surprisingly, however, the new product approvals from the USFDA are on the rise. Hence, these players are inclined to outsource some of the R&D budget to CROs like Syngene. Outsourcing allows clients to convert a portion of their R&D budgets from a fixed to a variable cost, giving them greater flexibility to shift strategic and development priorities in response to market conditions. According to Frost & Sullivan estimates, R&D spend in the global pharma space was ~US$139 billion in 2014 whereas the CRO pie was ~US$44 billion (32%).

Valuations & View:

We recommend buying Syngene post the listing for a target price of INR 350 per share. We value the company at 25x FY17E EPS at a premium to its only comparable peer in Asia. Wuxi Pharmatech (the only comparable peer in Asia) is valued at ~20x FY17E EPS. However, Syngene has superior financials compared to Wuxi with FY15 margin of 33.0% (vs. Wuxi’s 22.3%), ROCE of 21% (vs 10.5%) and ROE of 20.7% (vs 15.2). The novel drug CMO opportunity, could result in earnings surprise to our estimates in FY17. Further, as there are no other listed players in bio-pharm CRAMS space, we believe Syngene will command a scarcity premium.MOST_Syngene_IC_11082015.pdf (86.3 KB)

1 Like

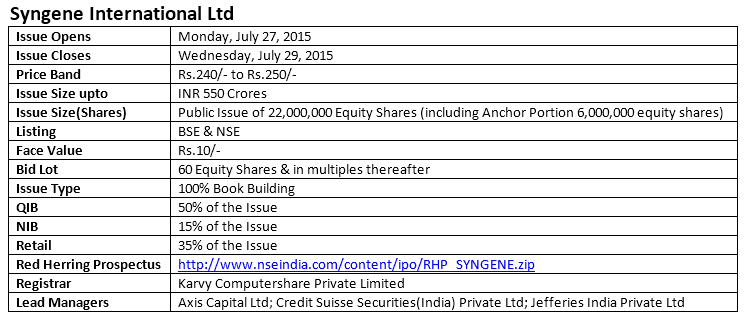

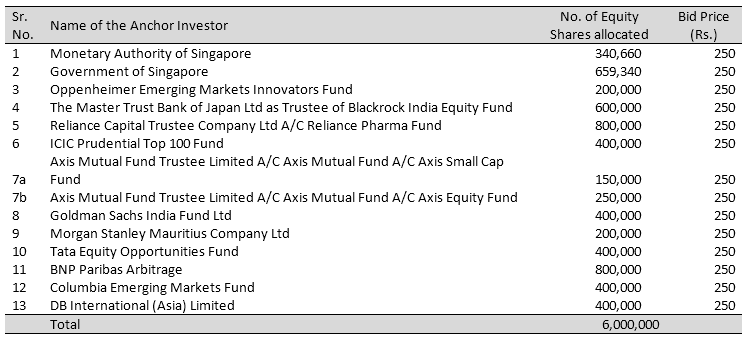

Details of the IPO and anchor investors.

Syngene International Limited

NSE SYNGENE (Series EQ)

Blg SYNG IN

ISIN INE398R01022

Issue Price Rs. 250/- per share

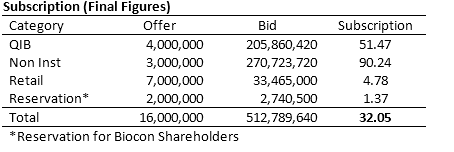

Syngene International IPO - QIB 51.47x | Non Inst 90.24x | Retail 4.78x| Biocon Shareholders 1.37x |Overall 32.05x (Final)

Company Description

Syngene International Ltd (SIL) is one of the leading India-based contract research organizations (CRO), offering a suite of integrated, end-to-end discovery and development services for novel molecular entities (NMEs) across industrial sectors. It offers service in discovery and development cover multiple domains across small molecules, large molecules, antibody-drug conjugates (ADC) and oligonucleotides. The integrated discovery and development platforms help organisations conduct discovery (from hit to candidate selection), development (including pre-clinical and clinical studies, analytical and bio-analytical evaluation, formulation development and stability studies) and pilot manufacturing (scale-up, pre-clinical and clinical supplies) under one roof.

The company was incorporated in 1993 and is headquartered in Bengaluru, India. It is a subsidiary of Biocon Limited (Biocon), a global biopharmaceutical enterprise focused on delivering affordable formulations and compounds. SIL is now forward integrating into commercial-scale manufacturing of NMEs

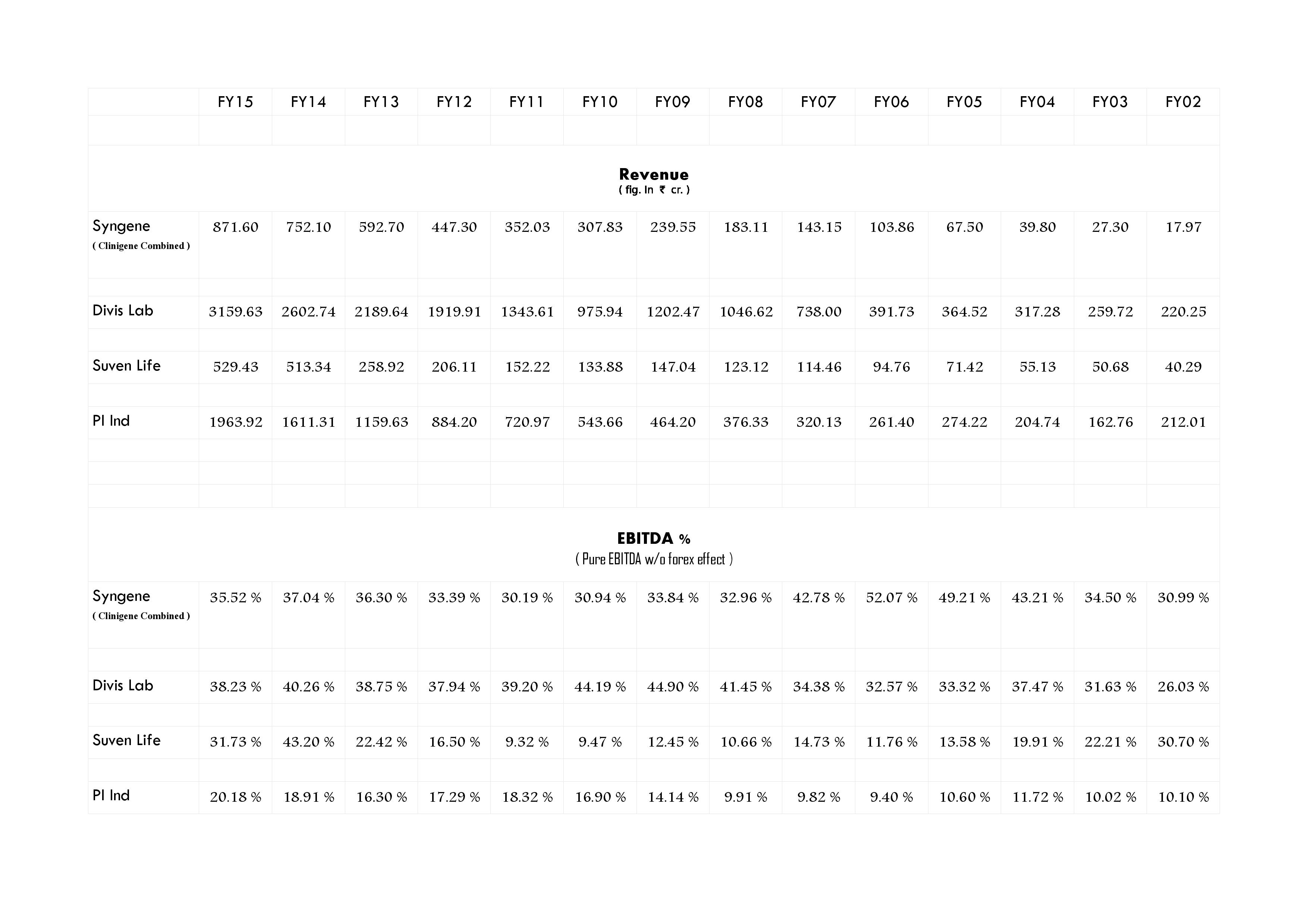

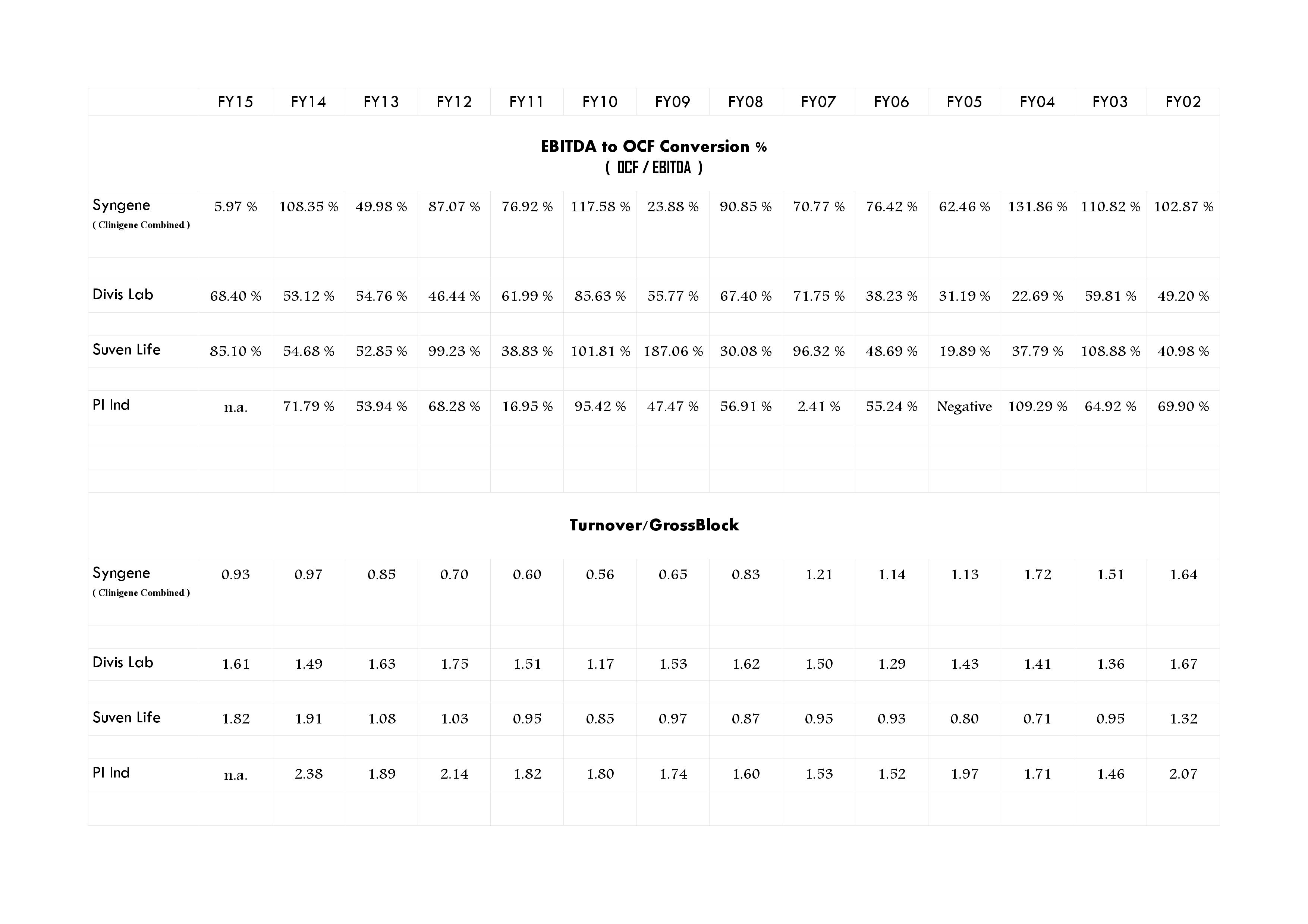

Had got few queries regarding comparison of Syngene with Suven & PI…have already explained earlier in this thread that the business models of Suven, PI and for that matter Divis are different than that of Syngene except one common fact that all companies focus on innovator MNCs (with Divis having presence in generics too). Since atleast this one factor is common, did a comparison on varied parameters of all the four companies for as much historical data I can get – 14 years :

As can be seen from the above, only Divis is as consistent as Syngene…Some things need to be noted from above :

(1) EBITDA to OCF conversion % for Syngene is above 50 % for 12 of the past 14 years which augurs very well for the management of CAPEX going ahead.

(2) Turnover/GB is lowest in case of Syngene which signifies scope for improvement.

(3) Alongside Syngene, only Divis has registered consistently high EBITDA margins.

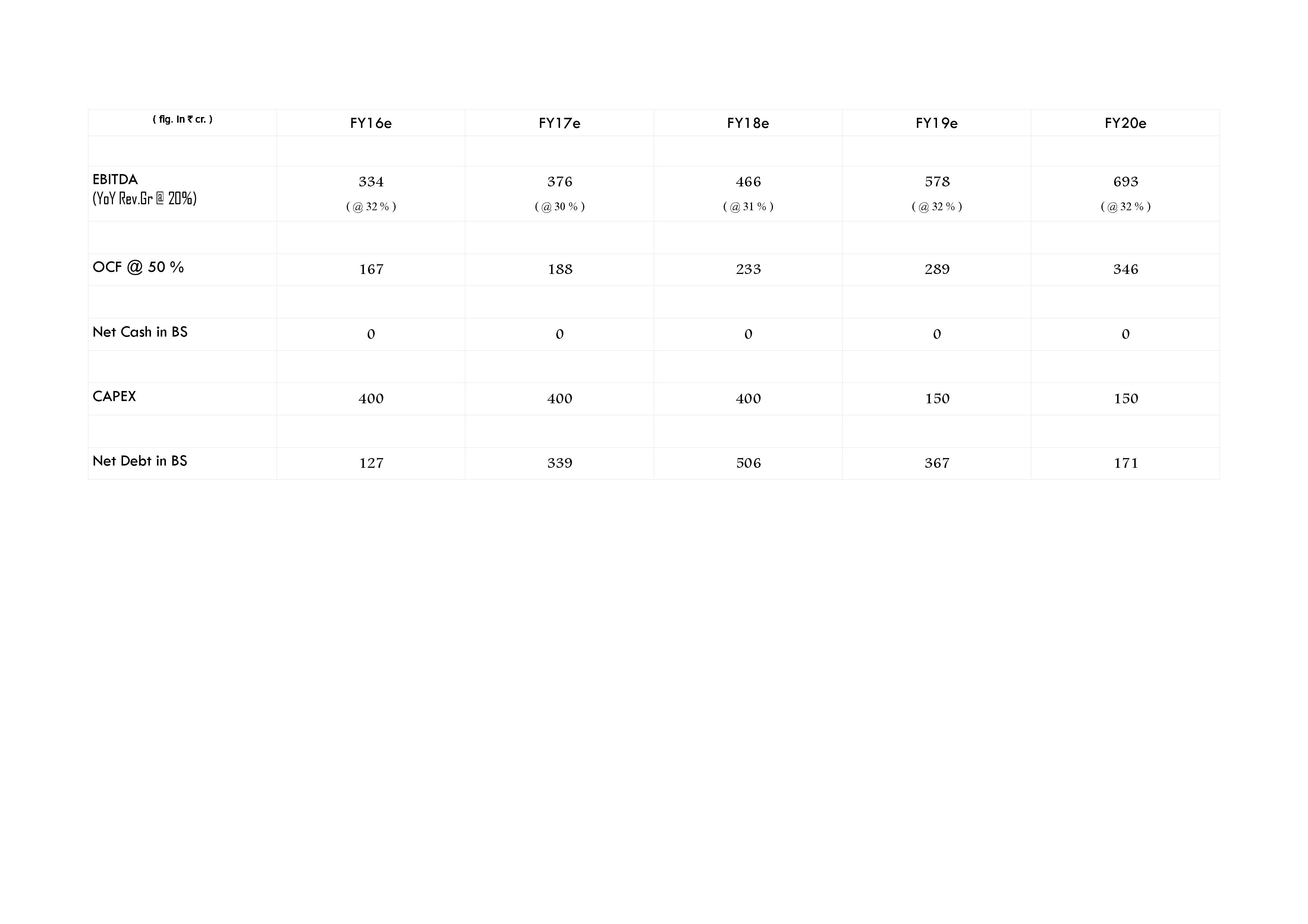

From the historical data we have, as also future CAPEX that is known, I tried to plot a rough possible future BS scenario for Syngene to assess the effect of 1200 cr. CAPEX over next 3 years…

It is worthwhile to note here that in an interview to ETNOW, management today guided for taking debt only if CAPEX is to be incurred immediately on the back of orders ; otherwise, management sounded confident of meeting staggered CAPEX requirement from internal accruals only…it reiterated that at no point company will go beyond 0.5 D/E…

Also, we have assumed here low EBITDA margins in the range of 30-32 % v/s MOST IC report estimate of 34 %…even in today’s interview management was confident of maintaining 30 % + EBITDA margins even after starting of CRAMS.

We have assumed here only 20 % YoY revenue growth each year for the next 5 years.

CFO (OCF) is assumed at flat 50 % of EBITDA each year v/s past 3 Years’ average of 54.76 %, past 5 Years’ average of 65.65 %, past 10 Years’ average of 70.78 % and past 14 Years’ average of 79.70 %.

0 % equity dilution is assumed over next 5 years as otherwise on just 10 % equity dilution, company can garner half of the CAPEX = 600 cr. at a price of Rs. 300 per share.

These are just assumptions based on the history which I devised before investing into the company and there are varied parameters which can go wrong. I just reproduced my calculation here for members’ benefit.

Discl. - Invested.

Note - This is not a Buy/Sell/Hold recommendation of any kind and is part of a general discussion.

8 Likes

Thanks a lot for your detailed analysis Mahesh. It helped me a lot to understand this company in a better way.

I went through its DRHP doc and have some questions on that… would be great if you/others can throw some light on that to understand it better:

It’s mentioned that, as on March 31,2015 they had around 2685 employees and out of which 258 are PHD’s and 1665 are Masters(degree in Science). Out of 1665, 400 employees are dedicated to BM R&D Center…

And during last fiscal, they serviced 221 clients. Since company works like a R&D center for clients where dedicated employees are required, I was wondering how company is able to manage less than 6 resources per client(for remaining ones)

However, I completely agree that it has got a great potential to grow in future.

I understand that, Quintiles also works in the same domain. Any inputs on sourcing the brokerage reports/industry reports to understand Syngene in better way would be of great help.

Thanks

Disc: Invested… 1% of portfolio. waiting for some correction to add more

Out of total employee strength of 2664, 2129 are scientists out of which 253 are PhDs…so total scientist count is 2129 and not 1665…secondly if I check the revenue per scientist figure of scientists dedicated to top 3 clients and of others, although revenue from a scientist of top3 client is higher than that of others but difference is logical as in case of top3 you have a dedicated clear roadmap whereas in case of others, company is also doing project-based work so utilisation will vary each year…also you need to understand one thing that the huge clientle that you see is in a sense building of a prospective inventory as there are two benefits to it – first NME research is also associated with failures so it could very well happen that tomorrow some small company which is working on a NME might discover a blockbuster product so you need to be present with them also — secondly, relationship building and therefore trust building is the most crucial pillar and infact the most long gestation investment of this industry and company seems to be very well aware of that…

Regarding industry reports you can very well find many on CROs but I feel you should try exploring past 14-15 years ARs of Syngene and its peers (especially Indian ones) as it will be a very good study. In that you will not only be able to understand industry and company evolution better but also you will be able to study varied financial and other parameters in detail.

Rgds.

Discl.- Invested and still Accumulating as on date.

Would request all investors interested in Syngene to visit its revamped website http://www.syngeneintl.com/

In investors section one will also find latest AR15 plus Q1FY16 results…must say its a great IR displayed by the company as have not seen many companies which not only before the IPO but also immediately post IPO follow such a transparent IR practices.

Rgds.

You can upload it here. Others will also benefit from the same. I have gone through the DRHP, FY15 AR & the Investor Presentation. Trying to understand about the industry as much as i can

@karu_lamborghi_

Please find attached Syngene ARs from FY07 to FY14…before FY07 one can refer Biocon ARs.

ar07.pdf (252.8 KB) ar11.pdf (522.5 KB) ar08-1.pdf (732.0 KB) ar14.pdf (431.0 KB) ar13.pdf (411.1 KB) ar07-1.pdf (1.0 MB) ar10-1.pdf (1.0 MB) ar12.pdf (370.5 KB) ar10.pdf (301.9 KB) ar09-1.pdf (578.8 KB) ar09.pdf (84.9 KB) ar08.pdf (206.6 KB)

Please find attached Clinigene ARs from FY07 to FY14…before FY07 one can refer Biocon ARs.

ar07.pdf (157.2 KB) ar13.pdf (336.3 KB) ar09.pdf (473.0 KB) ar07-1.pdf (860.0 KB) ar08.pdf (566.9 KB) ar14.pdf (331.3 KB) ar12.pdf (309.5 KB) ar11.pdf (494.0 KB) ar10.pdf (280.8 KB) ar10-1.pdf (40.4 KB) ar08-1.pdf (148.7 KB)

Rgds.

14 Likes

Mahesh, thanks a lot clarification.My bad, it should be 2129 not 1665.

I thought, if the company puts more number of scientists into other clients, they would feel confident about its r&d capabilities.Hence i felt it number of employees dedicated to each client was very less. Thanks for AR’s and for direction. I will go through them to understand it better.

Prashant…Not only till FY07 but also go beyond till FY02 which you will find attached in Biocon ARs…If you want to go still further then refer IPO prospectus of Biocon filed in 2004 where you will find data till 1999…Its a real treat to study the company :

14 Years’ Average Pure EBITDA margin (excluding forex effect) of 37.35 %…

10 Years’ Average Pure EBITDA margin (excluding forex effect) of 36.50 %…

Post initial low scale (less than 100 cr.) high margin (43 % +) phase, once company went into 30s in EBITDA margins over last 8 years, average pure EBITDA margin (excluding forex effect) is at 33.77 %…

EBITDA’s conversion to Net Cash Generated from Operations has been robust at 14 Years’ average of 79.70 %, 10 Years’ average of 70.78 % and 5 Years’ average at 65.66 %…

Not only that but even EBITDA’s conversion to Free Cash Flows (FCF) is excellent with 5 out of 14 years showing negative FCF with 9 Years’ average positive EBITDA to FCF conversion at 50.72 %

If we go further to look at health of balance sheet over last 14 years, with a Gross Block addition of 920.19 cr., we have a cash surplus of ~106 cr. in the balance sheet.

Now this is the kind of investment opportunities which a long term investor loves to invest…we have a great history in front of us and with the management confident of continuing with this historical parameters of 30 % + margins, promise of low D/E of not more than 0.5 and an investment plan of 1200 cr. over next 3 years —and this too from a management which exhibits great investor friendliness – an example – you have balance sheet published each quarter instead of half yearly requirement…

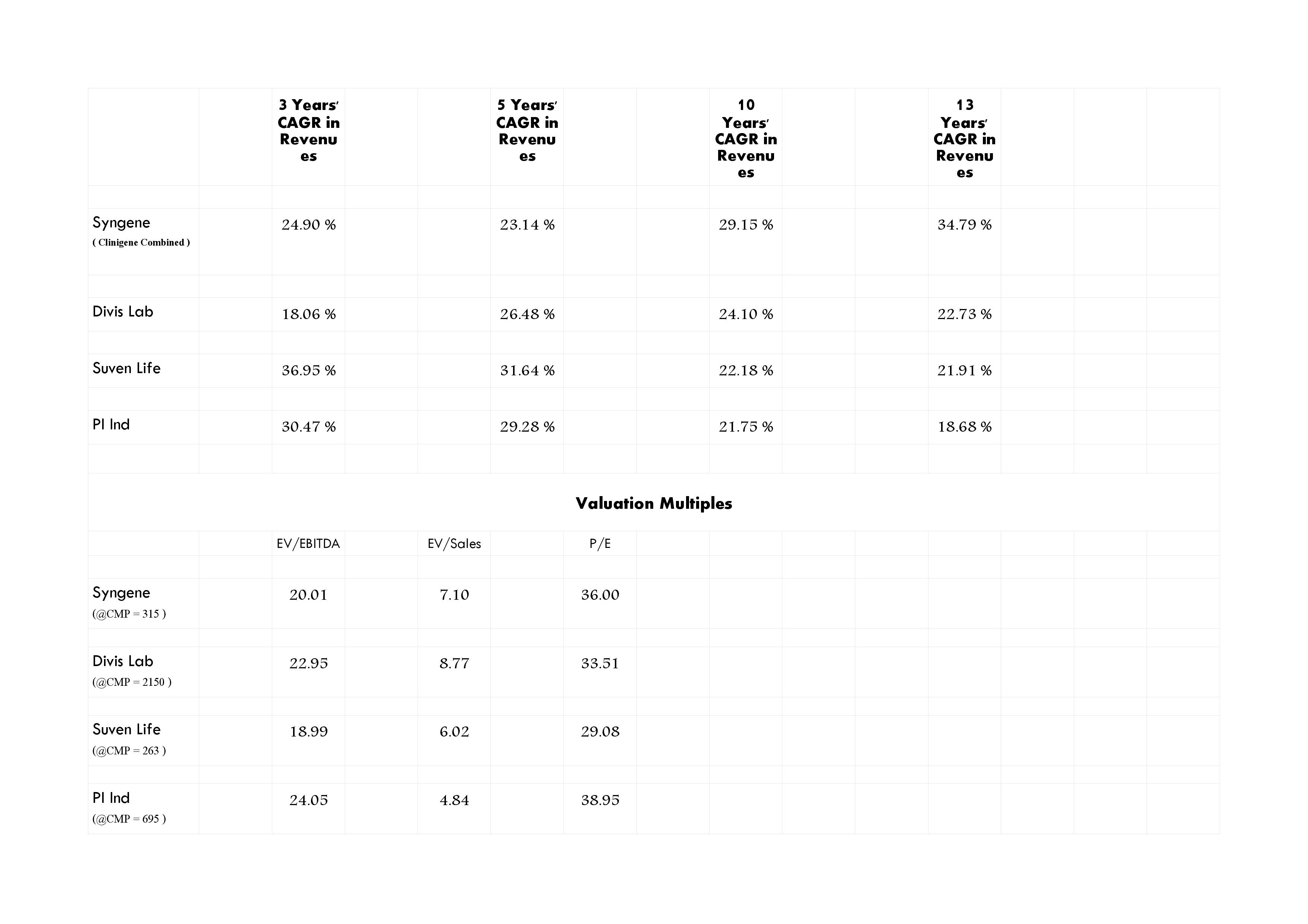

When I summed up all and looked at the future with just sustenance of 28 % + EBITDA margins, 50 % + EBITDA to OCF conversion, Asset Turn of just 1.1 post stabilisation of CAPEX and derisked business model because of focus on only NMEs, I fail to understand why this stock is still trading at discount to PI Ind. and Divis Lab on EV/EBITDA basis…Over next few quarters I expect majority of shares getting into the hands of pure long term funds and not remaining much with public category as with a free float of only 12.2 % equity capital or 2.44 cr. equity shares, at current market price of 320, only half the amount invested by funds in parent Biocon, can absorb the entire free float of Syngene…study of history of PI Ind as well as Divis Lab is a perfect case study for this as I remember once fund interest picked up, public category shrinked from ~11 % to 7-8 % with a simultaneous rerating in PI ; similarly in Divis, once fund interest picked up, public category shrinked from ~20 % to ~6 % with a simultaneous rerating.

Let’s keep our fingers crossed and hope the anomaly gets corrected soon by Mr. Market.

Rgds.

Discl. - Invested.

Note – This is not a buy/sell/hold recommendation and is just part of a general discussion.

7 Likes

Mahesh, as usual your research is super.

I think Syngene being involved right from the starting stages of a molecule i.e., Innovation is what makes market think twice on according high valuations. At least until it sees consistency and sustainability or the impact on revenues will no longer depend on molecule innovation.

Contrast this with other high quality CRAMS Players where the costs of R&D, innovation is the onus of MNCs while the Indian companies happily end up bulk manufacturing them with the cost advantages that Indian companies have.

Not invested in Syngene.

Also, I’m not convinced about Ms. Kiran Mazumdar Shaw’s management ability and who after her will run the show - I have not researched enough though. Please throw more light on this aspect of management capabilities.

Thank you so much.

That’s the strength and main attraction towards Syngene…catering to the entire lifecycle of an NME…it is far superior to any high quality CrAMS players of India…it builds an extra amount of trust and rarely you will find an innovator moving towards any other CRAMS player than Syngene if it’s involved with NME from the beginning…Three dedicated centres that you see are the result of the same…I think you are misunderstanding the business model…onus here also is on innovator in case of failure…it is almost identical to PI business model wherein PI is involved with an NCE at process research stage and in case of NCE’s failure, contract provides for take-or-pay…similarly in case of Syngene, in case of failure there is minimum guarantee fee amount payable by the innovator which covers almost the entire cost or is to be compensated by another NME from the same innovator…

Syngene is a services company in a way and not innovator that you need to understand…Question arises asto then why an innovator gets involved with Syngene ??? …The cost of research is rising tremendously every passing year so is the percentage of failure…so innovators are constantly looking at ways to cut cost of research…and if they get a reliable partner which can offer confidentiality, quality and reliability at say 70 % of the cost that they would otherwise have to incur, they immediately go ahead with it,Syngene has this advantage…

Lifecycle of an NME is quite long till commercialisation and it is the history of Syngene that is now working in its favour…similar to the way PI reaped benefits of its 10 year long investments starting 2010, PI seems to be at a similar stage…three of the molecules where it was involved since the beginning have reached commercialisation stage and ~6-8 % of the total molecules it is working on are in later stages of their lifecycle close to commercialisation…the 1200 cr. investments that you see over next three years are because of this…almost the entire investment will be backed by firm contracts similar to PI which incurs CAPEX only based on firm contracts…

Kiran M Shaw is not directly involved in Syngene and her intention seems to be to ultimately de merge Syngene after extracting maximum cash from it for Biocon and then eventually pass it on to a professional management or PE backed structure…Biocon is her dream project…as far as her management ability goes, one thing I am assured of is her credibility…the credibility she enjoys in the industry as well as government circles, she might not do anything to ruin that…its a very clear and transparent management…otherwise who will bother to announce IPO band before 10 days of opening of issue…who will declare not only Annual figures but also Q1 numbers before opening of issue…who will immediately after listing post Annual Report 2015 as well Q1FY16 results and q1FY16 Balance Sheet on the website…all this point to great corporate governance…

When we have past 14-16 years of history for all of us to see…when we have not only industry players but also company’s employees talking very respectfully for the company…when we have industry itself likely to grow in double digits in foreseeable future…its like not believing and finding something ugly which is not there…although such practice is great on most of the occasions but is not right on all occasions…I see no problem in management…what many are seeing is history of Biocon but parallely no one is seeing the history of Syngene…Syngene is now an independent company and now it might find its own valuation multiples in the marketplace.

Rgds.

11 Likes

@Mahesh : Thanks for your wonderful analysis… I maybe novice in this topic but how do you evaluate the business vis-a-vis Suven Lifesciences in the value chain? Overall I find suven extremely attractive …

PS: Also whats ur take on MPS at current valuations? Seems Market has hammered the company in the absence of any incremental news

Regards

Sreekanth

1 Like