Shree Renuka :

Brazil debt is about 4000cr. Restructuring plan with lenders have brought it down to just 30%. The sale of one of its Brazilian plants to take care of that 30% repayment. The Brazil operations will be debt free , with debt free plant .

Can anyone shed light on Renukas Indian debt position (2000 long + 1200 short) and inventory levels ( 2000cr) ?

If Indian debt is manageable, we have an enormous turnaround waiting to happen.

A 500 cr PAT can materialize ( " IF Brazilian restructuring is successful ").

Its Indian refineries are a zones where fair numerative pricing is followed .

It can import raw sugar and export white sugar from its refineries. This will.contribute a additional 1400cr to the top line, at 10% margin .

A risky multibagger turnaround?

Please provide your views.

Today was a momentous day…sensx fell by around 500 points…sugar stocks too fell by around 5%…

On the other hand SUGAR 11 touched 24.09 cents and is now trading just below 24 cents…in the cash market FIIS bought 3400 crores and DIIS bought around 1600 crores…

…once again the retail investors became bakra…selling into the fall.

Ace investor Anil Kumar Goel continuously accumulating Dhampur on every dips. Yesterday he bot 25,000 shares. He is now having 33,25,000 shares which translates into equity size of 5.01%.

Posting some tender rates i got from a trader… which just shows that even though we have festive season around, ground reality has not changed and prices are same last 3-4 months

and since the Government has already flushed out a lot of Sugar inventory from the mills and now they have very less Stock with them … which will last just 2-3 months i guess …

I am trying to understand Mills Profit from equity stock point of view …

Suppose if today rates are 45 and mills sell 100 kg …

With Rs 5 profit … so Rs 500 profit ( 5*100 )

Even if rates go Rs 65 but later mills left with only 20 Kg to sell

Say profit Rs 25 * 20 kg (65-40=25)

Practically profit remains the same Rs 500/-

If Mills will not have stock to sell …

So how are the mills gonna earn bumper more profit even if price increase to 65/- …

in the times to come … which we are expecting retail prices will jump

my argument may sound a bit Odd , but if someone may explain will be highly useful !!

Disclosure…pl refer to my post no 637 wherein I have already declared that my portfolio is heavily skewed towards Dhampur…therefore, insofar as Dhampur is concerned, my view have a bullish bias.

And here is the official confirmation that Maharashtra will produce 5 million tons of sugar…that is down by 3 million tons…that takes the sugar production figures for the present season to 22.5 million tons…less than the amount estimated by ISMA

And here comes the first recommendation to buy UP based sugar stocks…just as the sugar stocks are about to embark on the next leg of the sugar rally…in due course, there will be lot many experts whose bullish recommendations will cause a buying frenzy in sugar stocks…

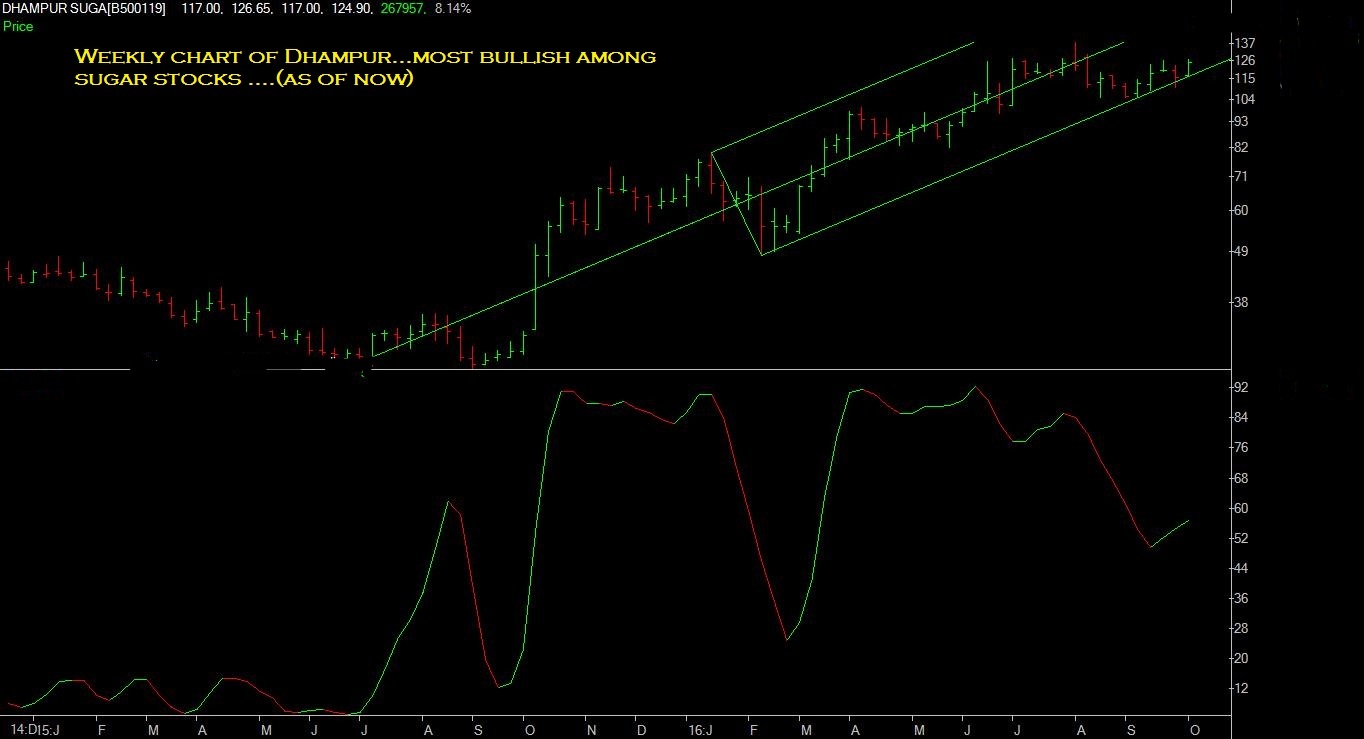

One of the rules of Andrews Pitchfork technique is that the price crosses the median line with a lot of momentum…i.e the median line is crossed by a long price bar as happened in the case of Dhampur for the months of Oct 2015 and March 2016…where the stock almost doubled while crossing the median line (in green)…therefore, I anticipate that the stock may cross the median line(in green) in Oct or Nov with a big price bar …till it reaches the next median line (in red) which is around 210-220 levels…

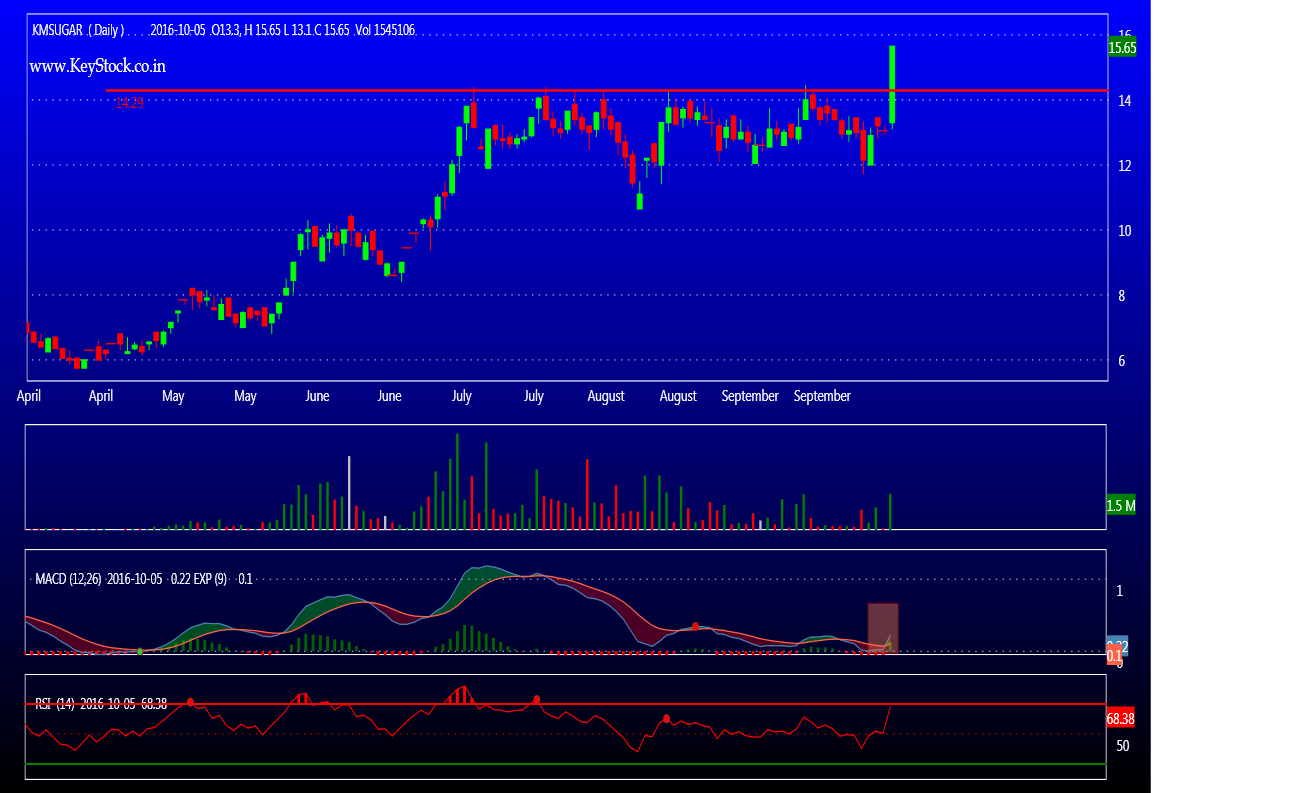

Mehnaz Jee, I am new to this forum and this is my first post. I have read all the posts as of today and can say that you share your views and comments in a matured way. What’s your views on K M Sugar Mills ? I am invested in it. Though I am not as experienced as you, in my view sugar sector seems to be optimistic at least may be for one more year from now because of supply & demand gap and firm sugar prices. Correct me if I am wrong. As recommendation comes to be invested in UP based sugar stocks looking to the upcoming election, apart from Dhampur, Balrampur, K. M. Sugar, which are the other UP sugar stocks available at good valuation and with strong fundamentals. Your valuable reply is appreciated. Thanks in advance.

hi guys,

There is a conversation in ET Now with my shyam sekhar of ithought, one of the early entrant of the sector. His views are quite optimistic about the sector. some points he has mentioned to selecting the companies

If we apply the above critera, then we are then left with Balrampur, Dhampur, Triveni and Dalmia sugars…

Another noteworthy thing is, he believes that there is a structural change in sugar sector…that implies that the sugar rally will last longer and also that sugar stocks will get rerated at higher p/e multiples.