the classy way you put it, I liked it. I think with Venkats hardwork and their team they will do something by 2017. Suven can be a multibagger

yet another patent news

PS - sold a minor qty tdy in the run up

What made you sell could you share whats fair value in your view where you will be comfortable buying back - i ask this since you have v good understaing of this co and have been holding it for a while i think

@reacher the later part of your statement (holding for a while) is true. I am not a great assessor of fair value. One observation of mine is that - on days, when the patent news is released, the stock jumps up a bit, only to give it up later. Also, Venkat Jasti had often clarified that there is no real monetary value to these patents, unless they find a buyer. I did not fully capitalize on the previous ride between 330 and 200 and my current behavior is to avoid the same the 2nd time; I am expecting a few flat quarters, I think, one more revisit of the lower levels is not ruled out, although often I have been proved wrong in the past, in my assessment !! so, take it with a pinch of salt. The real move up is when Suven is able to find a buyer and lock in some real royalty for one of those molecules in advanced stages of trial runs. I find that timeframe is some time away.

PS - Disclosure given above

2 Likes

yet another patent news…stock is up…

http://www.bseindia.com/corporates/ann.aspx?scrip=530239&dur=A&expandable=0

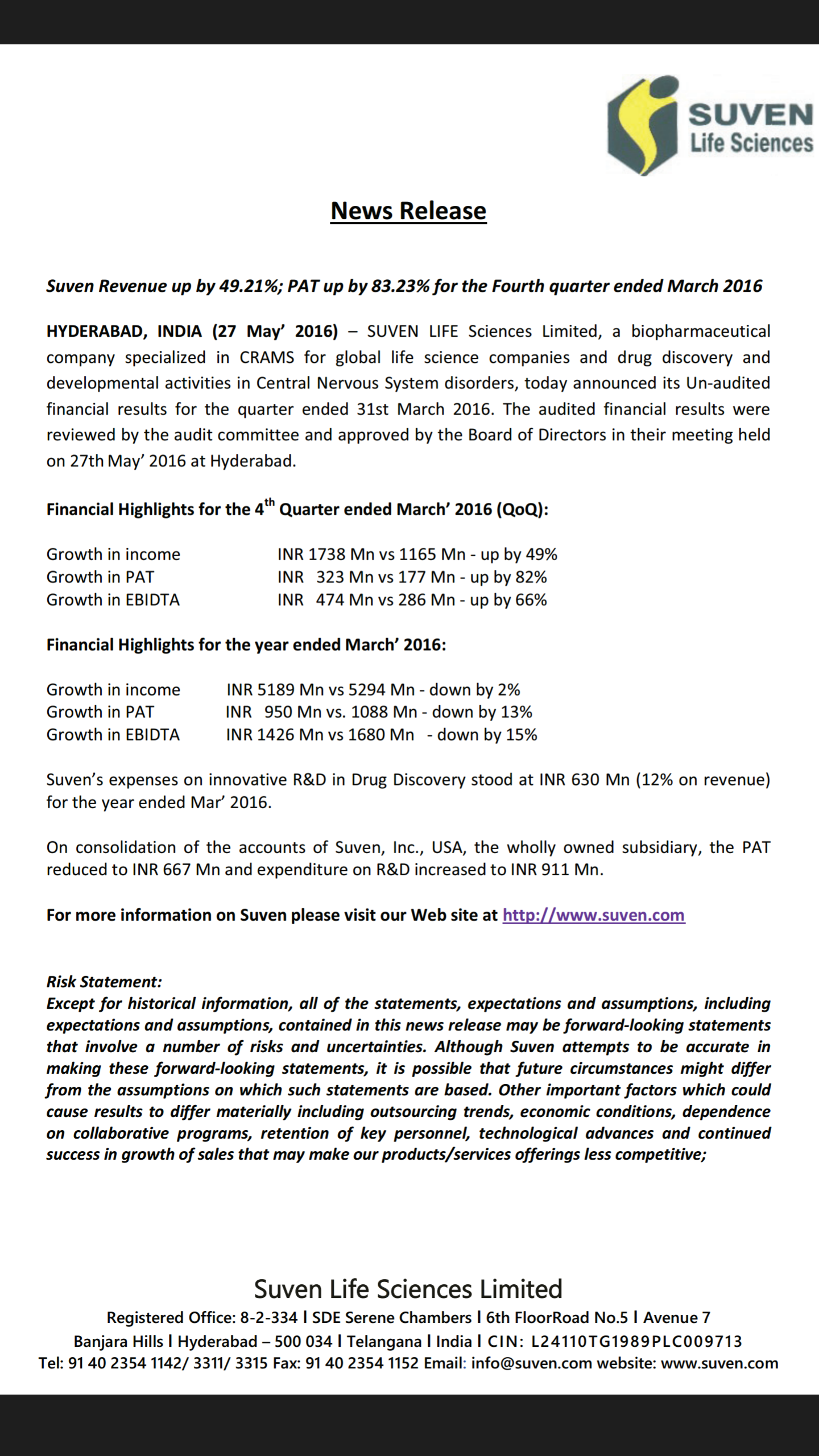

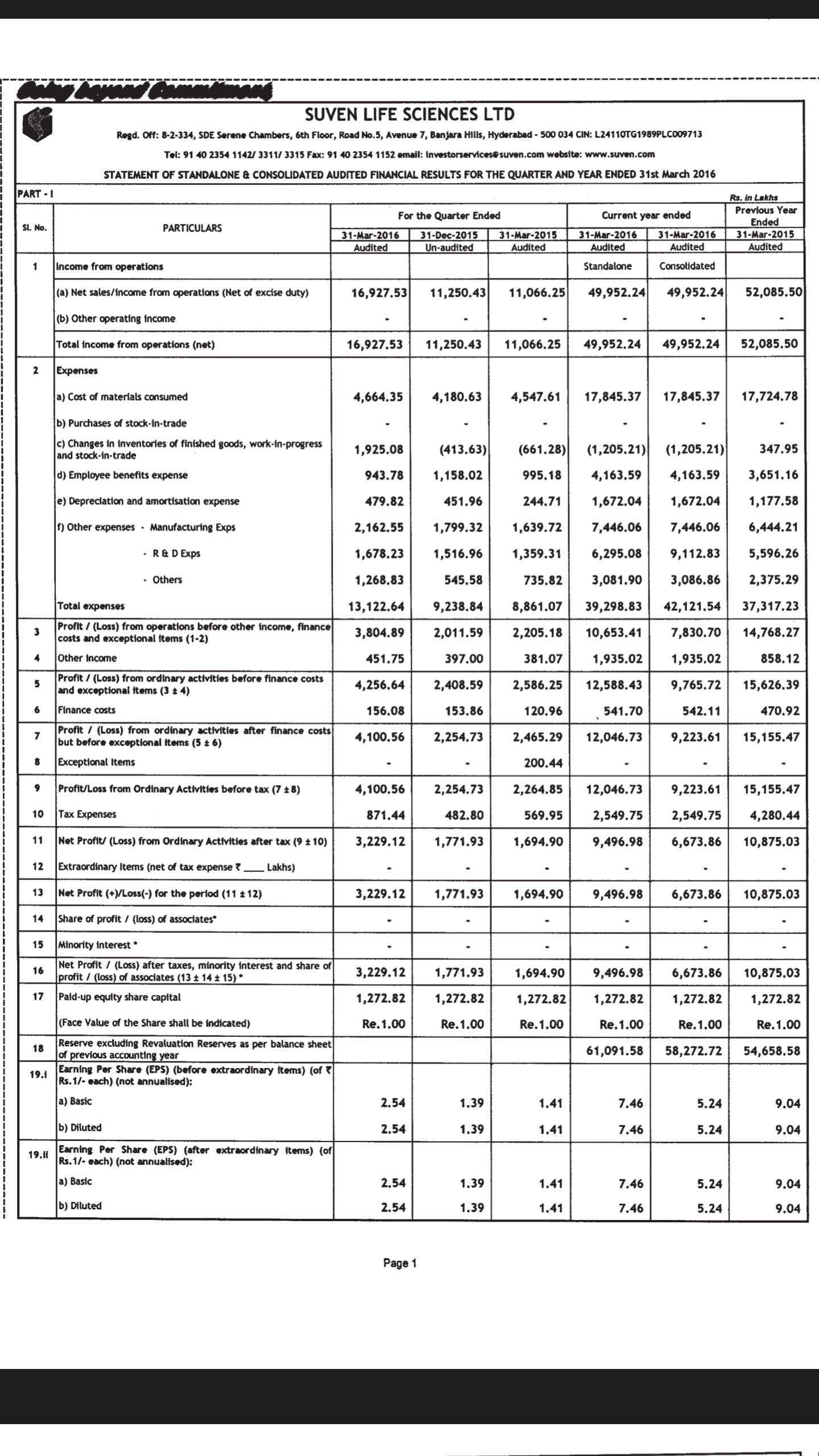

Suven Q3 results: http://corporates.bseindia.com/xml-data/corpfiling/AttachLive/AC6CA52B_3FAA_45E6_87A1_DD5030235F8E_145631.pdf

1 Like

Dear all,

Some notes from the concall ( from whatever I could gather)

- this year they had a degrowth in crams of about 17% in topline. The specialty chemical space compensated for that

- total rev from specialty chemical 220 cr for the year

- as per Mr jasti 220cr is the peak they can do in that space

- Fy17 they are expecting upwards of 15% growth in crams with specialty chemical remaining similar to last year.

- margins for crams (Ebidta) 30% and specialty 20%

- out of 3 molecules for which they got orders for preclinical phase they have got 1 order of 30cr to be executes in q1 17.

- of rest two second is doing well ( on innovator side) and they expect order by year end

- third one has been slow and he wasn’t sure when he will get repeat orders

- these compounds shud give recurring rev for 5-6 years

- malathion royalty wud remain same yoy

- vizag facility at current 45% utilisation. Plan to take it to 75%. However volumes won’t go correspondingly up as other crams facility was uti lised for the same and now vizag one will the one only for specialty chemical

- for suven 502 28cr was expensed last year and in Fy17 wud need another $10milion

- the trial is behind schedule by 2 months but confident it wud be ramped up. They need 500 patients for a gud data size.

- this drug is number 3 in sequence behind gsk and a Japanese one but has certain advantages when used synergistically with current t standard of care. Hence Mr jasti was very confident of making the cut. But earliest opportunity of monetisation wud be fag end of Fy18.

Please remind me of any errors.

Regards Nitin

Disclosure : invested since 45 levels. Forms 8% of portfolio

6 Likes

Suven has just published standalone results and tried to compare with same Q last year which is incorrect. Suven502 Phase 2 trial costs are supposed to part of US subsidiary now so we will need to look at consolidated results and comparison to same Q last year becomes irrelevant. Any one has any idea about consolidated results.

2 Likes

Company clearly disclosed that free cash flows along with funds raised in QIP are used to fund clinical research. So standalone results give the actual picture of Suven’s business. Consolidated results may not show any different picture if Suven is capitalising the R&D. I am not sure whether Suven capitalizing R&D or not.

Disc: Invested

1 Like

But aren’t shareholders entitled to access consolidated results? I can not find it anywhere. Lat year AR has consolidated numbers but this Q’s numbers don’t have consolidated figures. It is not capitalizing R&D but standalone number does not have R&D cost as it is booked in US subsidiary. Comparison with last year is incorrect as last year number had R&D cost in stand alone number.

1 Like

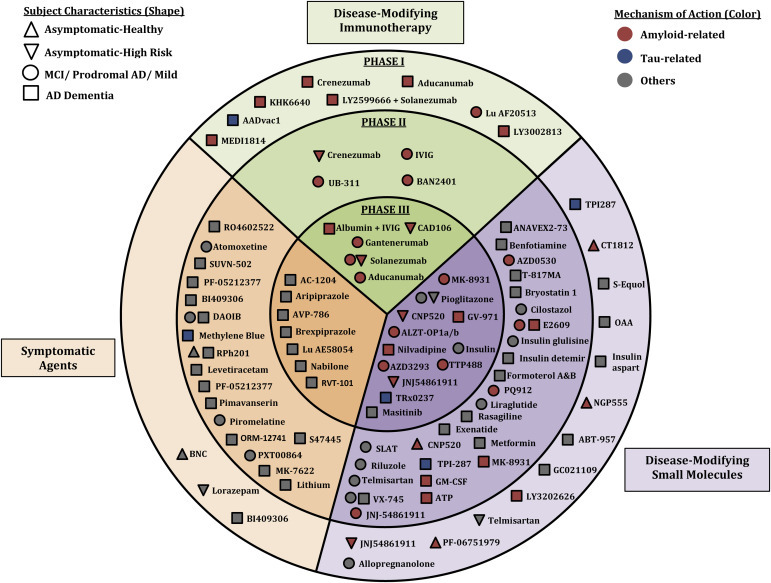

Drug development in Alzheimer’s disease: the path to 2025

Longish but worth a read

1 Like

Lundbeck says Alzheimer’s drug fails in late-stage study

1 Like

Alzheimer drugs received patent in India and Japan.

Extremely transparent management.

-Jiten Parmar

2 Likes

Suven @RESI (January 10, 2017 San Francisco)

The Redefining Early Stage Investments (RESI) Conference is an ongoing conference series that will be establishing a global circuit for early stage life sciences companies to source investors, create relationships, and eventually, get funding. The RESI conference focuses on the diverse breadth of early stage investors that LSN tracks, including Family Offices, Venture Philanthropy Funds, VCs, Angel Groups, Corporate Venture Capital Funds, and more. The RESI Partnering Forum allows fundraising executives to identify and book up to 16 meetings with life science investors who fit their company’s technology sector and stage of development. Additionally, through an expansive series of panels and workshops, attendees will have the chance to hear firsthand accounts from investors explaining their current investment mandates and process for identifying and qualifying candidates.

Who Attends RESI?

* Emerging biotech & medtech companies seeking investors

* Firms seeking strategic partnerships to build their companies

* Investors looking to source emerging technology

* CEOs seeking to parse the latest trends in the new investor landscape

Q2FY17 results delayed?

http://corporates.bseindia.com/xml-data/corpfiling/AttachLive/EF1751D4_42D7_4141_AF1C_FC90FA1BB9D3_152239.pdf

We wish to inform that our company will release IndAS compliant un-audited financial

results for the quarter/ half-year ended 30th September, 2016 within the extended time

lines as permitted by SEBI vide circular No.CIR/CFD/FAC/62/2016 dated July 05, 2016.

Notice of Board Meeting will be issued by our company at appropriate time.