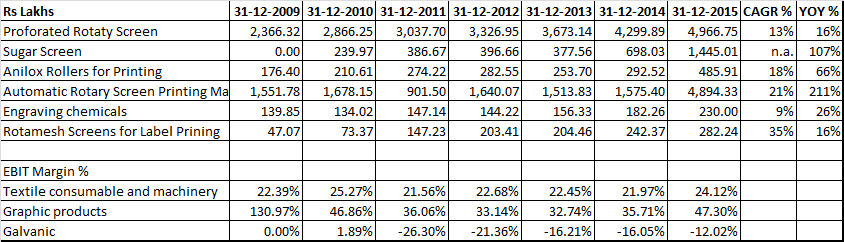

Segmetnwise Sales breakup of Stovec from Annual report indicate major growth of printing machine. Sales of Automatic rotary printing machine have more than doubled to Rs 49 Cr in CY15 vis Rs 15.7 Cr in CY14. Sugar Screen shown second largest growth

In view of major growth in Printing Machine, I believe that growth is more dependent on Textile Capital Expenditure then saving from Nickle price. Nickle cost for CY15 has increased by 23% in CY15 while Average Nickle price in CY15 declined to Rs 755 per kg from Rs 1026 per kg in CY14

I did attend the AGM of the company held recently. Unlike the AGM of other MNCs where the managements are very clear and open to providing details to the queries to the shareholders, here the senior management had a lot of resistance on making any comments which may be forward looking. They feel that the improvement has in the performance of the company has been due to more focus on India and initiatives done particularly for Indian market. Credit goes to the new management for the same. Some of the machines introduced for Indian markets have done well and have been the reason for growth. The negative was - it seemed that the overall market size is quite limited and they already have a high market share. Also, future is depended on the capex plans of the clients and hence its not in their control and could be cyclical.

Some idea about cost of printing machine of Stovec and other competitor in India. Not sure about date of publication but source is Textile Ministry hence expect it to be realiable although dated.

As indicated, while India made rotary printing machine are selling anywhere between Rs 10-30 lakh, Stovec (old name STORK) is being sold in range of Rs 1.5-2.5 Cr comparable to Zimmer machine.

The quality provided by Stovec would be perceived to good as recent volume jump observed in Printing machine sales during 2015. Do look forward to other members view on same.

Discl: I continue to hold Stovec since last 9 months and not changed my position in last 1 month. My view may be biased,

Has anyone looked at the impact of the new textile policy on the capacity creation and volume growth in textile industry? Could have a significant impact on Stovec’s machine and/or consumable sales.

Following are the key points:

The government will provide additional 10% subsidy under Amended Technology Upgraded Funds Scheme (ATUFS) to garment players (25% ATUFS subsidy for as against earlier subsidy of 15%) for next three years. It expects additional outgo of funds of Rs 4-5 bn per year.

The government will provide additional 5% duty drawback on garment exports for next three years

(total ~ 12% duty drawbacks to garment exporters as compared to ~7% earlier). It expects additional outgo of Rs 55 bn per year.

Government shall bear the entire 12% of the employers’ contribution of the Employers Provident Fund Scheme (against 8.33% earlier) for new employees of garment industry for first 3 years who are earning less than Rs 15,000/month. It has made employees contribution to EPF optional for employees

earning less than Rs 15,000 per month.

Minimum number of working days for regular employees reduced to 150 days for Garments manufacturers.

The government has allowed maximum overtime of 8 hours/week for workers involved in garment manufacturing against 4 hours/week earlier. Introduced fixed term employment for the garment sector. A fixed term workman will be considered at par with permanent workman in terms of working

hours, wages, allowance and other statutory dues.

Essentially what Stovec does is makes printing machines and then provides the ink/catridges/spare parts and after sales service. These kind of companies are very stable as the fortunes of its customers are tied to the company where they have purchased the machines, inks and catridges from. In addition, SPG seems to be the gold standard in printing technology like Bose is in Audio. Companies that have products that are top of the line gold standards have a big advantage over their cheaper rivals - people aspire to upgrade to them and with any increase in capex budgets they generally do.

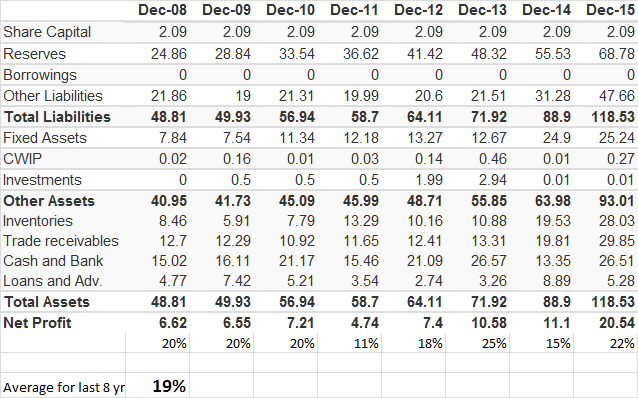

Stovec has an average return on assets of about 19% which is remarkable for a business that essentially serves the textile industry which has an average ROA of about 9%. This means its top of the line in ROA as well.

Having said that however, the part that may impede its growth is that it serves the textile industry which because of the inherent low returns is always going to look for low cost solutions. There are going to be very few players with high ROA’s ( Vardhaman Textiles, Indo Count) and only these guys will have Stovec in their plans. There is a natural limit to how much it can grow because of the economics of customers it supplies its machines to. Growth will happen but slowly. In fact, the textile industry is a littered with bankrupt firms. Research in predicting bankruptcy in Textile firms is a very active area of many a Phd thesis. Google “bankruptcy in the textile industry” and you will see what i mean.

I like this awesome company but i honestly i am shit scared about investing in it…

As I understand the business, the company is into assembling printing machines and manufacturing rotary screens and inks. It is a kind of business wherein once you sell the equipment, you will have repeat customers for selling screens and ink.

One thing which I am curious about is what is the operating life of a rotary perforated screen that the company is selling, which impacts repeat purchases.

* Facility: China, Brazil are the only other facilities of the parent company.

* India is the only rotary machine manufacturing plant outside Netherlands. Parent co. doesn't have much presence of selling rotary machines in export market hence, growth opportunity is there for the Indian co to tap.

* Manufacturing time 3-4 months.

* Semi-automatic- R&D is in progress would also be developing indigenous fully automatic machine. Once, done it will open further export market. most of the machines are mechanical in India. People will progress from mechanical to semi-auto and then to fully-auto.

Stovec AGM Q&A:

* screen market in India about 200 Cr.

* 75-80 machines sold in best year, 20-25 in a worst year. Hence tough to give the number on market size.

* Royalty increased by 50%-> new products are being added. Some of the existing products (screens) have matured and have been facing competition.

* CAPEX- yes, have constructed a new shed (pre-fab) for increasing the capacity seeing the good demand for next 2-3 years.

* The Indian team was appreciated for fantastic product development over past 3-4 years. Due to which Stovec was able to increase substantial market share in India.

* Order book position is comfortable.

What would be interesting is to understand the demand and market position in new set of digital printers. The market potential for the same is high and the textile industry is also moving towards more digital printing in the future. If they can get market leadership in digital printing then there is huge potential. They have also won international awards for the same.

@rationalist For sure digital printing is the new thing and will be more suited for shorter runs and better designs. SPG group seems to be already doing a lot in this area and may be able to benefit. However, it may take few years before it becomes material in overall scheme of things.

Thanks for insightful note. I had invested in the company . I thought that Nickle (being major raw material for screen) price increase would adversely affect the company in medium term. However, despite in Nickle price the company is able to manage margin in recent past.

My second concern was about increased exposure of the company in sugar screen business which is loss making. I could not get any justification on same and that was also major discomfort for me. Do you have any view on sugar screen business?

But for Sugar screen, a very good company for compounding investment for a long term investor in my opinion.

I did check with a small scale textile mill and I was told that the life is in terms of number of meters printed(did not provide a number). Hence other than the ink even the screens themselves need to be replaced once in a while

Could you get any color on their Investment is jaysynth dye? I wrote to the company within days of receiving the annual report but haven’t heard from them.

@dd1474 - Yes, at times it gives a bit of dis-comfort to see the investments done in the sugar screen business + small investment in the ink company recently - however, I also feel that this is how MNCs operate. To be in some business or to remove some conflict they do pay a premium and the story may unfold over a longer period only. Anyways, its good to see that the sugar screen business has turned profitable and seems to be making decent profits. Based on the AGM interaction, it was not an highlight area.

@csatishk - they didn’t reveal much. Seems to be some long term strategic planning for future. They might be wanting to manufacture inks in India or may be its for digital ink.

That is good to know. Otherwise amazing business which is already wealth multiplier for investor (25X in 10 years.), Wish contnue to compound wealth for investor at same or higher rate in future as well.

Indian Packaging and Label Industry continues to grow strongly and is also attracting international

attention. However, it has still not grown to the level of international packaging & label industries. The

increasing competition has driven printers to invest in newer and diverse printing and converting

technologies. In years to come, Printers who have technology and resources will be at added advantage

and can cater to a demanding consumer oriented market.[/quote]

So, can I assume they build printers & inks for printing Packaging and Labels? Then companies like Huhtamaki PPL, TCPL Packaging can use their products for printing!! If this is true, then the demand for the company can be linked to the performance of Textile, FMCG, Pharma sectors!!