Howlers continue (I mean in the day - I saw PFS and now this) !!

http://www.bseindia.com/xml-data/corpfiling/AttachLive/DD92EDC0_54B9_405A_B4DF_CF17B2558CDF_135718.pdf

Stock is going to be gorged for sure. Everything looks weak !!!

The biggest asset of Suven used to be its profit margin but net profit/EPS have halved now…

Absolutely flat FY16 guidance and poor Q4FY15, so stock will take some beating. Management in true Suven style said “Without knowledge of any repeat orders coming in, more or less FY16 will be flat”.

1 Like

I have some update from the co. sec

Pasting the specifics below

Mr. Rao

How are you? The flat results and subsequent guidance of 10% growth by Jasti has shaken us a bit but using this as opportunity to buy more of our favorite stock Suven. Here are some specific questions ;

Has the Vizag plant gone on stream of production? You had said in the below mail April and May 2015. If yes, how much it will contribute to the growth? I assume that the 10% projection given by Mr.Jasti includes this ? pl clarify

I had seen the occasional CRAMS order boost the PAT figures and I am sure that you must be looking out for one during the current fiscal. Given the flat growth projection, can this be the extra focus for you guys so that by Q3/Q4, we vault over, by showing improved results?

When and where is the AGM?

Thanks

Kalyan

Dear sir

Greetings from Suven. We give our replies to your queries as under

Commenced trial operations. Once validated will commence commercial operations. Yes, 10% projections given includes this facility.

CRAMS constitute major portion of revenue, which includes specialty chemicals. CRAMS grows at approximately 15%, YoY. The occasional-additional revenue related to one time pre-launch quantity was there in the year 2013-14 and the repeat order at commercial level for the same usually takes about 18 to 24 months. If we get repeat order, there is a possibility of revenue going upwards. So far, we do not have any visibility on the repeat order for commercial, the flat projections/guidance was given.

AGM will be held on Friday, 14th Aug 2015 at FAPCCI, Lakadikapul, Hyderabad.

Thanks

with regards

k h rao

PS - this is not a buy/sell reco. Please do your due diligence

3 Likes

Excellent Research Report from Karvy on coverage initiation:

https://www.karvyonline.com/viewdocument.aspx?DocumentID=10504

I have cherry-picked the most relevant poins from the above report,

Conscious effort was made to ignore and not highlight the analysts projections and estimates… ![]()

Robust base in CRAMS with client stickiness:

The company partners with innovators to develop intermediaries. SVLS was involved in over 725 innovation projects from its inception and has developed a secure basket of repeat clients with a min/max partnership of 2-15 years in the different stages trials.

Developing recurring revenue streams: Utilizing its strengths of complex intermediaries and innovator clients, the company could carve out independent streams of revenues expected to get base loaded into a constant run rate:

• A Specialty Intermediate supply: The company has been generating revenues of USD 10 Mn and 20 Mn in FY13 and FY14 respectively; and the company has built a Vizag facility to further enhance production. • Commercial supplies: Three molecules from Phase-III CRAMS have moved into commercialization in FY14. The company supplied pre-launch quantities and are expected to generate constant supplies for production from FY16E.

• Formulations: The company has out-licensed ‘Malathion’ ANDA and intends to develop 3-4 more such ANDAs with close to 13 ANDAs in pipeline.

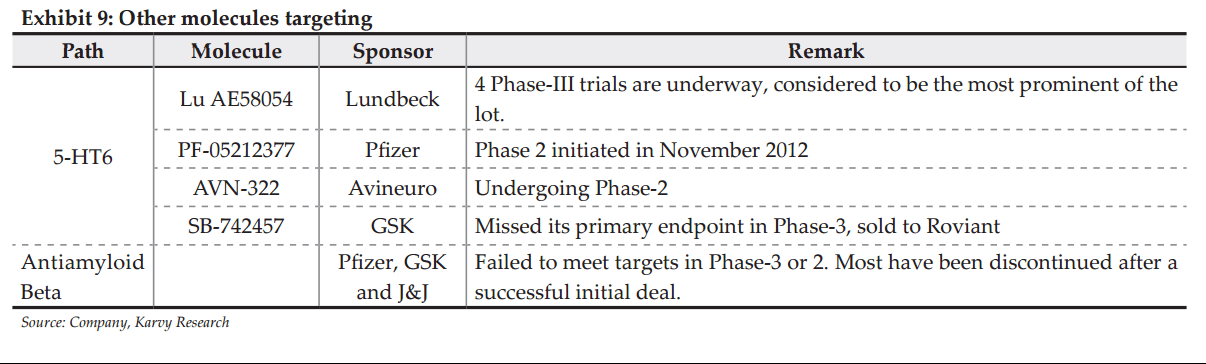

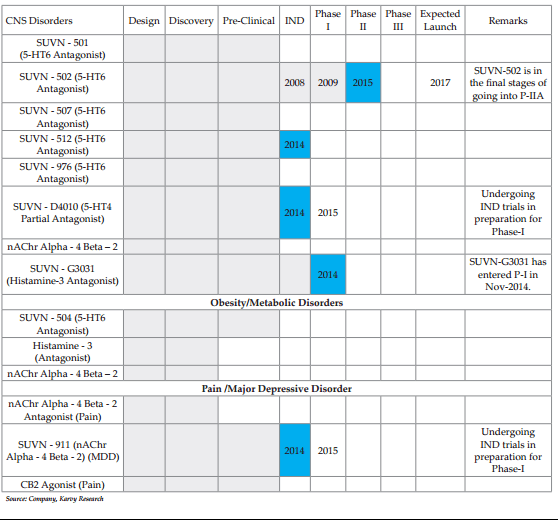

Drug Discovery-Developing a portfolio in NCE’s: SVLS has been focussing on drug discovery from FY05 covering discovery, IP creation, clinical development and out-licensing. Even in a cost intensive unit as such, the company followed disciplined method of funding. SVLS has built a pipeline of 13 molecules in therapeutics of CNS, Major Depressive and Obesity in 2006 with SUVN-502 as the lead molecule in CNS segment currently about to enter Phase-IIA. The company has 13 molecules and 26 inventions protected across markets with its 700+ product patents and 37+ process patents. SUVN-502: Targeted at Alzheimers Disease (AD), a huge unmet medical condition, with only palliative care addressing relief from symptoms (Donepazil) available currently. The molecule is expected to begin phase-IIA PoC trials in Q2-FY16 with an expected term of 2 years. The molecule acts as 5-HT6 serotonin receptor antagonist, the method which is currently regarded in this segment after the recent spate of failures for molecules following the antiamyloid method from Pfizer, GSK and J&J. In 5-HT6 Lundbeck-Otsuka in Phase-III, Pfizer in Phase-II are the other leading molecules along with Roviant (acquired from GSK) and Avineuro in Phase-IIB.

The company plans on out-licensing the molecule for an upfront, milestone and royalties subsequently if the molecule gains traction after clearing the proof-of-concept stage it is currently in. Comparatively in this space in June-13 when it cleared Phase-II, Lundbeck received an upfront payment of USD 150 million and is also entitled of upto USD 650 million in regulatory milestones. Apart from this, royalty from sales could be above 10% for Lundbeck.

Key Risks

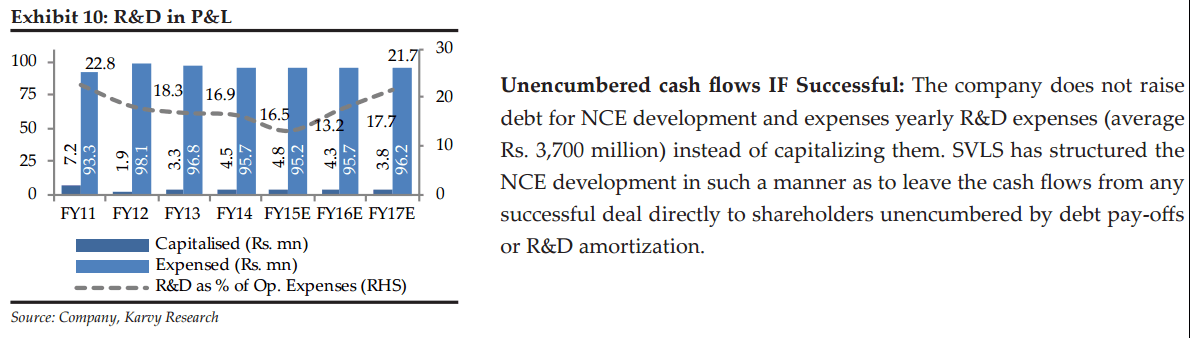

• Risk of NCE failure: The company has developed a well diversified portfolio of 13 molecules. Any set back in the long drawn process of the NCE development will have an impact in the short term. It has to be note that the company does not have any downside financial risk in any event of failure or set back of approvals as the financing is by equity sources and balance sheet does not carry any of the assets under development.

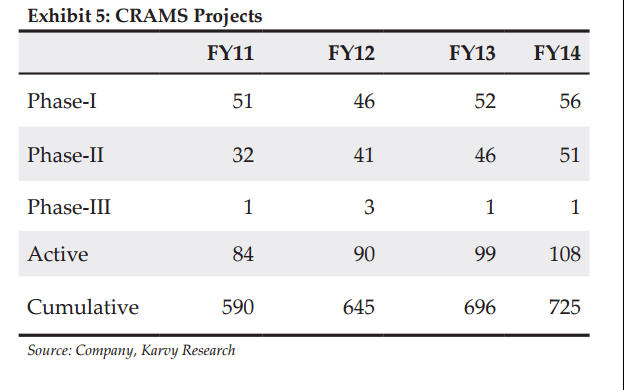

• CRAMS projects concentration: The company has 108 projects currently from a smaller number of clients, increasing the client concentration in the number of projects it handles for each client.

• Regulatory slowdown in approvals: Even as the company is not involved in the approvals of client products its supplies intermediates to and significant increase in rejections could significantly impact the revenues of the company across streams.

• Foreign currency fluctuations: As mentioned, the company earns close to 85-90% of revenues from exports exposing it to significant currency fluctuation risk.

Disc: Sold of Alembic Pharma to buy Suven Life sciences with avg price @250 (after FY15 results)

Invested for the long term.

Please do your own due diligence.

8 Likes

@crazymama Vishnu - specific Q to you and other Suven investors - The answer here will help me to increase the conviction since there is golden chance for me to invest in Suven ( given the correction from 300 odd to 240s now) by exiting strides, Cadila ).

We know that the current FY is going to be flat - with 10% growth at best ( Jasti had said it in multiple forums). We are banking on FY17 block buster in Alzheimer’s drug. Question is - are we taking too much risk in just this one drug to click?

I came across a Forbes article recently.

In that article, they mentioned that Eli Lilly started working on Alzhameir’s drug 25 years back and couldnt get a break through after Trial stage 3. It was a devastating failure for everyone involved.

But Biogen took a different approach and is showing promising Trial Stage 3 results, though with a small trial population - but certainly promising and the first time ever by a drug company on alzemeirs.

Compared to oncology drug approvals, 19%, alzemeirs has ~0.29% success rate in drug approvals.

Given this background, I tried looking up articles on Suven. Suven completed stage 1 trials and they are yet to get started on Phase 2A, and a line from Jasti summarizes the whole gamble “It’s always a huge bet, it’s zero and one, there is no in-between”.

Though it would be a jackpot of Phase 2A trials are successful, but I feel its a huge bet given success rates of Alzemeirs drugs.

PS - significant allocation in Suven. Average price 235

Hi @KS16,

I see Suven as a decent business + chance of a patent.

As Vishnu has pointed out above, in case the SUVN 502 turns out to be a failure, the balance sheet will not deteriorate but the stock price will certainly take a hit in short to medium term.

On the other hand, if the patent bid is successful, the upside will be huge. Although statistically it’s a low chance.

Now the question is, how do you value the underlying business without considering the patents? If we consider it to be worth say rs 100-150/share, you are essentially playing a gamble with the remaining money for a long period at an opportunity cost.

If you are OK with this, you should totally stay invested for long, otherwise we know what to do.

1 Like

@kalyan If you see Mr. Jasti’s track record,he has always been conservative in guidance.Even for FY15,the guidance was of a 90-100 cr. PAT.However,they ended up delivering much more.Similarly,for FY14,the guidance was 125 cr. & company delivered a PAT of 144cr.What strikes me about Suven,is their ability to find high margin segments.Even without the Vizag plant & ramp down of the big orders(vs. FY14),the company managed a very good EBITDA margin.Their specialty chemicals division did pretty well.

On SUVN-502,the sense I got was that the management is fully mindful of the risk.They have many times stated,that they have been ‘learning from other’s mistakes’ in the same space.So,they know what they are doing

However,I tend to look at Suven in this way: A stable,growing business with a free lottery ticket.The drugs for which they had delivered the ‘pre-supplies’,are doing well.Once the repeat orders come,there will be revenue visibility for many years to come(almost like an annuity business) Along with that,you might have SUVN-502 being monetised.

At the current prices,the margin of safety doesn’t seem too high.Though,if one removes the glamour factor…there is a pretty decent,highly profitable business which is lumpy when viewed quarter to quarter.As an investor,I will be worried only if SUVN-502 goes horribly wrong or if the repeat orders are delayed beyond 15-18 months.

Disc.: Invested…views maybe biased.

3 Likes

At what CMP should we enter to have a descent margin of safety as per your thoughts ?

Disc: Not Invested. Tracking from past 3 weeks. Will invest considering MoS

@sharemarketgen_ wish to congratulate you on the clarity of thoughts. I was trying on the similar lines for past few days but could not articulate.

Indeed, what you had said is true. Apart from that Suven has got a repository of Patents. Hope at some point, the management will go for commercialization of the same. That will open additional revenue streams in the form of royalty/monetization/annuity/additional orders. And that why it is valued richly @ 26/27x by Mr Market.

Disc : Invested.

Intresting article

1 Like

hi, I would think that it is fairly priced for its growth and CSM business. The value of of SUVN -502 is highly debatable and not easy to assess. The value will be known (whether it zero or more) by 2017 after spending 200 cr. This is a critical phase and nobody can say anything (not even mgmt) about it. So the current business should be valued without considering SUVN-502 and it seems to be fairly valued right now - no major triggers or growth opportunities right now for the next 1 year or so.

Regards,

AGM is on 14th Aug, which happens to be a Friday. The possibility of me attending this is high and if not, one from the VPr group in Hyd will certainly be present. Can we start compiling a list of potential questions for Mr. Jasti and Hanumanth Rao? I will prefer emailing them the list earlier so that they come prepared with answers. Giving a month runway for us to be prepared totally

Q: For CRAMS, there are 50 odd molecules in Phase 2, and 50 odd molecules in Phase 1. Some from Phase 1 will obviously not go through to stage 2. Does this mean less growth/degrowth going forward? It could be possible that molecules currently in Phase 1 are more lucrative or that co. gets business for some molecules in Phase 2 directly.

Thanks @chintans. Looking for more from others like @sharemarketgen_who have been around a while in Suven

I think suvn502 failure wont break the company but success will be a big bonus - currently its not priced in - I expect FY 2015-2016 to be operationally flat so the patient investor might have time to accumulate.In summary my thinking is suven is a good bet for above average returns (with the potential for jackpot which is not in the price and is 2 years away )

http://www.bseindia.com/corporates/ann.aspx?scrip=530239&dur=A&expandable=0

Suven Life Sciences Ltd has informed BSE regarding a Press Release dated

July 17, 2015 titled "Suven to Present at Alzheimer’s Association

International Conference (AAIC

One thing I find contradictory is that this company’s PR advertises too much about their potential IPs - patent filing, attending conference etc. On other hand CEO tries to tone down expectations when stock prices react positively. Is this a managed show?

@KS16 , I think that was a bad question. The phase 1 trials typically take many months (may be upto a year), and phase 2 trials take upto 2 years, so the phase 1 pipeline seems to be very strong.

@KS16, Kalyan, will you pls ask regarding, if there is a clear road map for commercialization of the basket full of patents?