Suven AGM 19 Notes

Chairman’s Speech

- Although visibility is limited to forecast about Q2, FY20 on a whole can be a lot better with minimum 25-30% growth in the profits possible.

- The company expects to do following CapEx over next 24 months - Multi purpose plant at Vizag for 120Cr, Formulations capex of 90-100Cr, 100cr capex at Pashamylaram.

- The company will be focused on niche molecules in formulations & will be filing ANDAs in 2020

- The company invested 35mn$ for a 25% stake in Rising Pharma, which is a development & distribution company. The stake was bought during bankruptcy proceedings. It takes ~2 decades to build a company like Rising which works with collaborators to file ANDAs & also owns distribution. The company hopes to gain as & when commercialization happen for ANDAs in Rising. This will take 2-3 or more years.

- The company will be split into two companies - namely Suven Life Sciences & Suven Pharma with mirror shareholding. Suven Life will have all the IP, NCE molecules etc. Suven Pharma will house CRAMS business & corresponding assets.

NCE business

- All the expenses are already written off.

- SUVN-502 - 560 patients were enrolled. 26 week study has completed but CRO could not get the data on time & hence could not publish the data. Now study will be extended for four more weeks & data will be published by Sept.

- SUVN-3031 - The molecule is focused towards dementia, Alzheimer with a condition called Narcolepsy - excessive day time sleeping. Most current medications are habit forming ones while 3031 will be non-habit forming & with more safety. Patients will be enrolled anytime for 3031 now. It’s a shorter 14 day treatment followed by 7 day washout period.

- There are two more molecules which are ready to go into clinical phase II trials.

- The new demerged company will have enough cash for two years. The management feels that the pipeline is good.

Q&A

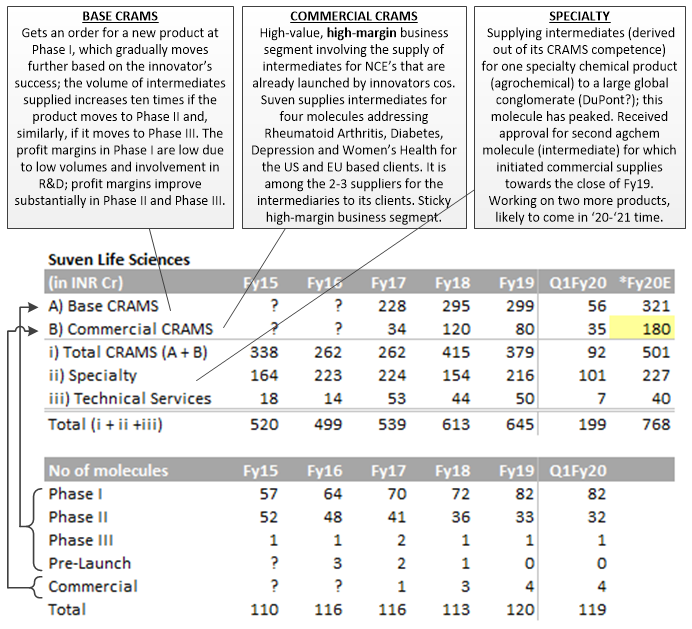

- The word CRAMS was invented by Suven during its IPO in 1995.

- There is one molecule in phase III which is likely to go into commercialization - revenue potential of 15mn$.

- In specialty business, first molecule is delivering revenue of 20-30mn$ & the recently approved second molecule is delivering 6-7mn$. The company expects more molecules will be approved in 20-21 & the potential of these molecules would be 6-7mn$

- Can CRAMS business go to 1000Cr sales? - Commercial CRAMS business can double as the company is seeing better traction.

- MEIS export benefits of (18-20Cr ). The government is thinking of doing away with them? - The company feels that the incentive will remain just that the program will be restructured. Anyhow, the incentive is not make or break for the company.

- Why is company getting into formulations business? Would it not conflict with CRAMS business? - The company has 13 molecules in pipeline, 4 are in clinical trials. Formulations capacity is towards that. With Rising Pharma, the company will identify niche 25mn$ molecules & align with innovators to produce them on some profit sharing kind of terms, So there is no competition with our innovators.

- Which is our strong or special therapy? - CRAMS business is therapy agnostic, it is rather based on chemistry skill.

- Almost ~300Cr of CapEx planned over 24 months, what’s happening? - We are preferred CRAMS supplier for Big 4 pharma companies. This does not guarantee any business orders but it provides more opportunities to bid. The company is seeing good traction in the business.

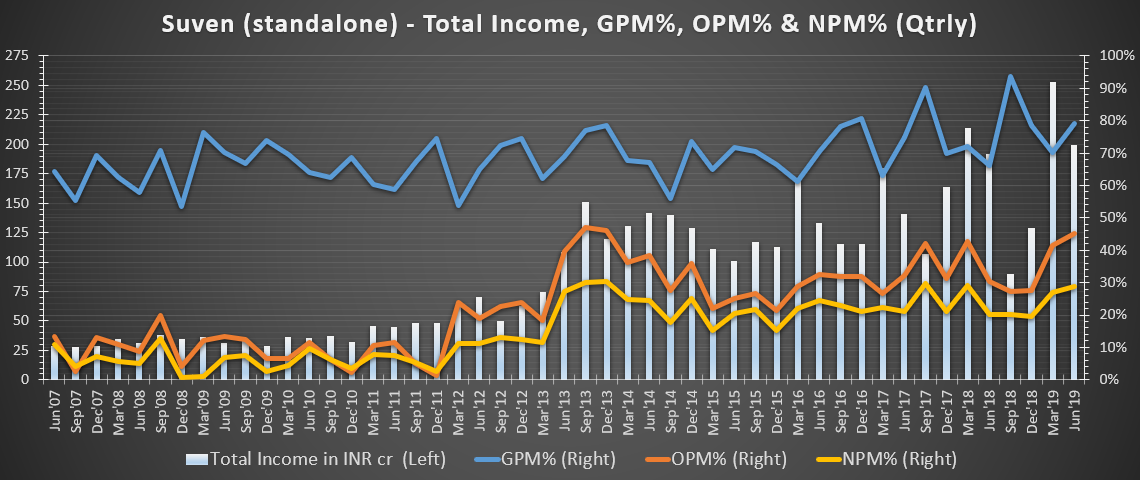

- Reason for high margins in Q1 FY20? - High margins are due to product mix & they might be sustained in FY20.

Disc - token position to attend AGM, have not done in-depth work on the story, mistakes in notes above are solely mine, not a buy/sell recommendation