Both Dhampur and Balrampur are displaying technical weakness…and i have fully sold off Balrampur. And as earlier disclosed, i have completely exited from Dhampur too.

Its very paradoxical…sugar stocks showing such weakness, just when we have the biggest sugar defict of around 5 million tons after 8 years…all three showing technical weakness…sugar stocks, domestic sugar price, and international sugar price.

Perhaps when i am a bit wiser, i will understand as to why such a thing happens in the market. As of now, i stand down. Will consider, buying back sugar stocks later…if and when they show signs of turnaround

Dear Mehnaz,

The logic is like ‘when everybody is bullish and macro conditions are strong, that’s the time when intelligent people (read Investor) reduces their positions’.

The decision of reducing import duty, whenever that happens, will lead to firming up of international sugar prices which will have a cascading effect on domestic prices. Come October, price are bound to go up to astronomical levels due to reduced buffer stock. Only reassuring and comfort factor for the Govt (albeit not good for Sugar investors) is El Nino may not be severe, as per latest weather reports, and may not affect Indian monsoons next season leading to increased output from Maharastra and karnataka.Patient investors for another three quarters will see hay days. It is not gone unnoticed some HNI investors have also taken position in Dhampur and Dwarkesh Sugar.

Skymet is forecasting a below avg monsoon and all nino to impact monsoon this year. This should further boost fundamentals? Not sure why stocks are not responding…

ICRA reaffirms the tight supply situation, which augur well for UP based sugar mills for next 2 to 3 qtrs. Prices have rebounded to Rs 37000 per tonne due to tight supply situation.

Global prices are on downward trajectory http://www.nasdaq.com/markets/sugar.aspx and INR is also strong against $…any idea what could be landed cost of import at current situation?

Global price trends will harden once India decides to import. Besides with cyclonic weather developements, Australian and Thailand sugar production was adversely affected leading to shortage in global supplies.Patient investors in UP based suagar mills for next 3 quarters will handsomely be rewarded. Any price aberration in short term should not be given a serious consideration.

So, to all the macro economoy guru’s, what is likely to happen in the next 3 months, I am getting confused after reading so many analysis…

Is Indian Sugar prices directly proportional to global sugar prices?

Last year, Dalmia Bharat Sugar and Industries Ltd invested about Rs 150 crore on expansion of its existing sugar plant at Kolhapur in Maharashtra. The company has five sugar plants in Uttar Pradesh and Maharasthra with cane crushing capacity of 29,250 tonnes. The power co-generation and distilleries capacities at these plants are 94 MW and 120 kilo litre per day, respectively.

Dalmia Sugar had entered Maharashtra by acquiring the Kolhapur sugar mill in 2012 for about Rs 135 crore. Then, it invested another Rs 200 crore to double the cane crushing capacity of this plant to 5,000 tonnes per day. In 2015, the company acquired another sugar plant at Sangli, Maharashtra having a cane crushing capacity of 1,750 tonnes per day for Rs 24 crore.

These state-of-the-art facilities serve as a role model for the industry and have achieved excellence in plant operational metrics and also have a technological leadership position in the industry. “We have robust quality systems and have also embarked upon 5S & TPM initiatives to create world-class systems & processes,” says Dalmia.

He quips that the company produces sugar of quality which is a hit in markets in U.P. & eastern India and with institutional buyers such as Pepsi, Coke, Britannia, Bharati Wal-Mart, Parle etc. which have stringent quality norms.

The only company to have done capacity addition in the past several years. The best is yet to come.

Sonia: You were telling us about how you need to see what the inventory levels are that many of these sugar companies have. We did speak with the management of Oudh Sugar a couple of hours ago and they told that there is a huge inventory of almost 2.7 million tonnes that they are sitting at, at a price of Rs 27 a kilo, so there could perhaps be a big profit from here on as well. Would you buy the stock now, Oudh Sugar?

A: That’s right and in fact, if you see as you have said that I have pointed out that inventory and the valuation two things are very key. In case of Oudh Sugar, we have seen 27 lakh of bags held by company at sub Rs 27 at Rs 26.40 they have indicated.

If you take the present prevailing price at Rs 34 plus that means they have an unrealised gain of Rs 7 per kg and that translate to a profit of about Rs 175 crore and I am not expecting the prices from here on if it gets hardened, which is most likely and the interest cost per month is not more than Rs 0.30 per kg to the mill, so even if you net that off the Rs 175 crore unrealised gain is there in the inventory held by the company that’s number one and in fact, if you see the small company may be Uttam Sugar which is again a very small company they also declared the results on Friday and Saturday and if you see the profit after tax (PAT) of Rs 68 crore against the loss of Rs 16 crore in the Q3, so my point is that this inventory is only held by the UP based sugar mills.

You won’t find this kind of inventories held by any of the Andhra or Tamil Nadu based sugar mills or may be such a sizable quantity. Yes, inventory gain has to be considered.

Today, we will be seeing the result of Triveni Engineering also again I am expecting that Triveni Engineering will also be having an inventory of about 33 lakh bags as of 31 March, so yes I am keeping my positive stance on all the sugar stocks going forward from here as well because all these inventories will get liquidated in next 2-3 quarters, so you are going to see the huge kind of profits coming in for Q1 and Q2 also which are always generally seen to be dull and boring quarter because of the non-crushing season.

So yes, keeping a positive stance on few UP based sugar mills.

Volatility is very high right now.It can go a few points lower or jump back to higher levels. While prices are indicative of the short term uncertainties, long term numbers could be very different. Post June we will have a definitive number to work with.

Indian Domestic situation is enough to support us until q3 at the least.

keep a close watch on Sugar price in domestic market…There is a good probability of reversal in sugar price…which in turn will lead to the next leg of rally in sugar stocks…

…

Dear Mehnaz,

Cant the government force the mill to not so sell beyond an X price, I mean they cant sell if they want to at X+1 but they can sell at X or X - 1. A kind of oral order, a soft signal, I meant this a poor people’s government and mill owners are seen looting the poor junta. No one will oppose this…

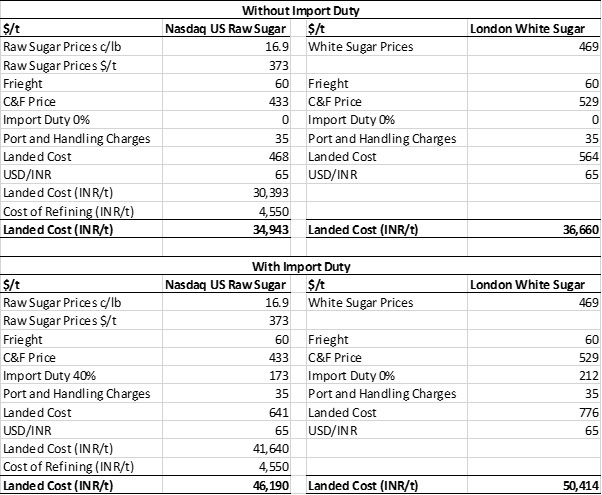

Is this the right way to look at it…are these calculation ok for import parity on current prices?

Is this the right way to look at it…are these calculation ok for import parity on current prices?