Hi Mehnaz, Dhampur crossed 189+ (above upper median line). Can you publish the monthly chart?

I have been experimenting with drawing multiple pitchforks on monthly charts…and the results are fascinating. The stock prices seem to be following these hidden median lines.

But putting up monthly charts of dhamour with multiple pitch forks may appear to be confusing to those not conversant with these techniques. Therefore, invedtors may refer to the earler Quarterly chart of Dhampur thst i have posted above.

In interpreting the chart pl do remember that the forklines act as magnets. Thus it is quite likely that Dhamour will touch the upper forkline at least once.

But also remember that these are not resistance lines…so the stock price may go even higher. Therefore, take the forkline as the minimum price target.

I am not giving the price targets for Dhampur as it is against the valuepickr guidelines.

3 Likes

And here is the monthly chart of Dhampur with two Andrews pitchforks…notice how the price bars are reacting to both the green fork and the yellow fork…now that the upper yellow fork is crossed with a big price bar, the price appears to be headed towards the next higher green forkline…this uptrend in dhampur is fundamentally backed by rising sugar prices in domestic market.

4 Likes

In the case of balrampur chini, the two Andrews pitchforks are very well aligned with each other and hence the price movement here is much more predictable…as can be seen from the chart below…the price appears to be headed towards the red fork line …and that can be taken as the minimum target… after that it is quite probable that the price will touch the upper green forkline too…

2 Likes

Now let us wait for the game to be played out on monthly charts. After that it shifts to quarterly charts. Somehow, i have a feeling that the final climactic game may be played out on quarterly charts…where there is one more buying frenzy…maybe after June / july 2017…

But the final round is going to be quite a risky one…a pump and dump kind of thing. Therefore, i may or may not be invested in that phase

6 Likes

Hi. Your posts are highly valued, but why reduce sugar stocks to a purely technical speculative play?. Why ignore the structural changes in both short and medium term ?

Even if imports are allowed the sugar prices are going to hold steady both in domestic and international market at least for the next two years.

ISMAs prediction of bumper crop in Maharashtra next year is as good as its earlier predictions . Are you taking ISMAs value of 10 million tonnes production from Maharashtra next year ? There is no real chance of that happening. It would probably do 6 million a recovery of 50% from this years level.

If we should go only by previous cycles ,the companies turn into record profits for two more years , not one.

If we should go only by the international sugar prices. Its at 20 cents, it’s peak in last cycle was at 34 cents. We are no where near the peak.

After all the wait we shouldn’t sell it in a knee jerk and miss out on bulk of the gains.

2 Likes

Have a look at dhampur for example,at present the revenue it gets from its cogen power assets is enough to pay off its interest. Rest all including sugar,ethanol,bio fertilizers flows into the bottomline. Next year it will be debt free. How would its PL account look?

Please have a look at Balrampurs return ratios. Its profitable at 14 cents, if sugar stays above 18-20 for two years how much would it make?

Also have a look at dalmia sugars dividend payout ratio and realisation level.

1 Like

This year, there was surplus rainfall even in drought prone areas of marathwada. All the reservoirs in the region reached full level. Maharashtra can produce around 9-10 million tons of sugar. The high sugar prices this year will attract more and more farmers to go more and more for sugarcane cultivation (which is by far the most remunerative crop). I anticipate the production in Maharashtra to bounce back to 9 million tons. That should be enough to take sugar production in india to 27 million tons.

Although, 27 million tons will still keep the sugar prices buoyant…I think any imports …even 2-3 million tons will effectively put an end to the sugar upcycle.

Pl refer to my post no 217 dated 1st june 2016 wherein I had laid down my exit strategy…I am posting a copy of the same…

But by next year, you will be reading about the following argument…

India can produce a maximm of 280-300 million tons of sugarcane(after diversion to jaggery). while the Modi govt sets to implement 10% ethanol blending and as more ethanol is produced from B heavy molases, the maximum sugar produced by India will be around 27 million tons (one litre of additional ethanol reduces sugar production by 1.5 kgs)…in a year or two the domestic demand which is rising at rate of .5 million tons per annum willcatch up with maximum sugar production… thus india is set for a long period of high sugar prices over the next 5-10 years…

At the peak of sugar cycle …i. e around june -auvust 2017, these kind of arguments / projections will drive the sugar sector p/e ratios to absurdly high levels… sometimes i think a p/ e ratio of 15 would be too modest once the real investor frenzy hits sugar stocks… when people will be talking why this time its different… how sugar has come out of cyclicality…

Thats the time to sell… when monthly charts give bearish signal… may be in May 2017…or june or july or Aug2017…

6 Likes

According to Franklin Templeton, the costiest words in the market are …“this time its different”…

It pay to remember that a cycle is a cycle is a cycle.

When a gave a call for purchase in Sept 2015…the sugar cycle was at its lowest…that time too it paid to remember that its a cyclical business and the cycle will turn eventually.

Now we are in upcycle…and we should not forget that its a cyclical business and upcycle will be followed by a down cycle.

In 2003 the upcycle was a more prolonged one because it was caused by farmers distress. While the 2009 upcycle was a caused by drought and ended rather quickly. this time too, the upcycle is caused by drought. Therefore, I would turn more and more cautious as time passes. its already 16months since the turnaround happened. Farmers would be quite keen to go back to sugarcane plantation in view of the high prices.

hence I would look for topping signals on long term charts to exit.

8 Likes

I have been invested in sugar stocks since April 16. P/E of 15 does look very absurd in the current scenario, especially since we know that most stocks (even the better ones) are no where near that kind of valuation.

2 Likes

yes…quite low p/es…doesit not indicate that the market expects the upcycle not to be a prolonged one…

1 Like

Thanks for the reply.

My argument is not on the prolonged upcycle but on sugar price staying at sustainable levels for a prolonged period.

While even if we take up the Maharashtra 9 million figure we will end up with 27 million, which leaves no room for buffer stocks , no room for consumption growth.

If the price stays at sustainable levels, the heavily indebted firms which will retire their debt this year, will continue to show impressive profits in the short to medium term.

1 Like

Any updates on Oudh Sugar. Is it worth holding compares to other peers

a good set of numbers by dwarikesh for Q3 . While I believe its on course to reach an eps of around Rs. 100 for the entire year i am much more elated looking at its inventory position from this set of numbers . The crushing season is currently at its peak Jan- March/April and the inventory which Dwarikesh is piling up is significant.

To highlight this has been the highest crushing by Dwarikesh in its entire lifetime from 2002 in the Q3 quater. The inventory of 182 crores has been piled up with Jan to March the nearest Q3 inventory pile up being in 2011 which was 90 crores . Q4 as usual for sugarcance companies is expected to be a blockbuster quarter for the company.

While the sales can be said to be dismal for the quarter its still the highest q3 sales since december 2012. Inspite of the lower sales the realizations (sales price/ton ) seem to be higher than average realization for Q2 resulting in increasing in PAT from 37cr to 42cr. The sugar recovery seems to be at an all time high for Dwarikesh using Co 0238 sugarcane varierty.

The average recovery in this season would be 12.4 per cent at Bundki and 12 per cent for Bahadarpur as stated by S.P. Singh, chief general manager, DSIL for 2017. Source :

In comparison to the results by Dalmia bharat (DB) it is to be noted that DB sugar inventory for Q3 is around 170 crores from last years 117 crores whereas DSIL has built inventory worth 182 crores vs last years 13 crores inspite of Dalmia being double the size of Dwarikesh . The increase in employee costs, consumption and expenses can be attributed to the crushing season though need to study how it fares incomparison to previous crushing seasons and its competitors. The finance cost is decreasing is a healthy sign. If the prices remain stable then the coming 2 quaters will see some good results. But again no view on this sector can be taken for a longer term as the next season might change the dynamics of the industry completely.

Disc: Invested at lower levels of 290 and forms a small part of my portfolio

Edit : Sunday 05.02.2017

Missed on reading the segment wise revenues. Its seems that Dwarikesh sold 50 crs worth of sugar lower than previous quater but the co gen segment helped it . The segment results show sugar division profits as merely 11crs vs last quaters 48 crs . This surely has to do with higher costs of this production season ( employee costs/ other expenses and raw materials loaded in this quater )

2 Likes

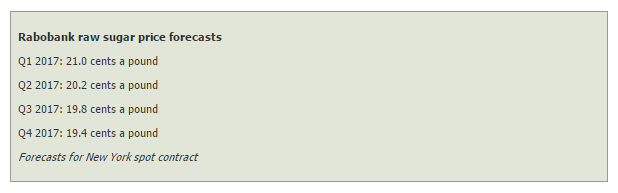

Seriously ![]()

Is this somewhere near to correct? Or is it a sign for everyone to change lanes.

Also found this link but since i am not subscribed to them i couldnt get access to it.

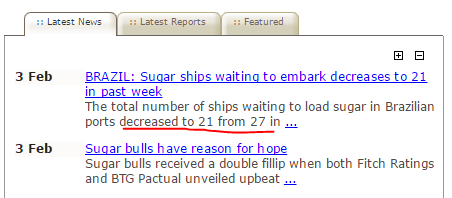

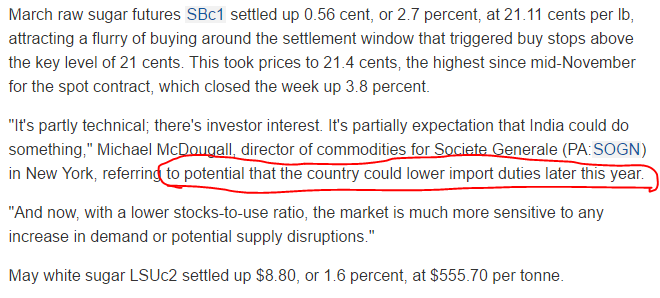

Check the above underlined statement. Any idea?

Lower import duties??

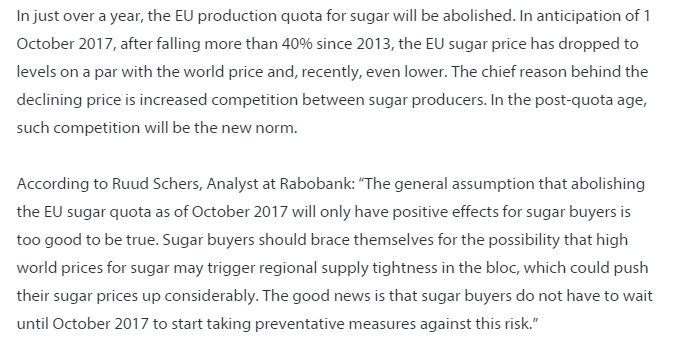

And Something in EU:

What is everyone trying to say? Different markets different interpretations.

1 Like

The global sugar futures market is very much similar to our financial markets . Lots of varied opinions, forecasts are made on factors including weather, crop maturity, ethanol, real vs USD , technicals , India.

India is the biggest consumer and second largest producer . India’s surplus/deficit numbers affects the futures pricing in a big way. ISMAs commentary, numbers are closely tracked .

Though ISMA has maintained that imports are needed. Its more like posing to keep prices in check so the govt does not intervene. In recent concalls of UP mills ,the management accept the fact that India must import later this year. The global sugar prices will reflect that.

In Maharashtra, farmers plant sugarcane either as a 17-18 month ‘adsali’ (sown in July-August), 12-month ‘suru’ (January-February sowing) or 15-month ‘pre-seasonal’ (October-November) crop. The adsali and suru crop do not have enough time to mature . The early crushing promised by ISMA is a joke. If crushing starts early the yields will be lower. The 9 million and 10 million figure given by ISMA for 2018 is simply impossible.

2 Likes