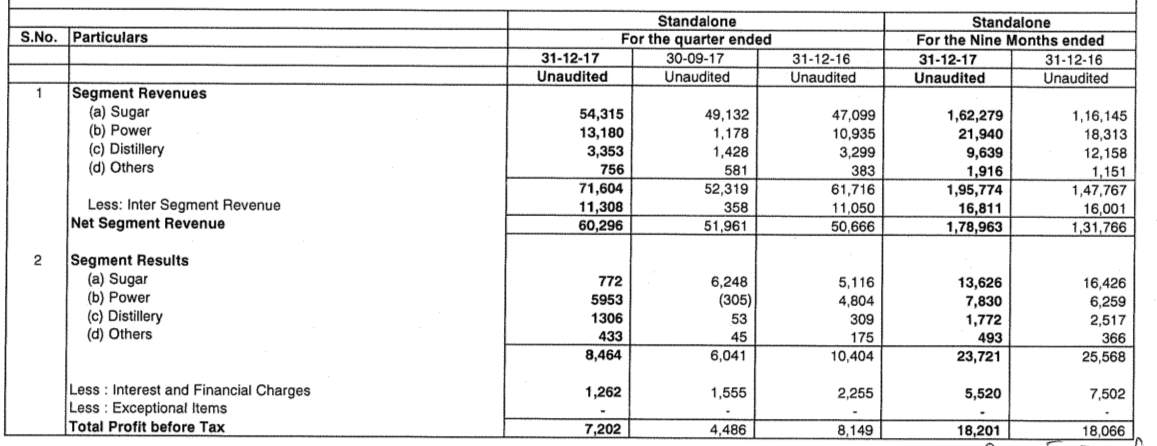

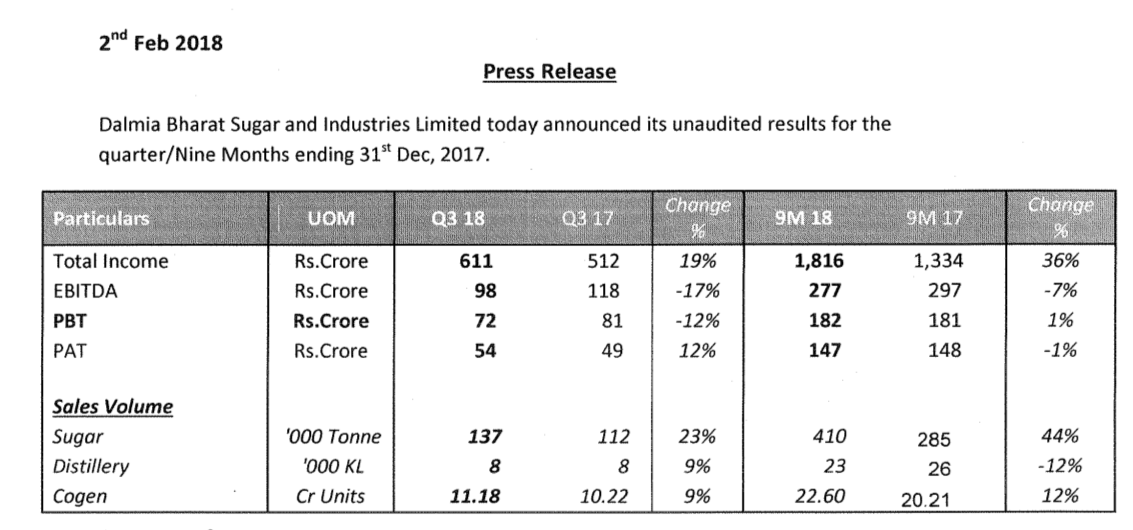

The above two figures are from Dalmia Bharat Sugar Q3FY18 results. According to these the company has sugar revenue of 543 crores for sales of 137,000 tonnes sugar. Therefore sales price comes to 39.6 per kilogram. This seems unrealistic given the average spot price of Oct, Nov, Dec 2017 period was Rs. 34/kg.

I will thankful if someone can explain this discrepancy?

This is because of inter segment revenue. Sale of Bagasse & Molasses to Cogen and Distillery respectively is counted in sugar segment revenue. Similarly sale of power to sugar plant is counted in Power segment revenue. You would see that inter segment revenue are excluded in the end.

Such a flawed model. Government implementing MSP, don’t want cane arrears to go up, not giving export subsidies, but forcing mills to pay to farmers in 15 days and do their export quota! Only way this chain can remain healthy is by deregulating sugarcane prices. Sugar prices are expected to fall more this month.

Just in a matter of 6 months, the leader stocks dhampur/balrapur have gone such a downhill. Dhampur almost is back to sub 100 levels from 300 plus.

Those who wanted to have a quick gains of 10 to 20 percent and enter at the top of the cycle have eroded their capital in such a short time. Now the wait for next upcycle is far-far away.

I saw Anil Kumar Goel holds almost 500 cr worth investment in Sugar? what was his thought process behind? May be he thought THIS TIME ITS DIFFERENT?

I followed this sugar cycle from the past one and half year and made some decent profit by following advices of senior boarders like Mehnaz/Jiten(very great full for them). Existed stock like Ugar when my friends were advising it will reach 100.

I keep coming back to this thread because i dont want to miss the next cycle. I want to understand few commodity cycles and want to benefit from it. Right now, am invested in metal stocks like Hind Copper. Can anybody advice on whats the best allocation for commodity stocks in your folio…

This time it could be really different (and may be not):

the change in cane variety to short term, high yield one is one change from current cycle to all previous ones. This is allowing the Mills about 40-50 extra crushing days (150 to now 200 crushing days). Without investing single rupee, the crushing capacity has gone up by 33%.

the high yielding variety has improved sugar realization too. Without having to pay any more money to farmer (in UP only) the companies are realizing 50% extra sugar due to improved realization from 9% to 13%. This drives down per kg sugar cost.

the extra sugar this year is only 4.5mt (excluding carry forward inventory). This could be gotten rid of in many ways, if govt has will, which so far did not take concrete action. a) talk to Bangladesh n Sri Lanka which are net importers and export excess sugar to them at losses by giving forced export quota to each mill. b) use the law to fix min sugar selling price of 34 rs.

c) this is easier but can not be implemented this year. Use of b-heavy molasses for generating ethonol, thus getting rid of excess sugar. The Mills did not anticipate sugar price fall this year. If they had anticipated they probably would have implemented this as much as they could. Still, I believe the Mills with good distillery capacity might already be doing it starting from this quarter. Brazil uses sugar juice directly to produce ethonol. They are planning to increase the ethanol produced from sugar cane juice as sugar prices are not remunerative. The ethonol blending can go up to 25% (even more too). The current distillation capacity supports only 5% blending. The companies now have to come up with more distillation capacity and start producing ethonol from sugar cane juice/b heavy molasses when they predict excess sugar production.

the rise in oil prices (got to see how long they last) would help better realization of ethonol (hope govt increases ethonol buy price now).

the world is facing threat of water shortage. Sugar production will not be growing as fast as it happened earlier. This is a threat to our Mills too. But I feel, UP based companies might be in good steady for next 10 yrs. There is a famous investor who is buying badam farms because, they are water guzzling like sugar cane and there will be badam shortage in future due to water shortage. It applies to sugar too.

the arrears to farmers seem to have built up rapidly to 20k crore. If govt wants to win next election, they have to get the farmers paid. The sane govt would make Mills profitable to clear the arrears. An insane govt would force the Mills to pay the farmers even though they are bleeding.

All said and done there are too many variables at play here.

Disc: I am new to investing and don’t have much knowledge about sugar industry either. These are just some thoughts. Invested small money in dhampur @200 and can wait until it gets wiped out or until there is a real turn around.

My mistake. It is about 11%+ for dhampur as per last concall. As the newer vareity gets adopted more and more the recovery % would keep increasing. Just searched Google and came across following article.

Sir ji,

This is old technology now. I am sugarcane farmer. In UP no body is cultivating old varieties. This theme is played out already. Also new sowing technology has increased the yeild from 250 quintal to 360 quintal per acre.

Do you have estimate of sugarcane production for this year? According to Govt. it should be around 353 million tons. But some people doubt this number.

Difficult to estimate. I know the sown area in up is more. Yeild varies too much like sowing time, monsoon etc. So difficult to estimate for all agencies.

@Gaurav_Agarwal

Thanks for sharing the news. I have just started understanding the sugar commodity cycle & it effects on share prices.

As of now the above news indicates that Sugar Mills are having Production cost of Rs.36 per KG. Do you have any historical data/news post which can give some sort of production cost in various years.?

I am just trying to understand the estimated loss per KG in various production quantity.

What do you feel how many years it would take (considering the normal monsoon each year) demand would match the production?

The best source to know the production cost will quarterly press brief or annual report by the companies, news items are news item.

It is very difficult to estimate the time period for demand-production match but cane arrears are too high and I think this cannot go on for very long.

If this realizes, it augurs well for sugar companies too. The crucial point being reducing the GST on ethonol & also increasing the sale price. Combining these short term measures with more important long term ethonol policy determining some formula for predictable calculation of ethonol would encourage sugar companies to install more distillation capacities which would ensure steady income for the sugar mills.

Disc: I am new to investing and don’t have much knowledge about sugar industry either. Invested small money in dhampur @200 and can wait until it gets wiped out or until there is a real turn around.

In Mahabharat, replying to Yaksh question, Yudhistir says the most amazing thing in the world is that thousands die, yet those living go on as if they will live forever.

Here the most amazing thing is that even in face of such massive over production, investors still do not believe that a 3-4 year downcycle in sugar industry has started.