Every time suven gets patents stock up by 5 to 8% and it would cool down immediately in next few days.

Can any body throw some light on what are these patents for? How much period they valid? When will they commercialize those patents?

@chintans The 50 odd molecules you mention,have little to do with their CRAMS operations.SLS’ main business activity is CRAMS,& they invest the Profits/Cash flows in their NCEs & develop them.The company is mostly focussed on addressing neurodegenerative diseases(Alzheimer’s,Parkinson’s,etc.) Any successs,would be a massive shot in the arm.However,given the lumpy nature of CRAMS revenues,the cash flows are also lumpy.This meant a lag in investments.However,since FY14 was a blockbuster year,the company decided to fast track one of its NCEs(SUVN-502) Also,they did a fund raising to address all the later stages.

So,growth won’t come from NCEs or these ‘molecules’,but from stabilisation of the core business(pre-supplies for ANDAs of some Pharma majors) and speciality chemicals.NCEs are just the glamour factor of SLS.

2 Likes

@sharemarketgen_ The 50+50 odd molecules that we are talking about, are new formulations being developed by innovator companies. The innovator companies outsource the manufacturing of intermediate molecules for these new molecules to companies like Suven. This is called Contract Research Manufacturing. SUVN - 502 is a new molecule being developed by Suven inhouse. Technically speaking, right now it doesn’t fall unders CRAMS category. However, the expectation is that Suven will sell the rights for this molecule to a large innovator company in return for cash and royalty option in case the molecule passes all trials.

Also, SUVN-502 was not fasttracked. It entered next phase after USFDA approved the Phase 1 trials. The core business is already growing at a very fast rate, and its not prudent to say that SUVN-502 won’t contribute to growth. It will contribute depending on whether Suven makes a contract with someone, and SUVN-502 passes all trials till such time (expectation is in FY17). The reason people say this is not in the price is that the statistical (historical) probability of molecules in CNS therapy passing Phase 2 is small. Hope I made some sense

2 Likes

Please refer this: http://www.moneycontrol.com/news/results-boardroom/profit-upnew-compound-big-plans-for-suvn-502-suven_822589.html

@sharemarketgen_ I have to admit I didn’t know what it meant to fasttrack a molecule (infact never heard the term before) ![]() . I found out from this link, page 2, first 3 paras.

. I found out from this link, page 2, first 3 paras.

But at the same time, I hope you figured out that the 57 molecules in Ph-I, 52 molecules in Ph-II, 1 molecule in Ph-III are the core CRAMS (CRM) business ![]()

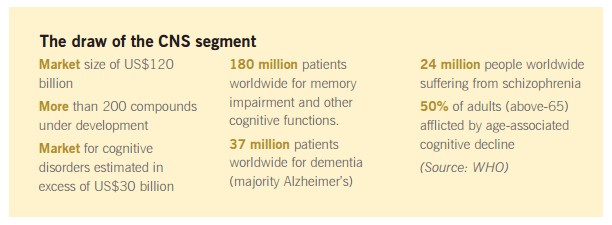

Anyways, on prodding further, I became more bullish on Suven. From this link, we get 27% as the probability (historical) of a molecule passing from P2 to P3, the lowest probability amongst all Phase trials for CNS (took this segment as the inhouse research of Suven is in this segment and has one of lowest success rates in trials). Phase 2 + Phase 3 takes 8 years for CNS instead of the general (2+4=) 6 years. So after 3 years, we can expect 27% of the 52 molecules in P2 to be in P3. The revenues are 10x in P3 compared to P2. Also, for P1, more than 27% (actually 56%) pass to next phase in a shorter time, again resulting in 10x revenue. For the P3 molecule, which is in this phase since at least 1 year, we can expect it to go to prelaunch with 27% probability (actually 46%). So just for CRAMS business, we can expect growth from 315 cr. revenue to 850 cr. (2.7x) in 3 years. The revenue would keep funding the inhouse NCE development also since revenue rises proportionately to R&D expense. For SUVN-502, company has kept aside 200 cr. from QIP, so that should certainly be enough. Adding back 100cr.(conservative) for 3 CRM molecules (depression, diabetes, arthritis) which are now in post launch phase, and 250 cr. for speciality chemicals (FY15 - 160 cr.), gives total revenue of 1200 cr. in FY18 v/s 520 cr. in FY15. That’s 30-35% CAGR. Typically for CRAMS, EBIDTA margin would increase in Ph3 compared to Ph2. So lets say ~30% revenue CAGR and ~35% PAT CAGR over 3 years. This is assuming inhouse NCEs keep guzzling cash but don’t contribute to revenue. 50 samples is a large enough number for probability to work its magic (very less variance due to linearity of expectation, and each sample being independent event). We made these calculations assuming the 110 CRM molecules are in CNS segment. If not, the time horizon would be shorter and (except onco, gynaec), the success rate (& hence revenue) would be higher.

@ananth, @ankitgupta, @crazymama, Please share your views.

@KS16, Q: (for AGM) what segments (CNS/oncology/cardio/etc.) do the Phase 2,3 molecules belong to? Breakup as % of revenue, or whatever info they can give like major segments. (Reason: This would help us figure out the expected revenue after few years in greater detail.)

Discl.: Not invested, yet.

2 Likes

Hi Chintan,

Haven’t looked at Suven and hence can’t comment.

1 Like

Hello Chintan,

@sharemarketgen_ has provided lot of valuable inputs in the early posts of this topic. Please read through them.

I thought i had missed the bus @ 72 levels.

Initially it was borrowed conviction, but on digging further and the expected increasing trend of outsourcing drug discovery further strengthened it.

But as the management has guided for 10% FY16 growth, IMHO this is one hi-quality business which we can do SIP to build position as i expect opportunities during the course of this year.

It makes sense to look at Suven in a similar light as PI Industries which does Custom Synthesis of complex molecules with innovator companies, and thus highly secretive and IP-protected. And like PI, we depend on the management’s commentary about CSM which is pre-dominantly on the conservative side.

From BQ perspective:

- FY14 was a teaser abt the potential fillip the topline and bottomline can receive when a Phase 3 CRM molecule is on the cusp of commercialization. In fact, EPA/Sales for FY14 at 22.24% was just short of Sun Pharma (pre-Ranbaxy merger). It only re-inforces the strong business architecture which has been established to provide disproportionate returns.

- R&D are expensed to the P&L and not capitalized.

From MQ perspective:

- Mgmt is very conservative and have shown the patience and long term vision which is expected to pay off from FY17.

- Can we classify Venkat Jasti as an intelligent fanatic? IMHO, undoubtedly so.

What about the valuation/price?

As Prof. Bakshi says, when u have a high quality business you need to pay up. For me, Suven is a fat-pitch.

Risks:

- Is it dependent on a main-man? What is the succession plan after Venkat Jasti?

Apart from the CRAMS, Suven has files DMF’s for certain API’s and will continue to do so to target those therapies which are not lucrative for the major pharma co.s to create more consistent revenue streams.

Disc: Invested. Views are highly biased.

Please do your own due diligence.

3 Likes

The latest annual report brings out in detail a lot of the things already mentioned in the discussions here. Though FY 16 is expected to show a stable growth, FY 17 is expected to be the key year not just for its CRAMS but also for its NCE business.

What I really appreciate about this company is the transparency of the management in its guidance. This time Mr. Jasti has even tried to address the fact that Suven is considered as a high risk investment due to non-repeat of orders and business.

Do go through the annual report - link here - its a great read https://karisma.karvy.com/images/2015/SPLN_2921/Suven_AR_2015_Low.pdf

Disc: invested and views may be biased

1 Like

I wanted to highlight some of the key insights from the AR -

"A NUMBER OF COMPANIES BUILD A PIPELINE OF PRODUCTS. AT SUVEN, OVER THE LAST TWO-AND-A-HALF DECADES, WE CREATED A PIPELINE OF CAPABILITIES INSTEAD. "

Pipeline leads to success and sustainability.

Suven has invested in robust governance, expensing its large and growing research and development costs. The Company has followed a policy of writing off research and development in the year of incurrence; it has never borrowed to invest in research and development spending.

Besides, four global innovator companies named Suven as a preferred supplier for their drug discovery and development programmes which, we hope, will result in more CRAMS projects coming our way across the mediumterm.

65.7% The outsourcing of CRO discovery services industry was estimated at 52% of the global pharmaceutical and biotech industry in 2013, poised to grow to 65.7% by the end of 2015.

Our company’s bottomline declined largely due to revenues from pre-launch supplies for three products declining from H175 crores in 2013-14 to H45 crores, a reality that had been anticipated and proactively articulated. This reality of a decline in profits brings me to a relevant point. Despite having grown the business every single year across the last five years, our business sustainability has been consistently questioned. We are perceived as a highrisk service-based business marked by volatile quarter on-quarter earnings because successful project completion may not necessarily translate into repeat orders if the project does not carry through at the innovator’s end.

The number of failed R&D attempts is rising while R&D capabilities remain finite, making it imperative to seek specialised partners. Decline in NCE approvals makes it imperative to outsource and build a research pipeline. Diseases are becoming increasingly multi-drug resistant. Global pharmaceutical sponsors have larger research outlays across a lower number of projects for which they seek specialised research partners

The section on “Risk Management” was thorough and a good example of Munger’s “Invert always Invert” mental model.

RESEARCH AND DEVELOPMENT

During the year Suven’s thrust on innovative R&D in CNS

therapies continued with an R&D spend of Rs 5894 lakhs

accounting to 11% on sales with an increase of 18% over the

previous year.

6 Likes

Yes, thank you for summarizing the key points… again, from the risk management section, we can infer that the management has always been proactive in highlighting the key risks which would impact future revenues and EPS.

Best is do a SIP throughout FY 2016

You stole my words. Hopefully Ian Cassel would agree.

Couldn’t agree more. I think we are not paying much above fair value either, with a 3 years forward horizon.

@sharemarketgen_ Thanks for pushing me to this gem.

@Dhairya The 2013-14 AR was very handy. Actually much better than the 2012-13 AR.

@crazymama In the calculation, I assumed 27% chances of going from P2 to P3. Infact if all molecule are not in CNS, probability would be higher and time frames shorter. Also, it’s not as though these molecules entered P2 on 31-Mar-2015. Some of them could be much closer to completing the P2 trials. The inhouse NCEs and API formulations could boost things further.

At the same time while we are so gung-ho, its prudent to point out that in 2008 many innovator companies cut down on research - which directly affects the CRM business of Suven. This is bad on 2 counts:

- US exposure could hurt in another financial crisis - where an Ajanta would fare much better.

- R&D costs are first to be cut in crisis - a Shilpa/Alembic with its generic pipeline would fare much better.

Though Suven maintains that after the crisis, the innovator companies separated the wheat from the chaff and allowed only promising molecules to move forward in trials.

Discl.: Forms ~14% of my recently adjusted portfolio.

Yes. They did cut down on their in-house research and outsourced it to players like Suven.

As highlighted in AR, Higher percentage of NCE rejections, increasing R&D costs makes the oppurtunity size for Suven higher as the business-motivation to outsource increases further.

Also wanted to highlight 5 new clients were added in the Global Relationship snapshot.

Perrigo

Bayer

Valeant

Fujifilm

Could not discern the 5th client due to the poor quality.

Disc: Suven remains 5% of PF. Intention is to keep doing SIP and max it out at 10%

1 Like

Innovator companies are outsourcing more frequently to companies like Suven. This is the value migration that Raamdeo frequently talks about.

What I meant was the following:

Excerpt from 2013-14 AR, pg. 20:

Post-2009 scenario

The global financial slowdown impacted

drug discovery initiatives resulting in a

weaker pipeline of innovator companies

and blockbuster launches. Interestingly,

however, research efforts became more

streamlined and concentrated around

select therapeutic segments. Significant

efforts were made in analysing and

assessing prospects in preliminary

stages, which helped increase the

probability of converting a prospect into

a product.

The impact of this transformation is

evident. A recent report examining

innovation in the drug development

pipeline discovered that 70% of 5,000-

plus new molecular entities being

investigated were potential first-in-class

medicines, or medicines in unique

pharmacologic class distinct from other

marketed drugs. Besides, among 27

new molecular entities approved by the

USFDA in 2013, one-third represented

first-in-class medicines, indicating that

they use new or unique mechanisms

of action, while a third addressed rare

diseases.

1 Like

@sumi00, With regards to the CRM pipeline, I think the large number of molecules in pipeling already provide much more than enough diversification. If one wants to build the expected value of SUVN-502 in valuation, diversification in portfolio is absolutely crucial.

Till now Suven didn’t capitalised the R&D expenses. They have rised 200cr through QIP to fund R&D expenses. They have diluted equity for R&D which indirectly means capitalising the R&D. Now they have approx 250 cr cash reserves to fund R&D. My question is… Will they continue to show R&D cost as expense or not? If they don’t show NCE R&D as expense then their profits will increase by 50cr atleast .

This a very valid point and a different perspective about R&D capitalization.

how is raising funds by diluting equity thro’ qip tantamount to capitalising r&d ? can you explain your logic ?

1 Like

This can be a real multibagger from here. Regular biz expected to grow only 10-20% in next couple of years. If any of their molecules click, sky is the limit for this stock. But it will take 2+ years, before we know the success of any of its molecules.

Disc : I hold from long (at 25 levels) and intend to hold more long. Do not construe this as a buy advice.

As per my understanding. Till now company showed their R&D expenses on NCE as an expense in P&L statement. This is actually not an expense but a capital on NCE segment as it didn’t have any revenue. I think because of this only suven return ratios are sky high. Now company using the money rised through QIP i.e diluted equity money to fund R&D cost of NCE segment. Because of this returns ratios fall because of increase in Equity. Now company no need to show this R&D cost as an expense in their P&L statements so they can show more profits.So they have to pay more taxes also.

Please correct me if I am wrong